Particularly with continued financial headwinds, accurate-as-possible cash forecasting and visibility are more critical than ever. But, according to a recent survey of hundreds of global treasurers, the process of generating forecasts has been either “somewhat difficult” or “extremely difficult.”

—

Jo Stevens, a senior product manager at GTreasury, wrote for Treasury & Risk on four specific best practices around how treasurers can improve cash forecasting and optimize their use of sophisticated forecasting technologies. Jo discusses how to capture more accurate data, how to best process that data with machine learning, how to approach cash visibility, and, crucially, how to continually adapt to meet ongoing forecasting challenges.

https://treasuryxl.com/wp-content/uploads/2022/07/gtreasury-200-21e.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-21 07:00:172023-06-28 09:38:55Zeroing in on 4 Specific Ways Treasurers’ Can Improve Cash Forecasting

That’s never been so important as in these times of rising interest rates, inflation, and supply chain shocks, when managing working capital is everyone’s concern.

From supply chain finance to accurate cash forecasting, solutions for every component of working capital management will be discussed on stage, demonstrated in our information area, and examined in our workshops at the world’s largest specialist working capital and supply chain finance event.

We’re delighted to return to Amsterdam for this one-day live event, with main stage keynote sessions, panel debates, and breakout workshops and demos.

If you’re interested in optimising working capital in your organisation, you need to join us in Amsterdam for the most productive day you’ve had in years.

Among the topics we will be covering are:

Cash forecasting and cash visibility

Payables finance

Receivables finance

Optimising receivables – get paid faster

Inventory management and inventory finance

Supply chain finance

‘Deep tier’ supply chain finance

Funding options for trade and supply chain finance

Using working capital tools for ESG objectives

Credit insurance

Disclosure rules on supplier finance

Ratings agencies and their view of working capital solution

USE YOUR COUPON CODE VIA TREASURYXL

Banks, fintechs, and other solution providers can get 25% off the cost of a ticket using this TreasuryXL code: TXL2225

Corporate Treasurers can apply for a free ticket using this Treasury XL code: TXL22CG

https://treasuryxl.com/wp-content/uploads/2022/07/WCFE-200x200-1-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-20 07:00:532022-07-15 10:49:09The Working Capital Forum Europe | Amsterdam 2022

Over the last weeks I saw the topic of fiscal expat rulings popping up in various media. The labour market is tight and governments want to support employers in attracting the best talent. Also internationally. In The Netherlands we have the “30% ruling” that takes care expats are not taxed over the first 30% of their income. Among politicians there is a discussion about this because, do we want to attract the best? Or do we consider lowering taxes for those who are already earning a lot not appropriate….?

https://treasuryxl.com/wp-content/uploads/2022/07/cb.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-18 07:55:502023-01-02 14:18:48Cross border movements of Treasurers and what drives them

A recent Refinitiv expert talk looks at the digital banking and fintech arena, unpacking the compliance challenges that dominate the sector and offering advice for a best-practice response.

https://treasuryxl.com/wp-content/uploads/2022/07/Ontwerp-zonder-titel-49.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-14 07:00:252023-01-09 16:54:215 steps to effective fraud prevention in fintech

Join this 15-minute bitesize webinar with a leading Kyriba Liquidity Management specialist to learn how artificial intelligence and machine learning are being applied in today’s liquidity management processes and how they will affect the future of treasury.

Emerging technologies are changing the way finance functions operate, opening up new opportunities for treasury and enabling teams to deliver increased value to the organization. As a new decade emerges, executives are looking to artificial intelligence and machine learning as a means for enhancing overall operations.

In this session he will discuss:

Difference between Business Intelligence, Artificial Intelligence and Machine Learning

Why are AI Solutions needed for best-in-class enterprise liquidity management ?

What Kyriba offers

Challenges of building AI forecasting solutions within an organization

https://treasuryxl.com/wp-content/uploads/2022/07/ky-web.png288304treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-13 09:25:512022-07-13 09:25:51The Role of AI in Liquidity Management | Webinar | July 21

The latest CompleXCountries report is based on two Treasury Peer Calls in which senior treasurers from Asia, the Americas and Europe discussed the latest bout of increased FX volatility, and the impact it is having on their hedging strategies. As to current volatility, some people are adjusting their strategies, but most prefer to stick with the approach which has already been defined.

FX – one of the biggest and most important challenges we all face. It has a direct impact on the business, and everyone has a view.

