| 27-1-2017 | Carlo de Meijer | treasuryXL |

Our expert Carlo de Meijer, distinguished blockchain specialist, has published an article that is worth sharing with you. This is Part I and Part II will follow soon. May we invite you to comment or share your experience with this intriguing topic:

In April last year I wrote a blog on blockchain and monetary policy. In this blog I went into a number of still unanswered questions posed by the European Central Bank around blockchain technology. There was a big uncertainty about the impact of this technology on the future role of central bank money and on monetary policy.

While at that time many financial institutions and startups already paid a lot of attention to this technology, only a handful of central banks were interested in blockchain with the most vocal being the Bank of England. Since than a lot has changed with a growing number of central banks around the globe starting to recognise the potential for blockchain to help them in obtaining their key objectives: stable financial system and efficient financial markets. In the first part of this blog I will try to answer why there is nowadays so much interest amongst central banks in blockchain technology, what are the main benefits and what are remaining concerns. In the second part a Tour de Table will be given, looking at the various initiatives of the central banks.

Central banks are experimenting with blockchain

Several central banks are or have been experimenting with different versions of blockchain-backed systems. A growing number are questioning the point of creating digital currencies, such as the Danes. But they are not alone. Also the central banks of Sweden, Japan, China and Russia have launched similar efforts. Others such as the central bank of Singapore and Canada have already tested blockchain-based currency systems for internet payments, while also the Reserve Bank of South Africa has expressed their optimism towards the blockchain technology and its potential impact on finance. The European Central Bank recently announced a new research undertaking in partnership with the Bank of Japan. Earlier last month the US Federal Reserve released its first major research paper on blockchain.

Why is there so much interest?

But why are so many central banks now embracing blockchain, seriously exploring their potential.

The turning point was a three-day event in Washington , hosted by the World Bank, the IMF and the US Federal Reserve where representatives from more than 90 central banks worldwide expressed broad interest “in how the technology might impact both the banks they regulate as well as their own regulatory practices”.

Central banks’ interest in deploying a blockchain “comes in step” with moves by the big banks to use the technology to ease cross-border settlement transactions and overhaul antiquated back-office infrastructure. Experiments by banks with distributed ledgers as a way to settle trades and record data and transactions, have clearly shown its potential to reduce costs and increase the efficiency of its operations. The distributed ledger and its potential to simplify the record keeping, tracking and accounting process makes it hard to ignore by central banks.

Central banks and public stances: some quotes

Over the course of the past half year many central banks representatives have taken a public stance on their potential use of distributed ledgers and digital currencies. Here follow some of the most interesting quotes.

“Innovation using these technologies could be extremely helpful and bring benefits to society. The technology has the potential to transform multiple aspects of the financial system” Janet L. Yellen, Chairwomen Federal reserve

“We are paying close attention to distributed ledger technology, or blockchain recognizing this may represent the most significant development in many years in payments, clearing and settlement” Lael Brainard, Federal Reserve Board

Other interesting quotes include:

“The conditions are ripe for digital currencies, which can reduce operating costs, increase efficiency and enable a wide range of new applications” People’s bank of China

“A state-sponsored digital currency is still on the agenda, and if adopted, the technology could deliver a range of benefits” Russian central bank

“The technology could be worth using for central banks because it would make for a financial system that does not go down even if the central bank’s computer systems are temporarily taken offline” Mark Carney Bank of England

What are the potential benefits for central banks?

Central banks are now exploring the potential of blockchain and distributed ledger technology. As banks experiments have shown blockchain networks may lead to safer and better payments and securities systems..

- Make money more easily traceable

The inherent property of immutability and transparency associated with blockchain makes it easier for the central banks to trace the money that is in circulation. It would allow them to track every euro, pounds, dollar or renminbi on every step through the financial system in real-time.

- Build single shared record

Central banks are also interested in blockchain technology as a way to build a single, shared record of all transactions among several institutions. The central banks hope they can use the decentralised method of record-keeping to complete and record transactions in the real economy more effectively, quickly and transparently. The creation of a standardised way of recording transactions would allow all the players in the system to communicate more seamlessly. That could leave much less money sitting idle while banks reconcile their different ledgers, as now happens.

