7 reasons why you should do e-invoicing too

| 30-6-2017 | Mark van de Griendt | PowertoPay – UnifiedPost – Sponsored content |

E-invoicing is more than just a PDF that you send via e-mail. It’s a fully-automated process that enables receivers to get the invoice directly into their financial system. In this blog our expert Mark van de Griendt van Power toPay/Unified Post has summed up some of the key benefits for senders and receivers of electronic invoices.

E-invoicing is more than just a PDF that you send via e-mail. It’s a fully-automated process that enables receivers to get the invoice directly into their financial system. In this blog our expert Mark van de Griendt van Power toPay/Unified Post has summed up some of the key benefits for senders and receivers of electronic invoices.

Key benefits

1. Shorter payment periods: Since with e-invoicing invoices are being processed faster, they can be paid sooner. E-invoices are directly sent to the financial system, which make the chance that they end up in the wrong hands almost impossible.

2. Lower costs, fewer actions: Saving money on things as paper, ink and post stamps. Sending a paper invoice is 57% more expensive than e-invoicing and receiving a paper invoice is even more than 60% more expensive than receiving an e-invoice (Billentis).

3. E-invoice is delivered directly with confirmation of reception: Since you can track whether the invoice is delivered or not, it’s easier to have a clear insight of the status of your invoices sent. Now that you know for sure that the receiver actually received their invoice, you can confidentially do a follow up (if not automated).

4. Contributing to durability: Of course less paper is good for the environment. An e-invoice solution will remove at least 80% of paper from most accounting departments. Replacing unnecessary waste of paper by electronic invoicing, will save a lot of paper which means more trees.

5. No more need of manual input or scan recognition software

The the e-invoices are automatically loaded into financial system of the receiver. That is why manual input is not necessary anymore since all the data of the invoice are correctly loaded into the position where it needs to end up at. Scan recognition software is basically built in e-invoicing, since data is automatically recognized.

6. Safety – less chance on “ghost invoice”: A ghost invoice means that the invoice is fake. It’s an invoice for services or products which have never been delivered. The e-invoices are automatically checked on authenticity.

7. Clear insight into business processes: The financial department is very important to a business When it’s a mess, it’s stressful for the employees but it’s also bad for the prospects of the company. E-invoicing takes this mess away, since invoices cannot go wandering around ending up at the wrong persons. A clear and solid insight into the status of all invoices is a clear and solid insight into a company’s business processes.

Mark van de Griendt – Cash Management Expert at PowertoPay

Mark van de Griendt – Cash Management Expert at PowertoPay

[button url=”https://www.treasuryxl.com/community/experts/mark-van-de-griendt/” text=”View expert profile” size=”small” type=”primary” icon=”” external=”1″]

[separator type=”” size=”” icon=””]

More articles from this author:

PSD2 is coming soon: Some information about PSD2 summed up.

[separator type=”” size=”” icon=””]

In their first session

In their first session

The main task of a treasurer is linked to cash management and short term funding and investments. This is the common practice in the Dutch corporate market, but this is by far not the right view on treasurer’s tasks and responsibilities. In the UK and USA the treasury function is more based on a position close to the CFO, being responsible for the corporate financial strategy and being an advisor for the financial framework of a company. A treasurer is more than a operational position in the company.

The main task of a treasurer is linked to cash management and short term funding and investments. This is the common practice in the Dutch corporate market, but this is by far not the right view on treasurer’s tasks and responsibilities. In the UK and USA the treasury function is more based on a position close to the CFO, being responsible for the corporate financial strategy and being an advisor for the financial framework of a company. A treasurer is more than a operational position in the company.