The calls (European morning and afternoon to accommodate Asia and the Americas) were to discuss the latest bout of increased FX volatility, and the impact it is having on people’s hedging strategies – if any. Unsurprisingly, it turned into a long discussion of the way different companies approach hedging. The report below is long and very varied – we managed to reduce it to 20 pages, but they are dense. As to current volatility, some people are adjusting their strategies, but most prefer to stick with the approach which has already been defined.

What is that approach? The participants came from a variety of different industries, and covered a broad range of different ways of handling the issue.

Everyone has a defined hedging approach, though most contain some degree of flexibility. So, if the approach is to hedge the next 6 months, for example, there may be leeway to go down to 4 months or up to 8.

Most people add their hedges via a layering approach, where they build up the hedge over time. This provides an average hedge rate, and avoids the risk of choosing a single point in time.

Everyone tries to match their hedges to the needs of the business. This involves co-ordinating with the business units to get their input on the ability to change prices, how long it takes to do so, etc.

Most companies have a centralised approach to hedging, but there is variety as to whether central treasury acts as and advisor, or as a decision maker. In most cases, this is decided by the company’s internal measurements and incentive system.

Several companies try to insulate the operating units from the effects of currency. This is done by various means: several participants operate re-invoicing centres, which invoice the operating entities in their own currencies, and manage the resulting exposures in the centre. One participant achieves the same result by levying a currency specific working capital charge on the operating units. The income from this charge is then used to pay for hedges – which may, or may not, actually be taken out.

In these cases, the centre usually operates as a profit centre – but with strong risk management disciplines to contain the danger of positions getting out of control.

One other approach is to fix a budget exchange rate for the coming year, and try to lock that in via hedges. There was a discussion as to whether this suits all businesses.

Most participants use forwards for hedging, with the choice of deliverable or NDF varying from one country to another. Several use options, though cost and accounting complexity were obstacles.

One participant has an approach which is built entirely around options, including a sophisticated trading strategy to reduce the cost of what they view simply as an insurance policy, like any other. This company is also very opportunistic, and will be active or inactive in the market according to their view of current pricing. This company is also private, and family owned, so they have a higher tolerance for earnings volatility than most – and they are not concerned about quarterly earnings announcements. They also have a relatively high margin business.

In this company, as in all others, this strategy is only possible because it has the understanding and buy-in of the management and the operating units. Every participant mentioned this as being key for success.

Generally, the percentage of hedging is fixed by policy. However, most participants exercise some judgement, based on the cost of hedging. This is particularly relevant for some emerging market countries, such as Brazil, Argentina and many African countries. The judgement as to what constitutes a hedge which is too expensive was often empirical, but the currencies which were left unhedged usually did not represent a significant exposure for the company.

Most participants prioritise balance sheet hedging over cash flow hedging, but some take the opposite approach. In all cases, the accounting treatment is a significant factor in determining the approach.

Bottom line: hedging and managing currency is one of the key competences of the treasurer. For many years to come, it will continue to be one of the areas where there is the biggest variation in approaches – and endless debates. If you have an approach which is well defined and which has been fully discussed with the business, there should not be any need to change it during a period of volatility – though it can be an excellent stress test!

[The full report can be downloaded FREE by corporate treasury practitioners, please Log in to your account to download (if you receive emails from us – use your email address to retrieve your password), if setting up a new account, please ask for the FX report in the comments and ComplexCountries will send you a copy]

https://treasuryxl.com/wp-content/uploads/2022/07/cxc-200-13e.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-13 07:00:582022-07-08 09:08:17Approaches to FX Volatility

