Een parttime CFO – parallellen met de Flex Treasurer

| 29-6-2017 | CFO netwerk | treasuryXL |

CFO netwerk biedt (parttime) CFO diensten aan ondernemingen, waarvan aard en omvang van de activiteiten de fulltime inzet van een CFO niet rechtvaardigen. Wat dat betreft herkennen wij parallellen met onze Flex Treasurer, die wij op treasuryXL aanbieden aan ondernemingen, die wel treasury exposure hebben, maar geen ruimte om een fulltime treasurer of cash manager in dienst te nemen. We waren in gesprek met Jeffrey Janssen van CFO netwerk en hebben de parallellen voor u uitgewerkt.

CFO op maat

Wat is de toegevoegde waarde van een CFO voor een onderneming?

Veel jonge en kleine bedrijven hebben vaak niet de financiële mogelijkheden om een ervaren CFO in dienst te nemen. In deze situatie is wellicht een parttime CFO een goede oplossing. Een ervaren professional met commitment die u voor een beperkt aantal uren inhuurt, maar toch de vinger aan de pols houdt en indien nodig 24/7 voor u beschikbaar is.

Maar waar u als ondernemer ook bent in de levenscyclus van uw bedrijf, het goed functioneren van uw financiële afdeling is van groot belang en zij hoort u tijdig te informeren over strategische, financiële vragen die van belang zijn voor het voortbestaan van uw bedrijf. Daarbij gaat het niet alleen over cijfers, maar ook over een sterke CFO, die u uitdaagt en als business partner optreedt bij de bepaling van de strategie en volgens een strakke CFO-agenda de groei van uw bedrijf ondersteunt.

Uw bedrijf groeit

U werkt hard en investeert. Het bedrijf groeit en alles gaat eigenlijk beter dan verwacht. Of toch niet? Er ontstaan groeistuipen en er worden veel ad-hoc beslissingen genomen om de voortrazende trein op het rechte spoor te houden. In deze fase kunnen grote fouten worden gemaakt die de continuïteit in gevaar brengen. De belangrijkste hiervan is dat het strategische plan niet wordt gevolgd en dat dit plan niet regelmatig wordt geëvalueerd en aangepast. Aspecten die in deze fase van groot belang zijn:

- Het hebben van juiste en tijdige stuurinformatie (ook wel KPI’s genoemd)

- De kwaliteit van de organisatie (juiste mensen, juiste skills) De administratieve systemen en procedures. Zijn deze nog adequaat en kunnen ze de groei aan?

- Is er voldoende cashflow aanwezig om de continuïteit te waarborgen?

Succesvol en nu verder…

Alle bedrijfsprocessen zijn goed ingericht – het gaat heel goed met uw bedrijf. De resultaten zijn uitstekend, maar blijft dat zo? Indien u niet bezig bent met nieuwe innovaties, oog hebt voor de veranderingen in de markt loopt u het risico dat uw groei gaat stagneren en te laat uw organisatie hierop aanpast. Ook dan moet U keuzes maken die ingrijpend zijn en een weerslag hebben op mensen en systemen. In deze fase is het cruciaal dat u de continuïteit van het bedrijf centraal stelt en het bedrijf robuust maakt voor de toekomst. Ook hier is het de taak van de CFO om dit spanningsveld te bewaken en u tijdig te helpen in uw besluitvorming.

Ups and downs

Iedere onderneming komt ze vroeger of later tegen. Door te weinig innovatie streven uw concurrenten u voorbij. De resultaten lopen opeens terug. Uw bankiers komen vaker langs en aandeelhouders zijn niet tevreden en eisen veranderingen. U bent het grootste deel van uw tijd kwijt aan het managen van uw liquiditeit en het sussen van aandeelhouders en personeel. Zorg dat u in deze fase de juiste mensen binnenhaalt om het tij te keren, dan wel te zorgen dat keuzes worden gemaakt. Dit kan van levensbelang zijn om een faillissement te voorkomen.

Wat kan een CFO betekenen?

Een krachtige CFO is een sparringpartner die u als ondernemer in iedere bedrijfsfase ontzorgt en uw financiële continuïteit bewaakt. Hij of zij is onder meer verantwoordelijk voor de financiële systemen en processen, de stuurinformatie en de contacten met financiers en accountant. Maar bovenal moet hij als financiële business partner onderdeel zijn van uw team en mede sturing geven aan de strategische agenda van uw onderneming. Een onderneming kan niet functioneren zonder een goede CFO in het hart van uw organisatie.