- Simplify the settlement process

It has also the potential to create efficiency. Blockchain or the distributed ledger technology has the potential to simplify the settlement chain around securities transactions. The resulting cost reductions, speed of settlement and enhanced transparency may all contribute to more efficient and safer payments and capital markets.

- Reduce transmission costs

It may also drastically reduce the transmission costs and time associated with cross border transfers, by enabling instant transfers between branches both within and outside the country.

The use of blockchain-based digital fiat currency will reduce the amount of banknotes and coins that are in circulation. This will, in turn, reduce the operating costs associated with printing and distribution of currency notes by the central bank.

The wide spread implementation of blockchain based fiat currency will also help the central banks (and government’s) fight money laundering while eliminating the issue of counterfeiting.

The blockchain technology provides a tool to measure leverage in the system and counterparty exposure, and can monitor compliance in real time. It can also answer questions about collateral ownership.

A blockchain could untangle the spaghetti structure of central swap bank lines, which would improve crisis response capabilities.

Digital currencies may eventually benefit the developing world too. Because they are low-cost and easy to use on electronic devices, digital currencies may enable greater access to financial services for the billions of the world’s unbanked.

This all should make the financial system more transparent, fast, efficient and secure. According to a Bank of England research paper produced last year, the economic benefits of issuing a digital currency on a distributed ledger could add as much as 3 percent to a country’s economic output, thanks to the efficiency it could offer.

Remaining concerns

There are however still a range of questions and all sorts of security and regulatory concerns where central banks will need answers for before blockchain technologies are to become a key part of the future central banking landscape.

Questions such as: How may it impact monetary policy?; What are the implications of issuance of central bank digital money?; What is the impact on physical cash?; How would it impact on central bank seigniorage?; What are the implications for the integration of the European capital market?; and What is the impact on exiting projects such as T2S?

In previous blogs I already tackled some of these issues. See: “Could blockchain bring the EU Capital Market Union forward?” November 6, 2016; “Blockchain: What about T2S?” June 30, 2016; and, “Blockchain and Monetary Policy” April 29, 2016.

There are also a number of concerns that are already highlighted, such as assurance around scalability, data integrity, resilience and resistance to cyber-attack. A big concern is regulation of digital currencies. This is a looming challenge that will require cross-border co-operation. Monetary authorities must come together to start thinking about the necessary regulation of digital money that will be flowing around the world.

See my blog: “Blockchain and Regulation: do not stifle innovation!” April 4, 2016.

When can we expect central bank-operated digital currencies?

When a move to official digital currencies might occur is hard to estimate. Central bank-operated digital currencies could be ‘decades away’ according to the more pessimistic (or realistic?). But what is sure is that it will take a number of years before any central bank issues its own currency onto a live distributed ledger. Research is still at an early stage and many puzzles still have to be worked out.

It has become clear that central banks are set to take a much more active role in the development of blockchain technology. But how active that will be is not yet clear. The Fed’s preference at this stage is still to take a fairly hands-off approach and allow banks take lead the way – “as long as they remain within defined guidelines and best practices”. A switch could happen within the next 5 to 10 years. When large parts of the financial system are using blockchain for financial transactions, so will central banks!