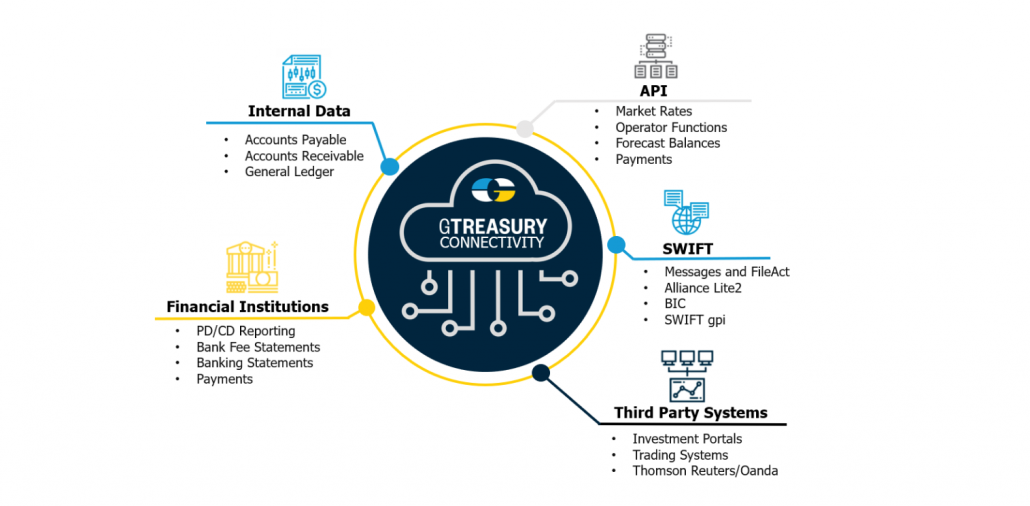

Workflow Brings in Third-Party Banking, Payments, and Financial Data

ClearConnect ensures the fidelity of data essential to treasurers and CFOs

CHICAGO, Ill. – July 12, 2022 –GTreasury, a treasury and risk management platform provider, today announced the launch of ClearConnect. Featuring more than 80 API calls in a dozen key categories, ClearConnect offers the most robust connectivity suite available to treasury teams and the office of the CFO. The solution provides immediate access to the comprehensive data required for confident and actionable treasury insights, and ensures the fidelity and security of that data through purpose-built connections bolstered by GTreasury’s support.

While “API” is becoming a buzzword often associated with data connectivity solutions, the terms are not synonymous. API connections are only as powerful as the underlying workflows that support them. Activating an out-of-the-box API is not an instant panacea for an organization’s data needs. Without the right underlying workflows, APIs not attuned to a business’s specific requirements will drop or fail to capture all the data sets necessary to power effective analytics and data lakes. Given the complexity of treasury and risk management, those missing insights can result in significant consequences for treasury teams and CFOs.

ClearConnect provides both the powerful underlying workflows and the multifaceted purpose-built API-enabled connectivity to ensure that data capture is consistently done correctly and thoroughly—providing all the analytics an organization needs from a particular connection. The solution creates certainty, security, and seamless connections by integrating all data from business systems and financial institutions, and is capable of combining connection types for uniquely complete data sets and data fidelity.

Specifically, ClearConnect creates value for treasury teams and the office of the CFO by delivering:

Secure connectivity across the financial value chain

Extensions to corporate treasury workflows

Access to specialist solutions within the integrated platform

Lower bank fee costs through seamless connectivity

Access to multiple innovative FinTech products and services

ClearConnect’s market-leading API catalog features over 80 API calls, augmented by host-to-host connectivity wherever needed to bolster capabilities. The solution enables robust functionality across a dozen categories, including payment approval rules, payment workflows, payments and templates, balances and transactions, general ledgers, deal management, bank accounts, bank account management, legal entities, forecasts, operators, and data extracts. ClearConnect’s flexible connectivity architecture uses best-in-class API-enabled connections to ensure fidelity and continuity of customers’ most vital data. Connectivity into Swift, Fides, and others provides a single source of truth and visibility into an organization’s cash and financial risk, and delivers transparent workflows for payments, bank file monitoring, and more.

GTreasury’s always-expanding partnerships with leading global financial institutions and market data partners ensure seamless bank and ERP connectivity, domestic and international transactions, and access to market insights. As client needs change, GTreasury’s active collaborations with product partners further ensure the creation and delivery of modernized products and services, securing ClearConnect’s place as a market-leading solution always aligned with customers’ current data requirements.

From risk management capabilities powered by Moody’s Analytics and KYOS, to market data provided by Refinitiv and Fenics MD, to banking, ERP, investments, and payments partners, ClearConnect now enables customers to wield the full power of the GTreasury ecosystem even more easily and completely.

“ClearConnect doesn’t just offer a significantly greater breadth of connectivity options than anything else available, it also underwrites those capabilities with foundational workflows for data integrity and ease of use,” said Pete Srejovic, Chief Technology Officer at GTreasury. “Investing in API technology only to realize that you are dropping crucial data is a nightmare that has come true for many CFOs and treasury teams. With today’s launch of ClearConnect, we’re proud to offer not only the largest and most powerful API connectivity solution on the market, but one that customers can entrust to deliver absolute data integrity along with the comprehensive and future-proof solutions of the GTreasury ecosystem.”