Een Flex Treasurer als ondersteuning voor de CFO

We merken dagelijks dat treasury iets is waar CFO’s en Controllers er vaak te weinig tijd voor hebben en/of niet altijd de noodzakelijke kennis. HR managers en directeuren bemoeien zich er liever niet mee.

Ook hier hetzelfde beeld: de meeste organisaties zijn niet groot genoeg om een treasury-afdeling te huisvesten maar dat betekent niet dat deze organisaties geen kosten kunnen besparen of dat er geen mogelijkheden zijn voor bijvoorbeeld funding. Om de treasury van uw organisatie onder controle te hebben is het niet altijd nodig om er een complete afdeling van te maken.

Een ervaren hands-on treasurer kan een eerste check doen binnen de organisatie om te bepalen of het de moeite waard is om te investeren in treasury. Door optimalisatie van interne processen, het beter beheren van banken en bankkosten of het opnieuw organiseren van FX processen kan vaak een substantiële besparing worden gerealiseerd.

Cash & liquidity management ondersteuning

Heeft u een goed overzicht van uw liquiditeitspositie? Is er geen versnipperde cash- en kredietbenutting? Bent u onlangs geconfronteerd met liquiditeitsproblemen t.g.v. onverwachte uitgaven? Wordt u regelmatig geconfronteerd met manuele verwerking van betalingen? Bent u recent geconfronteerd met fraudegevallen? Is het aantrekken van de financiering een issue?

Een treasury expert kan u helpen in het vinden van de juiste antwoorden op deze vragen. Een Flex Treasurer kan ondersteuning bieden op tijdelijke basis, onder meer voor de volgende aspecten:

Begeleiding opvolging liquiditeitspositie groep en uittekenen processen in dit verband

Assessment van het cash forecasting proces en voorstellen tot optimalisatie

Optimalisatie betalingsprocessen (incluis fraudepreventie)

Advies selectie bankpartners

Nazicht van de bankvoorwaarden

Bepalen van de optimale financieringsstrategie

Automatisatievoorstellen en begeleiding van de implementatie

Optimalisatie werkkapitaalverkeer

Kampt uw bedrijf met een DSO (gemiddelde betalingstermijn klanten) die veel hoger is dan het sectorgemiddelde? Heeft u een duidelijk afgelijnd acceptatieproces en een politiek voor de betaaltermijnen? Is je facturatieproces optimaal? Heeft u een afgelijnde politiek voor de selectie en de betalingstermijnen aan uw leveranciers? Heeft u regelmatig incassoproblemen? Kampt u met wanbetalingen en afschrijvingen op uw klantenportefeuille? Ondervindt u regelmatig reconciliatieproblemen bij binnenkomende en uitgaande betalingen?

Dan kan een Flex Treasurer, die treasury & working capital management expert is, u helpen bij het vinden van de juiste antwoorden op deze vragen en het optimaliseren van uw werkkapitaalbeheer.

FX en IR risico analyse

Heeft u een goed zicht op de risico’s die je bedrijf oploopt (o.m. valuta en renterisico) en op de impact hiervan op uw bedrijf? Heeft u een politiek in verband met de risicoafdekking? Heeft u een zicht op de mogelijkheden om ze in te dekken? Koerswijzigingen in valuta en rente kunnen zeer vluchtig zijn en leiden tot onnodige extra kosten. Als u zich wilt concentreren op uw ‘core business’, zonder u zorgen te hoeven maken over bv. de EUR/USD wisselkoers of de Europese rente dan is het inhuren van een Flex Treasurer de ideale uitkomst. Hij kan de organisatie helpen eenvoudig en effectief de risico’s af te dekken, alsmede te onderhandelen over betere spreidingen en lagere kosten bij uw bank.

Aangeboden diensten

Met de verschillende CFO diensten van CFO Netwerk krijgt u het beste van beide werelden: de expertise van een ervaren CFO en op maat gemaakte uitbestede CFO diensten — tegen een prijs die u zich kunt veroorloven. De CFO-diensten zijn schaalbaar in de tijd. Dit betekent dat het niveau van ondersteuning geleverd wordt, dat u nodig hebt en wanneer u het nodig hebt.

Op treasuryXL bieden wij een Treasury Quick Scan aan, die beoogt de treasury-pijnpunten in kaart te brengen en de aanbevelingen om deze te verhelpen, inclusief de business case. Op basis daarvan kunt u bekijken of er voor verdere ondersteuning een treasury-expert voor uw organisatie zinvol is.

