Cashforce raises €2 Million to accelerate international rollout

| 27-02-2018 | Nicolas Christiaen | Cashforce | sponsored content |

Cashforce, a fintech leader in Cash forecasting & Treasury solutions for corporates, announced today that it has closed € 2 million in Series A financing. The internal funding round was led by Volta Ventures and Michel Akkermans (Pamica NV), reinforcing their previous commitment to the company. The Series A financing enables Cashforce to accelerate the ongoing international roll-out and fuels its rapid global growth and industry leadership as a premier provider of Cash forecasting & Treasury solutions. Organisationally, staff will be expanded, and operations will be scaled up – with a significant number of new hires in 2018. Product-wise the company is working on developments that will enable even more insights and potential savings for its clients. Commercially, supporting and growing the customer base and increasing customer success and adoption as well as continuing to build strategic partnerships and alliances are part of the strategic plan.

Cashforce, a fintech leader in Cash forecasting & Treasury solutions for corporates, announced today that it has closed € 2 million in Series A financing. The internal funding round was led by Volta Ventures and Michel Akkermans (Pamica NV), reinforcing their previous commitment to the company. The Series A financing enables Cashforce to accelerate the ongoing international roll-out and fuels its rapid global growth and industry leadership as a premier provider of Cash forecasting & Treasury solutions. Organisationally, staff will be expanded, and operations will be scaled up – with a significant number of new hires in 2018. Product-wise the company is working on developments that will enable even more insights and potential savings for its clients. Commercially, supporting and growing the customer base and increasing customer success and adoption as well as continuing to build strategic partnerships and alliances are part of the strategic plan.

“Cash management & Treasury is evolving from a focus on data acquisition to Treasury automation and data analysis, enabling Treasury departments to bridge the gap between the Finance and other operational departments and enable data-driven strategic decision making. On top of that, Cash flow forecasting has become the major focus of the industry.”, said Nicolas Christiaen, CEO and co-founder of Cashforce. “This investment also re-confirms our investors’ confidence in the leadership that Cashforce has established in the Treasury space, our continued rapid growth and the potential to re-define the category.”

Additionally, Cashforce announced that Michel Akkermans will become Chairman of the board. Michel Akkermans is a serial entrepreneur in fintech companies. Amongst others, he was the Chairman and CEO of successful companies such as FICS and Clear2Pay. After the global payment solution company Clear2Pay was acquired by FIS in 2014, he became an active investor and board member in several companies and private equity organisations, as well as a venture partner and Chairman of Volta Ventures.

Cashforce: The Leading Cash forecasting platform for the Modern Corporate

Cashforce is a next-generation Cash forecasting & Smart Treasury Management System, focused on automation and integration for corporates. It helps corporate finance/treasury departments save time and money by offering accurate cash flow forecasting, pro-active working capital management analysis as well as flexible Treasury reporting & automation.

Cashforce is unique because it offers full transparency into what exactly drives the cash flow of mid-size & large corporates with different complexities such as multi-entity, multi-bank, multi-currency and complex ERP(s). Smart algorithms are applied to generate highly accurate Cash forecasts. The intelligent simulation engine enables companies to consider multiple scenarios and measure their impact. Its intuitive user interface allows for extensive and tailor-made analysis & reporting possibilities. Unlike other enterprise software players, the platform is set up quickly, even in the most complex environments, and connecting seamlessly with any ERP system through its ‘plug-and-play’ connectors. As a result, finance/treasury departments can be turned into business catalysts for cash generation opportunities throughout the company.

“While we started off as a Cash forecasting tool, we have added Advanced Working Capital analytics and Smart Treasury functionalities, and are now operative as a comprehensive modular Treasury Management System (TMS). This makes Cashforce a one-stop-shop for the many analytical and operational practices that benefit Financial and Treasury departments,” says Nicolas Christiaen, CEO of Cashforce. “The endorsement we get from both industry experts and clients progressively confirms that our solution really does bring change into the Treasury market. We now see that potential customers compare the classical TMS providers to Cashforce with Cashforce ending up as the preferred solution! Then you know you’re on the right track. We therefore strive to continue our vision to further integrate and automate to provide our customers with an even more effortless experience.”

“Cashforce has brought a very compelling solution to the corporate Cash management market, which is clearly seen in its results. Since its last financial injection in early 2016, Cashforce has demonstrated a rapid growth, including well over 100% annually recurring revenue growth”, explains Michel Akkermans, the company’s recently appointed chairman.

“With a surge in employees to over 25, an increasing and global interest from the market and partnerships with leading corporate banks, private equity firms & Treasury consultants, Cashforce has been expanding both reach and product. We have heard back from multiple existing customers about their positive experiences with the solution and its impact on their business, and they strongly believe in its trajectory moving forward”.