About GTreasury

GTreasury believes there is opportunity in complexity. We connect treasury and finance teams with industry-leading experts, technology solutions and untapped possibility. By simplifying complexity, teams can unleash their organization’s potential to gain strategic advantages and grow. GTreasury helps organizations reach that potential by connecting treasury and digital finance operations through a world-class SaaS treasury and risk management platform and integrated ecosystem where cash, debt, investments, and exposures are seamlessly managed within the office of the CFO. GTreasury delivers intelligent insights, while connecting financial value chains and extending workflows to third-party systems, exchanges, portals, and services. Headquartered in Chicago, with locations serving EMEA (London) and APAC (Sydney and Manila), GTreasury’s global community includes more than 800 customers and 30+ industries reaching 160+ countries worldwide. Visit GTreasury.com

https://treasuryxl.com/wp-content/uploads/2022/07/gtreasury-200-12-7.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-12 07:00:302022-08-08 14:25:22GTreasury Launches New Connectivity Suite for Treasurers

Recently, treasuryXL partnered with Nomentia on a live webinar on how successful master data management can help you secure financial processes.

Watch the recording of this session for free now by clicking on the image below!

In this webinar, we discussed how you can manage your Master data in a safe way, how you can prevent fraud and sanction risks through the management of this data, and the subsequent processes that make use of your master data. This ranges from the creation of counterparties in your ERP to the safeguard checks in your payment process and system.

More specifically, we will discussed the following topics:

Introduction to Master Data management

Managing the counterparty Master Data in your ERP

Trends that companies face related to Master Data

High-risk processes using your master data

Steps to create a safe and secure culture within your company

Setting up appropriate processes and systems to enable security

https://treasuryxl.com/wp-content/uploads/2022/07/nomentia-webinar-recording.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-12 07:00:142022-08-08 14:27:01Recording Webinar | How successful master data management can help you secure financial processes?

As a CFO, you are aware of the benefits of FX hedging for treasury. However, are you also aware of the macro-level advantages for your company and its value?

A new CurrencyCast series has just been introduced by Kantox. They examine five ways that efficient currency management may benefit your entire business in the first episode of their CFO Edition miniseries, including how to incorporate it into your strategy and how to decrease cash flow fluctuation. Watch below the video or read the corresponding blog.

In the first edition of CFO Perspectives, we’ll draw from our work with CFOs to explore three ways senior finance executives can make currency management a winning growth and cost-saving strategy for their business.

Looking at the concerns expressed by CFOs in most risk management surveys, a number of familiar themes seem to reoccur: the importance of cash flow forecasting and monitoring, the centrality of FX risk management and the ongoing digitisation of treasury processes

Yet, this picture is far from complete.

Ultimately, among the tasks assigned to CFOs, there is the need to make a contribution toward enhancing the value of the business. But what is the role —if any— played by currency management in that regard? Answering this question allows us to single out three strategic contributions of currency management that CFOs should prioritise.

Value and FX hedging: time for a reassessment

Does currency management create value? The traditional view has been ambivalent: a ‘glass half full, half empty’ kind of appraisal. While the benefits of hedging FX have never been in dispute, the problem lies with the perceived high costs of currency management.

This is precisely where things are changing—and quite fast. Digital, API-based technology is putting to rest the notion that currency management is always a costly, resource-intensive task. Meanwhile, Multi-Dealer Platforms (MDPs) such as 360T, embedded in these solutions, sharply reduce trading costs.

CFOs: three strategic contributions of currency management

(1) Create opportunities for growth

Feeling concerned about exchange rate risk, managers may neglect the growth opportunities that come from ‘embracing currencies’. Buying and selling in more currencies allow firms to capture FX markups on the selling side while avoiding markups on the contracting side. Two examples will suffice:

(a) On the selling side: In e-commerce setups, currencies can be leveraged to increase direct, high-margin sales on company websites with many payment methods. Multi-currency pricing is the secret weapon for reducing cart abandonment, which still stands at about 77% globally.

(b) On the buying side: Buying in the currency of their suppliers allows firms to (1) Avoid inflated prices charged by suppliers who seek to manage their own FX risk; (2) Widen the range of potential suppliers by putting them in competition; (3) Obtain extended paying terms.

By taking FX risk out of the picture, currency management enables firms to reap these and other margin-boosting benefits of using more currencies in their day-to-day business operations. Ultimately, it is about removing the disincentives that prevent firms from ‘embracing currencies’.