Daarnaast biedt treasuryXL ook treasury coaches aan. Treasurers werken vaak alleen of in een klein team en hebben ondersteuning nodig van andere (meer senior) treasury professionals. Vaak is deze ondersteuning niet aanwezig binnen het eigen team. In ons netwerk zitten een aantal senior professionals die deze ondersteuning op regelmatige basis kunnen bieden. Zij kunnen op regelmatige basis of incidenteel ingepland worden.

Mogelijke samenwerking

Omdat er duidelijk parallellen zijn tussen de diensten van CFO netwerk en treasuryXL en de diensten elkaar goed aanvullen, onderzoeken wij op dit moment of wij wellicht kunnen samenwerken. Het doel is om organisaties, die een financiële professional – parttime CFO of Flex Treasurer – nodig hebben, als klant nog beter van dienst te zijn.

In their first session

In their first session

In the

In the

Our expert Carlo de Meijer is our blockchain specialist and publishes his articles on a regular basis. We present his latest article about blockchain and supply chain finance in a shorter version.

Our expert Carlo de Meijer is our blockchain specialist and publishes his articles on a regular basis. We present his latest article about blockchain and supply chain finance in a shorter version.

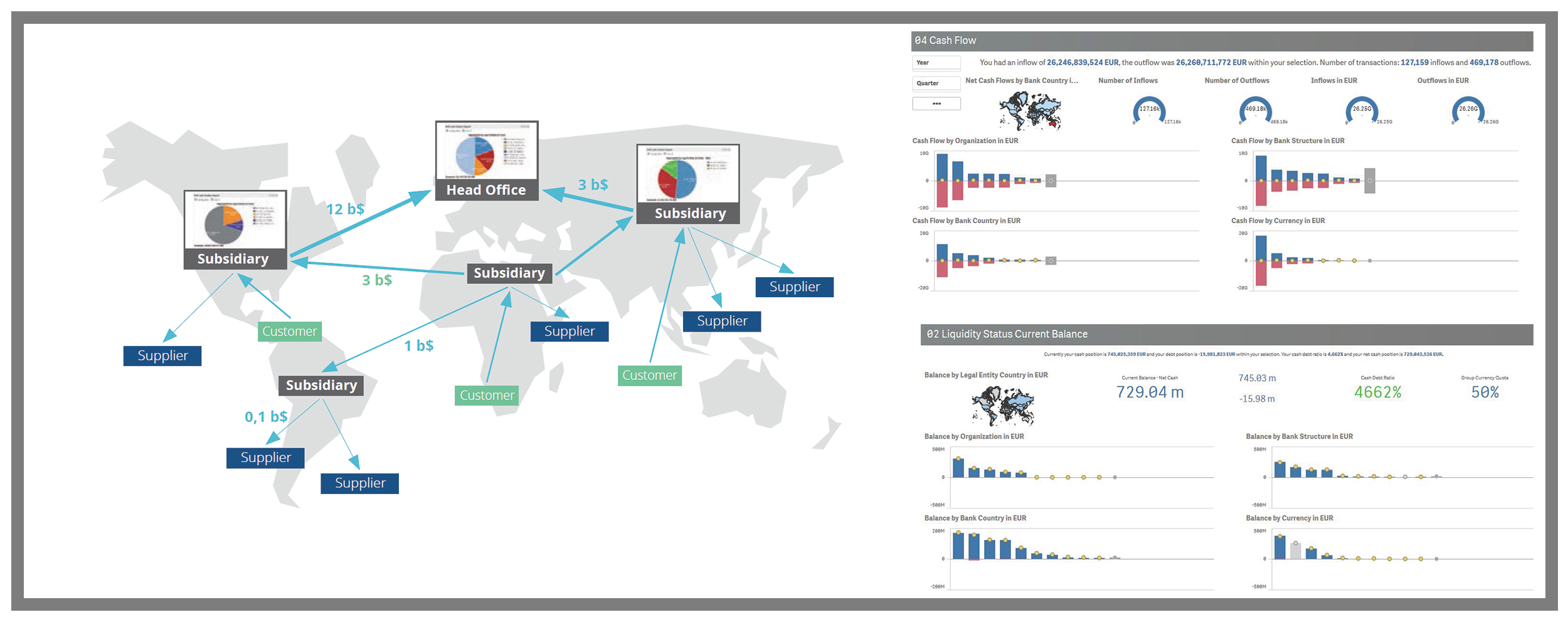

How do strategic professionals decide on the best path to success for their company? The key is in transparency and real-time reporting. If it comes to the responsibility of the treasurer or financial professional this means deciding about company-wide cash flow and liquidity levels, bank, customer and supplier relations and working capital.

