4 financiële problemen die bedrijven in gevaar kunnen brengen

| 19-12-2016 | Schenkels | Pavey | FM.nl |

Op FM.nl (Financieel Management) kunt u een artikel vinden over de vier financiële problemen, die de continuïteit van een bedrijf in gevaar kunnen brengen. Dit onderwerp werd uitvoerig besproken tijdens een opleiding risicomanagement van Alex van Groningen.

Op FM.nl (Financieel Management) kunt u een artikel vinden over de vier financiële problemen, die de continuïteit van een bedrijf in gevaar kunnen brengen. Dit onderwerp werd uitvoerig besproken tijdens een opleiding risicomanagement van Alex van Groningen.

Het artikel gaat uitgebreid in op de vier problemen. Hier volgt een korte samenvatting:

1. Acuut probleem (illiquiditeit)

Bedrijven gaan vaak failliet, omdat ze geen cash meer hebben. Het gaat mis als er onvoldoende cash is om aan kortlopende financiële verplichtingen te kunnen voldoen. Met het werkkapitaal kunnen zich verschillende problemen voordoen:

● De hoeveelheid vlottende activa als percentage van de balans loopt te hoog op.

● Het probleem van onbeheersbare groei: vanwege snelle groei loopt de debiteurenpost te snel op.

● Wanneer een economische crisis uitbreekt, zoals de kredietcrisis van 2008, wordt liquiditeit schaars.

● Het grootste probleem ontstaat wanneer de cashflow snel daalt bij een achterhaald businessmodel terwijl de kosten/verplichtingen grotendeels hetzelfde blijven.

Je kunt werkkapitaal beoordelen met verschillende kengetallen: current ratio, quick ratio en netto-werkkapitaal. Echter, deze getallen zijn beperkt betrouwbaar omdat het momentopnamen zijn.

2. Chronisch probleem (organisatie is onrendabel)

Een onderneming kan jarenlang verlies lijden, maar toch blijven voortbestaan zolang er maar geld is. Wanneer de geldkraan wordt dichtgedraaid door de kredietverstrekker kan een chronisch probleem ineens een acuut probleem worden. Dit geldt bijvoorbeeld voor veel retailketens op A-locaties, die vanwege de enorme impact van internetwinkelen onrendabel werden. Terwijl de omzet per winkel terugliep bleven de vaste lasten, zoals huur, salaris en afschrijvingen, gelijk.

3. Structureel probleem (insolvabiliteit)

Van insolvabiliteit spreek je wanneer er iets mis is met de vermogensstructuur van een onderneming. Hoe hoger de leverage – het vreemd vermogen – hoe lager de solvabiliteit. Het aantrekken van meer vreemd vermogen is niet per definitie verkeerd. Het kan ondernemingen in staat stellen te investeren en te groeien. Maar omdat het geld kost aan rente en risico’s met zich meebrengt moet er wel meer rendement tegenover staan.

4. Strategisch probleem (toekomstplannen)

Een onderneming heeft een strategisch probleem wanneer het management niet goed in zicht heeft hoe de markt veranderd en hoe de onderneming haar toekomstplannen daarop moet aanpassen. Dit probleem kun je niet uit de boekhouding halen. Volgens docent Jan Vis, een autoriteit op het gebied van waarderingsvraagstukken, is het van het allergrootste belang dat het management zich focust op het vergroten van de toekomstige geldstromen, want waarde ligt altijd in de toekomst en in het genereren van cash (geen winst).

Wij hebben twee van onze experts gevraagd om hierop commentaar te geven:

Boudewijn Schenkels:

De meeste bedrijven in problemen zijn inderdaad afhankelijk van overnames of te afhankelijk geworden van de standaard financieringsproducten van banken. Hoe langer hun financiële crisis voortduurt hoe eerder de bodem van de kas in zicht komt. Er wordt (nog) niet of te weinig gedacht aan de alternatieve onorthodoxe vormen zoals bijvoorbeeld crowd-funding. Banken worden hier steeds creatiever in en er ontstaan steeds meer netwerken. Out-of-the-box vormen die alle 4 de probleemgebieden kunnen tackelen of beheersen. Ook kom ik ook nog steeds bedrijven tegen waar vastgehouden wordt aan oude structuren in het kader van cash management. In het post-SEPA tijdperk zijn lijnen korter en is betalingsverkeer meer transparant en ontstaan er nieuwe producten. Om te komen tot deze nieuwe vormen is een afwijkende strategische visie nodig vanuit management. Streef er constant naar onderscheidend en denk na over hetgeen er verder in de wereld aan de hand is dat er onverwachte wendingen ontstaan. Kijk naar de politiek.

Senior Consultant Payments bij Payments Advisory Group

Lionel Pavey:

Hij reageert op het probleem illiquiditeit: Er zijn 2 stromen waar geld vaak vast zit – voorraden en debiteuren.

Voorraden

1) Plan de hele cyclus van levering tot verkoop

2) Hoe lang is de levertijd

3) Hoeveel ruimte nemen de goederen in beslag en heb ik genoeg ruimte

4) Zijn de voorraden snel bederfelijk

5) Hoeveel leveranciers zijn er

6) Zijn de goederen seizoensgebonden

7) Implementeren van “just-in-time” methodiek

Debiteuren

1) Facturen tijdig en correct versturen

2) Controleren en vermelding van juiste voorwaarden

3) 1 week na verzending controleren dat facturen zijn ontvangen bij debiteur

4) Bevestig met debiteur dat alle gegevens correct zijn

5) Bevestig met debiteur dat betaling vindt plaats op afgesproken datum

6) Alle contact met debiteur ten eerste via telefoon, daarna via email

7) Implementeren van een solide debiteurenbeheer

8) Altijd proactief actie ondernemen – niet wachten op debiteur

9) Laat verkoop afdeling weten de stand van zaken, maar laat verkopers nooit direct met klanten praten/onderhandelen over openstaande posten

10) Zorg voor alle nodige vaste gegevens van een debiteur – contact persoon, hoofd crediteuradministratie enz.

11) Uw klant is ook een mens – als een klant wordt op de hoogte gesteld van openstaande posten, dan realiseren zij dat U een goede beheersing hebben van alle organisatorische aspecten

Cash Management and Treasury Specialist – Flex Treasurer

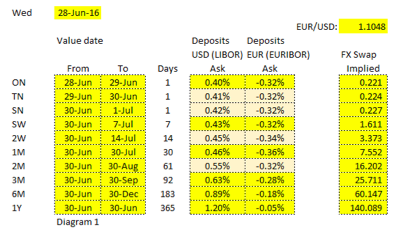

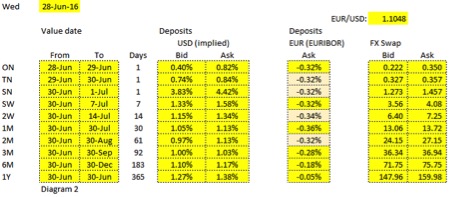

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows:

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows: e are looking at a single day FX swap, the annualized rate could swing a lot.

e are looking at a single day FX swap, the annualized rate could swing a lot.

Many CFO’s and Financial Managers would like to improve the cash awareness inside their companies. The most obvious action is to set up financial targets but how could a change of mindset be reached without new targets? One way is to see cash awareness as a product and to try to sell this product inside the company.

Many CFO’s and Financial Managers would like to improve the cash awareness inside their companies. The most obvious action is to set up financial targets but how could a change of mindset be reached without new targets? One way is to see cash awareness as a product and to try to sell this product inside the company.