(2) Provide more informative financial statements

Informative financial statements allow investors to assess the quality of management by removing noise from the process. To the extent that the variability in net income is perceived as a measure of management quality, effective currency hedging creates a sense of discipline in the eyes of investors.

The good news for CFOs is that technology is making great strides in cost-effectively managing the accounting-related aspects of currency management. Here are two examples:

Traceability and Hedge Accounting. The perfect end-to-end traceability made possible by automated solutions eases the costly and time-consuming process of compiling the required documentation for Hedge Accounting.

(3) Lower the cost of capital

Companies can reduce cash flow variability thanks to a family of automated hedging programs and combinations of hedging programs, including layered hedging programs that make it possible to maintain steady prices in the face of adverse currency fluctuations.

In challenging times, when the availability of external financing at a reasonable cost is scarce —an all too common occurrence in years of pandemics and wars—reduced cash flow variability makes it possible for companies to execute their business plans and meet all cash commitments.

An impaired capacity to raise financing has implications in terms of valuation, especially for smaller businesses. This ‘cost’ has been variously measured, with some estimations ranging from 20% to 40% of firm value. Currency management enhances the capacity to raise finance and, by extension, lowers the cost of capital and boosts firm valuation.

A wide range of opportunities to create value

We have singled out three major contributions of currency management in terms of creating value for the business: (1) stimulating growth while protecting and enhancing profit margins; (2) lowering the variability of cash flows; (3) presenting more informative financial statements. We can mention even more benefits:

Taxation is optimised as smoother earnings reduce the tax burden when higher levels of profits are taxed at a higher rate.

Capital efficiency is raised when pricing with the FX rate improves the firm’s competitive position without hurting budgeted profit margins.

While most of these advantages have been known by CFOs for many years, there is a new factor to consider: they can be implemented with Currency Management Automation solutions that remove most of the resource-consuming, repetitive and low-value tasks performed by the finance team, eliminating unnecessary operational risks along the way.

With an added bonus: by leveraging currencies, CFOs have the opportunity to take decisive steps in terms of digitisation. According to a recent HSBC survey, digitisation is seen as the most positive factor by 84% of CFOs overall, as they expect investments in digital technology to have a “positive impact on their business”, with more than half of them expecting it to give the business model “a large boost”.

https://treasuryxl.com/wp-content/uploads/2022/07/kantox-cfo-200.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-05 07:00:052023-03-03 12:11:13CFO Perspectives: 3 ways CFOs can use currencies to boost their business’s value

Boost your professional skills, knowledge and expertise in Treasury Management & Corporate Finance thanks to these high-level modules. Complete the programme and be awarded with the title of Registered Treasurer (RT).

The Vrije Universiteit Amsterdam invites you to join the Online Open Evening on Tuesday, 5 July 2022.

The postgraduate Executive Treasury Management & Corporate Finance programme combines two finance disciplines which largely overlap and are inextricably connected: Treasury Management and Corporate Finance. For this reason, it is a unique programme both in the Netherlands and abroad. It has now been running for more than 20 years at Vrije Universiteit Amsterdam. This postgraduate programme aims to promote development as an academic professional through a mix of academic theory and case studies of real issues in the field of treasury management and corporate finance.

Upon successful completion of this 18-month programme, you will be awarded with the title of Registered Treasurer (RT), a well-known and widely recognised title within the treasury professionals’ community. Exemptions apply to alumni of Dutch RC and RA programmes.

There are five key benefits of attending this programme

Broaden the perspective on the corporate treasury and finance disciplines that all-round corporate treasurers and finance professionals should master

Gain and master hands-on knowledge crucial in the daily practice thanks to a balanced mix of academic and professional expertise

Career development opportunities in a different setting thanks to the participation in the Thursdays lectures, leading to new ideas, insights and development

Interactive sessions are an added value of the programme, which explain and apply the main principles to professional practice through practical examples and business cases

Connect with the treasury community and fellow participants and build your own professional network

The programme Treasury Management & Corporate Finance at a glance

Start date: September 2022

Duration: 1,5 year (part-time)

Modules: 6

Time Investment: 130 hours per module including 8/9 weeks of four-hour teaching sessions and approximately 10 hours of self-study per week.

Tuition fees: € 22,500

Lectures: Thursdays

Form: Physical classes (VU Amsterdam follows the advice of the RIVM for public health).

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.