Carlo de Meijer

Economist and researcher

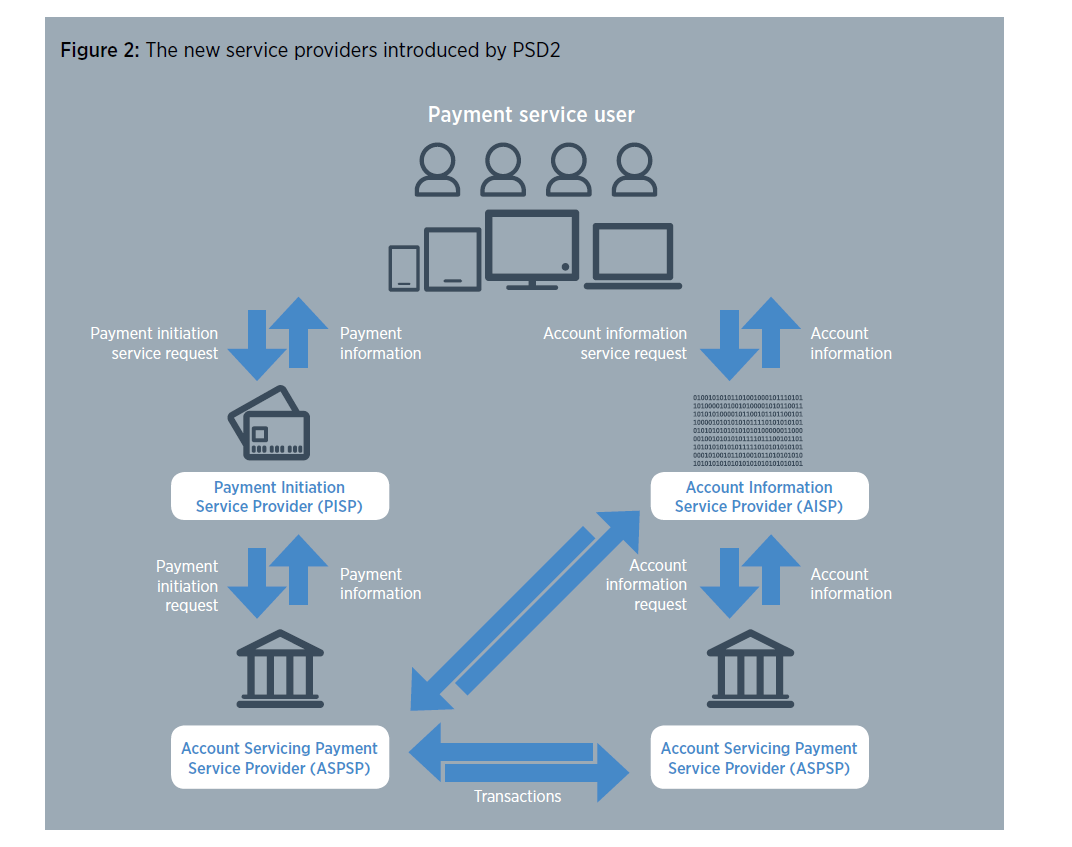

The Directive 2015/2366 on payment services in the internal market (hereinafter PSD2) was adopted by the European Parliament on October 8, 2015, and by the European Union (EU) Council of Ministers on November 16, 2015. The PSD2 updates the first EU Payment Services Directive published in 2007 (PSD1), which laid the legal foundation for the creation of an EU-wide single market for payments. PSD2 came into force on January 13, 2016, and is applicable from January 13, 2018 onwards.

The Directive 2015/2366 on payment services in the internal market (hereinafter PSD2) was adopted by the European Parliament on October 8, 2015, and by the European Union (EU) Council of Ministers on November 16, 2015. The PSD2 updates the first EU Payment Services Directive published in 2007 (PSD1), which laid the legal foundation for the creation of an EU-wide single market for payments. PSD2 came into force on January 13, 2016, and is applicable from January 13, 2018 onwards.

François de Witte – Senior Consultant at

François de Witte – Senior Consultant at

With globalisation and an increasingly complex business environment, having an efficient and centralised payment system is vital to any multinational’s success. Recognising this, we at HSBC are proud to have successfully connected to Treasury Intelligence Solutions (TIS) in Asia for automated payment and bank statement processing.

With globalisation and an increasingly complex business environment, having an efficient and centralised payment system is vital to any multinational’s success. Recognising this, we at HSBC are proud to have successfully connected to Treasury Intelligence Solutions (TIS) in Asia for automated payment and bank statement processing.

As you may remember I travelled throughout South Africa in december 2016. Being back home I was curious to learn if there were developments in the blockchain area. A

As you may remember I travelled throughout South Africa in december 2016. Being back home I was curious to learn if there were developments in the blockchain area. A