“Cashforce set foot in the Netherlands this year and has been growing substantially, proving that the company can be scaled up relatively easy,” says Nicolas Christiaen. “This would not be the case without the help of Volta Ventures and Michel Akkermans, who not only provided funding, but also lent their vast strategic experience in our market. The plans for Western-Europe as well as the US are outlined, and this funding round will be valuable to accelerate the international roll-out.”

About Cashforce (www.cashforce.com)

Cashforce is a ‘next-generation’ Cash forecasting & Smart Treasury platform, focused on integration and automation. With its technology, Cashforce is helping Treasury departments from large capital-intensive businesses save time and money by offering cash visibility & pro-active cash saving insights. The platform is easy to use and install, and connects seamlessly with any ERP system. Cashforce is headquartered in Belgium with an office in Amsterdam and New York, serving customers globally such as TomTom, Hyundai and Greenyard among many others worldwide.

About Pamica (www.pamica.be)

Pamica is the investment company of Michel Akkermans.

About Volta Ventures (www.volta.ventures)

Volta Ventures Arkiv invests in young and ambitious internet and software companies in the Benelux. The fund has € 55 million under management and is supported by EIF and ARKimedesFund II.

Press Contact Information

Nicolas Christiaen – [email protected] – +32 479 65 52 95

Michel Akkermans (Pamica NV) – [email protected] – +32 3 202 40 30

Most companies, regrettably, experience internal fraud. The financial value of the loss can be small or large – however the impact is the same. Internal investigations, procedural reviews, the time spent on detection, possible prosecution, together with the potential loss of reputation are significant factors above and beyond the monetary loss. Fraud can never be eliminated, but the threat can be minimised through proper procedures.

Most companies, regrettably, experience internal fraud. The financial value of the loss can be small or large – however the impact is the same. Internal investigations, procedural reviews, the time spent on detection, possible prosecution, together with the potential loss of reputation are significant factors above and beyond the monetary loss. Fraud can never be eliminated, but the threat can be minimised through proper procedures. I want to include you in my search for what is right. Newspapers don’t publish what is right but what sells (for the Dutch, why did the Volkskrant publish the story of Jillert Anema this week?). Politicians don’t work from their convictions but what gets them votes. Large companies pay low level taxes in countries where they don’t manufacture & sell, and no taxes where they do. Actions that benefit the environment are not implemented because it weakens our position in global markets.

I want to include you in my search for what is right. Newspapers don’t publish what is right but what sells (for the Dutch, why did the Volkskrant publish the story of Jillert Anema this week?). Politicians don’t work from their convictions but what gets them votes. Large companies pay low level taxes in countries where they don’t manufacture & sell, and no taxes where they do. Actions that benefit the environment are not implemented because it weakens our position in global markets.

Every year the EU raises money by applying a levy on member states that represents a percentage of their Gross National Income (GNI). The EU Budget operates on a 7 year plan and then an annual budget is proposed and agreed. The EU strives to use 94% of expenditure on policies and 6% on administrative costs. As with all budgets, there are 2 sides – income and expenditure. There are 4 main sources of income – traditional own resources, VAT (BTW) based resources, GNI based resources, and other resources. There are 6 main sources of expenditure – growth, natural resources, security and citizenship, foreign policy, administration, and compensations.

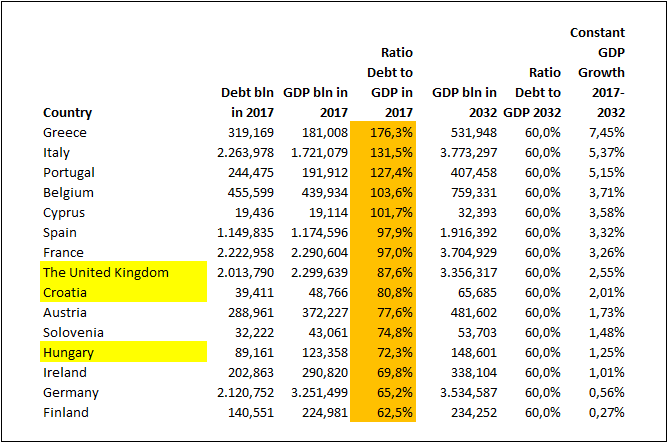

Every year the EU raises money by applying a levy on member states that represents a percentage of their Gross National Income (GNI). The EU Budget operates on a 7 year plan and then an annual budget is proposed and agreed. The EU strives to use 94% of expenditure on policies and 6% on administrative costs. As with all budgets, there are 2 sides – income and expenditure. There are 4 main sources of income – traditional own resources, VAT (BTW) based resources, GNI based resources, and other resources. There are 6 main sources of expenditure – growth, natural resources, security and citizenship, foreign policy, administration, and compensations. A few weeks ago the EU Commission released a report on debt sustainability within the EU. It provides an overview of the challenges faced by member countries over the short, medium and long term to meet the original convergence criteria – specifically, that existing Government debt is less than 60% of GDP. As with most Government related documents it is long – over 250 pages. A lot of attention is drawn to the Debt Sustainability Monitor (DSM) and the challenges faced to achieve the abovementioned criteria by 2032.