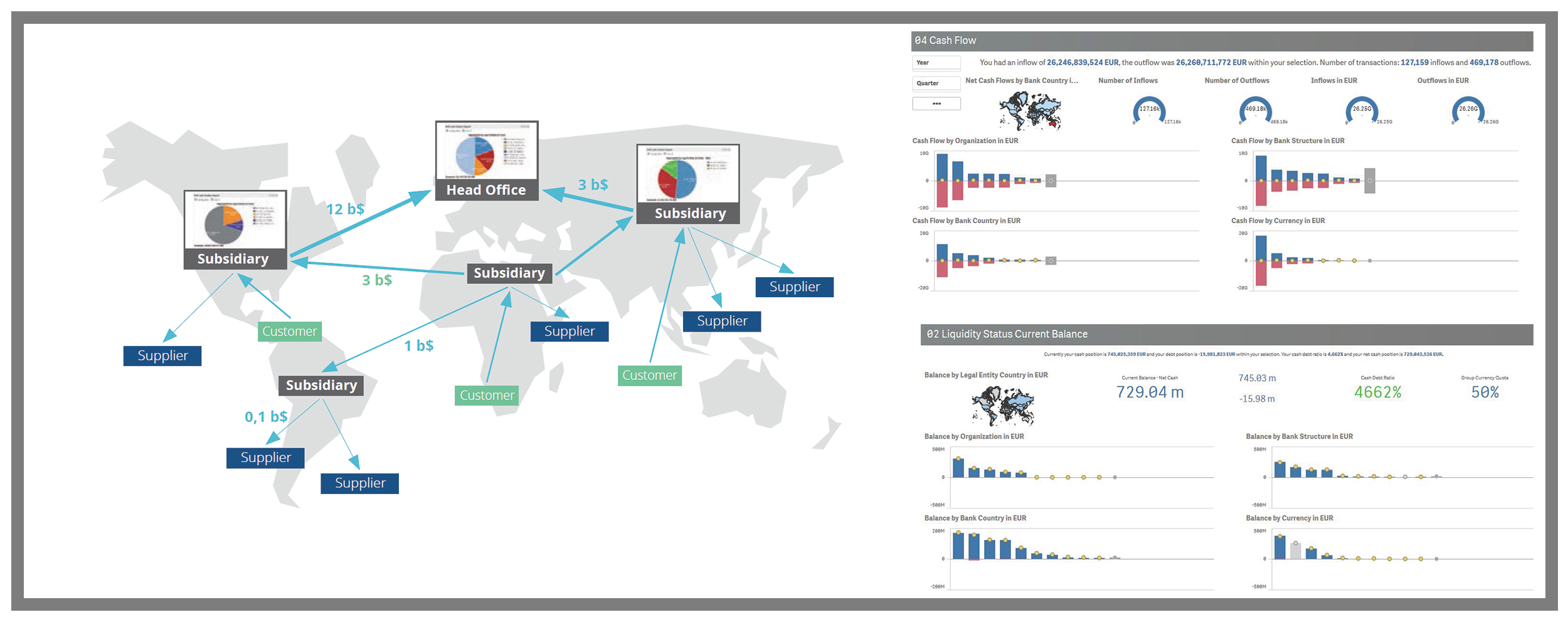

How do strategic professionals decide on the best path to success for their company? The key is in transparency and real-time reporting. If it comes to the responsibility of the treasurer or financial professional this means deciding about company-wide cash flow and liquidity levels, bank, customer and supplier relations and working capital.

How do strategic professionals decide on the best path to success for their company? The key is in transparency and real-time reporting. If it comes to the responsibility of the treasurer or financial professional this means deciding about company-wide cash flow and liquidity levels, bank, customer and supplier relations and working capital.

GMU, het formaat wat al jaren door ING wordt gebruikt als formaat voor de bankafschriftinformatie, wordt vanaf 1 juli niet meer door ING aangeboden. Dit formaat wordt al tientallen jaren door ING geleverd en wordt ‘ingehaald’ door formaten die uitgebreidere (incasso) informatie kunnen geven. Wat houdt deze verandering precies in? En wat zijn oplossingen voor het verdwijnen van GMU?

GMU, het formaat wat al jaren door ING wordt gebruikt als formaat voor de bankafschriftinformatie, wordt vanaf 1 juli niet meer door ING aangeboden. Dit formaat wordt al tientallen jaren door ING geleverd en wordt ‘ingehaald’ door formaten die uitgebreidere (incasso) informatie kunnen geven. Wat houdt deze verandering precies in? En wat zijn oplossingen voor het verdwijnen van GMU? GMU-converter

GMU-converter