Cash flow forecasting – more than just safeguarding liquidity

| 4-6-2018 | Gerald Dorrer | TIPCO Treasury & Technology GmbH |

“We don’t need cash flow forecasting” – statements like this are frequently heard at companies with significant cash reserves. They often highlight concerns about major internal expenses as capturing the relevant data can tie up significant resources. Modern cash flow forecasting, however, is about far more than just safeguarding against insolvency. And using up-to-date technologies only minimal efforts are needed to implement a forecast that will provide you with an array of insightful data.

“We don’t need cash flow forecasting” – statements like this are frequently heard at companies with significant cash reserves. They often highlight concerns about major internal expenses as capturing the relevant data can tie up significant resources. Modern cash flow forecasting, however, is about far more than just safeguarding against insolvency. And using up-to-date technologies only minimal efforts are needed to implement a forecast that will provide you with an array of insightful data.

The easy way to achieve modern forecasting

Many of the data needed for cash flow forecasting already exist in various systems. ERP systems are a particularly efficient data source. For example, this is where you’ll find all of your receivables and payables, including the associated due dates and terms of payment. These data alone will already provide much of what you need. You can also find other influential factors here such as the volumes of regular salary payments. Modern forecasting systems already come complete with an interface to ERPs, making it possible to import these data at the press of a button and take them into account in your forecasts.

Another helpful tool is predictive analytics. Although the statistical methods which predictive analytics are based on have already existed for quite some time, modern technologies now make it possible to use these in practice. Predictive analytics is the key to leveraging historical data to predict future developments with an amazing degree of accuracy. A good example of the advantages offered by this procedure is in the case of a company with seasonal fluctuations in terms of its revenues. If you already have a target figure for revenues in the coming year, then predictive analytics will be able to rapidly and accurately break this down into sales for the individual months. But far more complex scenarios are also conceivable, such as the early identification of trends by means of automated analyses of social media data which can ultimately be translated into cash flows.

Flexibility

But which factors characterise a modern forecasting system?

Besides the criteria mentioned above (a connection to existing data sources and predictive analytics), flexibility is the most important factor – in all respects.

A modern system will allow you to freely define the structure of your forecasting within just a few minutes. Regardless of whether you need standard forecasting of operational and non-operational payments and financial cash flows or whether your company mainly engages in project-related business, you should be able to freely define the structure and the details of your cash flow categorisation. On the other hand, it should also be possible to rely on templates provided by the system in order to start the process using a structure tailored to your specific industry.

At the same time, modern systems also allow you to be flexible in terms of your forecasting horizon. Everything should be possible: from short-term day-by-day forecasting required by banks for companies facing critical cash flow bottlenecks, to long-term forecasting with a horizon of several years. Top-of-the-line systems can even offer you the option of mixing daily, weekly and monthly data in order, for example, to forecast the next seven days on a daily basis, the following twelve weeks on a weekly basis and the remaining nine months on a monthly basis. You can specify how the weekly and monthly values are automatically distributed. This means that you are free to define how previous figures with a low degree of granularity appear at the weekly or daily level after the next data rollover.

Flexibility is also required when it comes to displaying the data. Modern systems offer you several features which enable you to investigate the causes of significant differences between the current and earlier forecasts. For example, switch between the various levels of granularity, whether in terms of the structure or the timeline, or compare forecast and actual figures, or even forecasts from different points in time. Thanks to these flexible display options, expensive analysis tools are no longer necessary; all you need to do is take a quick look at your system.

More than just safeguarding liquidity

The primary purpose of forecasting of course remains ensuring sufficient liquidity. Based on your current cash reserves, the cash flows captured for future time periods are aggregated to provide you with the forecast of cash available at the end of every period. This makes it possible to quickly spot cash bottlenecks.

If your system also offers you the option of managing your credit facilities and their due dates, and integrating these into your cash flow forecasting, then this will enable you to quickly determine when credit lines will need to be drawn on or when they will need to be increased. This is just one of the many aspects which make it clear how significantly you can be supported by a well-designed system.

Systems which also permit you to forecast on a currency-differentiated basis offer considerable additional benefits. This feature will allow you to capture all cash flows in the original transaction currency. The advantage here is that, as soon as you have prepared the forecast, you not only have an overview of the development of liquidity but also of your FX risk exposures. If your system also allows you to manage FX hedge transactions, a comparison of FX payments and these hedge transactions will enable you to determine your unhedged FX exposure in no time at all. The latest systems can even automatically generate hedge proposals based on the unhedged exposure which are then automatically forwarded to your trading system in a workflow-based process once these have been confirmed and approved.

Conclusion

Technological progress has made preparing a cash flow forecast easier today than ever before. Even if no liquidity bottlenecks are currently likely at your company, due to the ongoing reduction in the expenses involved, it nonetheless makes little sense to take unnecessary risks and to pass up on the advantages that comprehensive cash flow forecasting offers.

Gerald Dorrer – Manager TIPCO Treasury & Technology GmbH

Content originally posted on Cash & Treasury Management File on 26/3/2018

[separator type=”” size=”” icon=””]

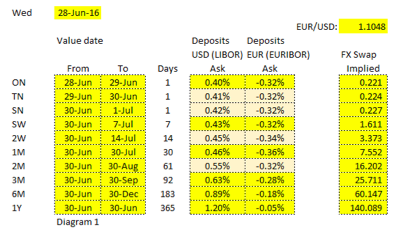

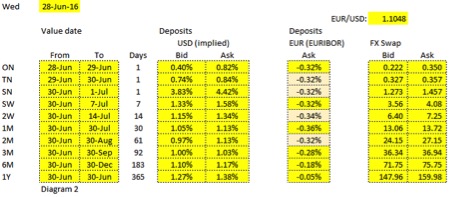

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows:

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows: e are looking at a single day FX swap, the annualized rate could swing a lot.

e are looking at a single day FX swap, the annualized rate could swing a lot.

There are many instruments that can be used to obtain short term funding. We have touched on some of them earlier in this series. This article is all about lines of credit. These are normally provided by banks of other financial intermediaries and help corporates with their short term funding needs. At first glance is might appear to be the same as a short term loan, but there are some clear differences. Normally, the financial institute that is the counterparty, will provide you with a line of credit – after appropriate inspection – which sets a specific limit on the amount of credit to be extended. Let us see how this works.

There are many instruments that can be used to obtain short term funding. We have touched on some of them earlier in this series. This article is all about lines of credit. These are normally provided by banks of other financial intermediaries and help corporates with their short term funding needs. At first glance is might appear to be the same as a short term loan, but there are some clear differences. Normally, the financial institute that is the counterparty, will provide you with a line of credit – after appropriate inspection – which sets a specific limit on the amount of credit to be extended. Let us see how this works.

When they hear e-invoicing, companies often think that this is sending invoices by e-mail. However, e-invoicing is more than that. Not only sending the invoice is part of this, but also the electronic booking, payment and collection of the money belongs to this process. Electronic invoicing leads to a major save of costs. For the sender, but especially for the receiver. Since e-invoicing is digitalizing invoicing for the sender as well as the receiver, a PDF-invoice is not seen as electronic invoicing.

When they hear e-invoicing, companies often think that this is sending invoices by e-mail. However, e-invoicing is more than that. Not only sending the invoice is part of this, but also the electronic booking, payment and collection of the money belongs to this process. Electronic invoicing leads to a major save of costs. For the sender, but especially for the receiver. Since e-invoicing is digitalizing invoicing for the sender as well as the receiver, a PDF-invoice is not seen as electronic invoicing.