A few weeks ago the EU Commission released a report on debt sustainability within the EU. It provides an overview of the challenges faced by member countries over the short, medium and long term to meet the original convergence criteria – specifically, that existing Government debt is less than 60% of GDP. As with most Government related documents it is long – over 250 pages. A lot of attention is drawn to the Debt Sustainability Monitor (DSM) and the challenges faced to achieve the abovementioned criteria by 2032.

Leasing is a common method used in business to benefit from using an asset. The part owning the asset is called the lessor who agrees to allow the user – the lessee – to use the asset, in return for a rental fee. The lessee also has to agree to certain terms and conditions as to how the asset can be used and by whom. This arrangement allows a business to enjoy the benefits of an asset – normally property or equipment – without having to purchase the asset outright at inception. The contract can also offer flexibility to the lessee with regard to replacing an asset when it is determined to be outdated. On the 1st January 2019, new accounting standards will be implemented meaning that for a lessee all lease contracts will have to be displayed on the balance sheet – with exception of short dated leases (less than 12 months) and with a monetary value of less than USD 5000.

Leasing is a common method used in business to benefit from using an asset. The part owning the asset is called the lessor who agrees to allow the user – the lessee – to use the asset, in return for a rental fee. The lessee also has to agree to certain terms and conditions as to how the asset can be used and by whom. This arrangement allows a business to enjoy the benefits of an asset – normally property or equipment – without having to purchase the asset outright at inception. The contract can also offer flexibility to the lessee with regard to replacing an asset when it is determined to be outdated. On the 1st January 2019, new accounting standards will be implemented meaning that for a lessee all lease contracts will have to be displayed on the balance sheet – with exception of short dated leases (less than 12 months) and with a monetary value of less than USD 5000.

On the 25th May 2018, GDPR – regulation by the European union – will come into effect. It requires any company that does business within the EU to protect the privacy relating to the data held on consumers, as well as restricting the types of data that can be collected. Obviously, this will mean extra expense for companies as they have to invest in systems and procedures to meet their obligations. However, a recent report by Deutsche Bank has shown that the implications of implementing GDPR could also have an impact on revenue.

On the 25th May 2018, GDPR – regulation by the European union – will come into effect. It requires any company that does business within the EU to protect the privacy relating to the data held on consumers, as well as restricting the types of data that can be collected. Obviously, this will mean extra expense for companies as they have to invest in systems and procedures to meet their obligations. However, a recent report by Deutsche Bank has shown that the implications of implementing GDPR could also have an impact on revenue.

Since the beginning of February there has seen large declines in all the major stock markets – Dow Jones down 9%, AEX down 7%, DAX down 7%, FTSE down 5%. The major reason given is that the market has been disturbed by the thought that interest rates in the US will rise more quickly than previously expected as prospects of inflation come to the fore. Going counter to this thought is the explanation that stock markets achieved good growth in 2017 – all major markets were up with some growing by 15% – and that this is a bout of profit taking, before participants will buy on the dip.

Since the beginning of February there has seen large declines in all the major stock markets – Dow Jones down 9%, AEX down 7%, DAX down 7%, FTSE down 5%. The major reason given is that the market has been disturbed by the thought that interest rates in the US will rise more quickly than previously expected as prospects of inflation come to the fore. Going counter to this thought is the explanation that stock markets achieved good growth in 2017 – all major markets were up with some growing by 15% – and that this is a bout of profit taking, before participants will buy on the dip. At the moment headline inflation is remaining stable, but it appears that the market is expecting inflation to move higher in 2018. The increase in the yield of US 10 year Treasury rates has been more rapid than expected – at the moment the yield is almost 2.90%. It would appear that the increase in US rates is pulling other currency yields higher. Furthermore rises in US interest rates will have an impact on FX hedging policies for companies.

At the moment headline inflation is remaining stable, but it appears that the market is expecting inflation to move higher in 2018. The increase in the yield of US 10 year Treasury rates has been more rapid than expected – at the moment the yield is almost 2.90%. It would appear that the increase in US rates is pulling other currency yields higher. Furthermore rises in US interest rates will have an impact on FX hedging policies for companies.