How do strategic professionals decide on the best path to success for their company? The key is in transparency and real-time reporting. If it comes to the responsibility of the treasurer or financial professional this means deciding about company-wide cash flow and liquidity levels, bank, customer and supplier relations and working capital.

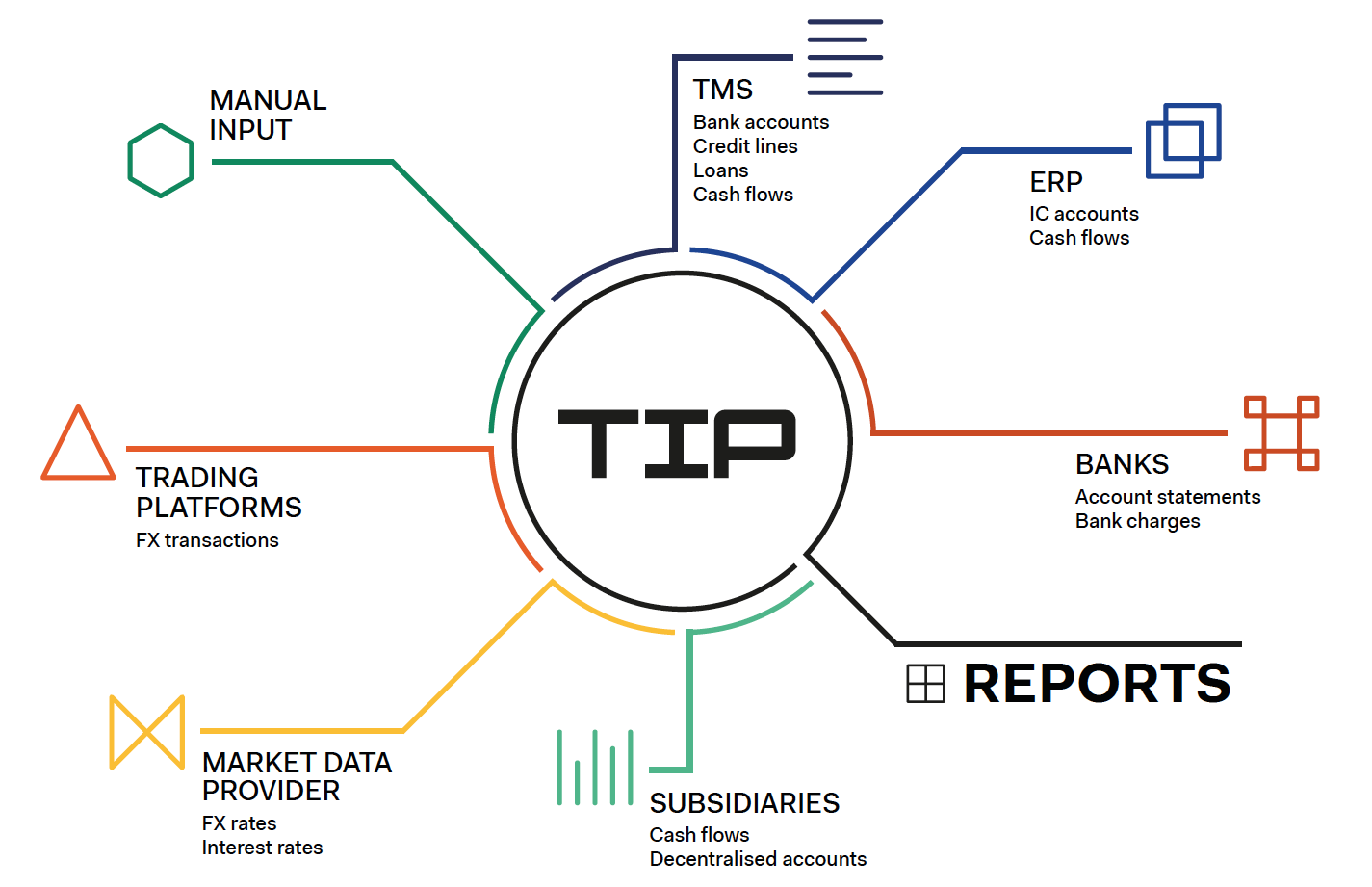

Hubert Rappold from TIPCO Treasury & Technology, puts the case for a treasury information platform (TIP), which acts as an information hub for the treasury department and reduces companies’ reliance on “Excel-based monstrosities” that are doomed to fail.

Hubert Rappold from TIPCO Treasury & Technology, puts the case for a treasury information platform (TIP), which acts as an information hub for the treasury department and reduces companies’ reliance on “Excel-based monstrosities” that are doomed to fail.

Hubert Rappold – CEO at

Hubert Rappold – CEO at