Recap & Recording: The New Way Treasurers Are Managing Payables – Old Tool, New Tricks

11-03-2026 | In our live session with ETR Digital we explored how working capital notes and a digital marketplace can transform payables and supplier financing.

11-03-2026 | In our live session with ETR Digital we explored how working capital notes and a digital marketplace can transform payables and supplier financing.

30-03-2023 | Have you ever sat staring at a huge data set, perhaps spread across many files or sources, wondering how to collect and extract the valuable insights hidden within it?

06-02-2023 | Anastasia Kuznetsova | treasuryXL | LinkedIn |

The recent increase in ESG awareness among consumers and investors, along with regulatory pressure, has prompted companies around the world to incorporate ESG aspects into their business models in order to become sustainable.

However, a transition to more sustainable operations is not possible without new financing. Thus, Corporate Treasurers can significantly help companies to achieve their ESG goals by raising funds for the company’s sustainable initiatives. This can be done through the creation of a sustainable finance framework, which has gained popularity among companies in recent years.

A sustainable finance framework aims to align financial decision-making with the principles of sustainable development. The framework outlines how a company uses environmental, social, and governance (ESG) factors in its financing, refinancing, and investment processes. As a starting point, corporations typically establish a sustainable finance framework to arrange debt financing for a certain group of projects with positive environmental or social benefits. Many organizations set up their sustainable finance framework in accordance with international guidelines such as the Green Bond Principles (GBP) or Social Bond Principles (SBP), which support the issuance of ESG-related debt.

The use of Proceeds clause defines categories of projects for which a company can use debt proceeds that were raised under its sustainable finance framework. For instance, the Framework of a property developer may cover the issuance of green and social bonds for three project categories:

Each project category will also have specific ESG criteria that will help to identify truly sustainable investment opportunities eligible for sustainable financing. For example, a project category “acquisition/development of low carbon buildings” may only allow spending debt proceeds on the acquisition of buildings with an energy efficiency rating of A. Projects that do not fall under eligible project categories, or projects that do not satisfy the established ESG criteria within each project category, will not receive sustainable financing and, thus, will not be undertaken by the company.

Another crucial component of a sustainable finance framework is project evaluation and selection. Corporate Treasurers should establish a method for determining whether new projects available for the company fit eligible project categories and, therefore, can be adopted. All selected projects included in a sustainable finance framework should be reviewed on a periodic basis and before new financing is raised. As a rule, a full list of eligible projects is examined and approved by the CFO to confirm that they meet the ESG criteria of the Framework and, thus, can receive financing.

After the sustainable financing is raised, Treasurers should ensure that funds are properly allocated and used in accordance with the “use of proceeds” clause. Thus, the sustainable finance framework should specify how a company will track the disbursements and allocation of debt proceeds among eligible projects.

The fourth component of the sustainable finance framework is the periodic disclosure of debt-related and project-related information. As long as a company has some outstanding debt raised within its sustainable finance framework, it should disclose, at least annually, the total amount of ESG debt raised, the remaining outstanding proceeds and the allocation of the proceeds across eligible projects. Such disclosures will help the company’s debtholders to understand how and to what extent their capital has been deployed by the organization.

Companies should also evaluate the environmental/social impact of funded projects via verifiable Key Performance Indicators (KPIs). For instance, a property developer can measure the environmental impact of projects under the “acquisition/development of low carbon buildings” category by energy consumption (kWh) and/or energy intensity (kWh/m2) KPIs. Impact reporting is crucial to assess whether the projects that received sustainable financing have achieved the expected positive environmental/social benefits.

The last attribute of the sustainable finance framework is independent external assurance. This step is needed to confirm the credibility of the established Framework as well as attest the compliance of the debt issuance process with the principles of international guidelines adopted by the company as a foundation for its sustainable finance framework.

The ultimate objective of a sustainable finance framework is to drive the financing of all corporate activities that align with the company’s sustainability goals. As such, Treasurers should gradually broaden the Framework by incorporating other sustainable finance instruments, such as convertible green bonds or sustainability-linked revolving credit facilities, to finance a diverse range of sustainable initiatives that support a company’s transition towards more sustainable operations. Over time, the Framework should be continuously expanded to include the development of new products/services and other sustainable business activities, instead of being limited to the financing of specific project categories that were initially defined in the use of proceeds clause.

The implementation of the sustainable finance framework can potentially result in the following benefits for the company.

By inclusion of ESG factors in the financial decision-making process, the Framework ultimately forces companies to consider environmental and social risks as well as their interdependences when evaluating investment opportunities. This enables businesses to receive a more complete picture of their risk exposures and, therefore, timely put in place adequate risk management tools that are required to keep company’s exposure to risks at an acceptable level.

The improved risk management that accounts for ESG-related risks is also likely to increase the confidence of capital providers in the company’s ability to survive in the long-term and remain profitable during challenging times. This, in turn, might improve a company’s credit rating, decrease the cost of capital, and enable businesses to obtain new financing on more favourable terms.

Sustainable finance has gained significant momentum in recent years. Therefore, companies that are perceived as environmentally and socially responsible are more likely to receive investment from impact-oriented investors and financial institutions. Thus, the implementation of the sustainable finance framework can increase a company’s access to capital and provide new source of financing in the face of ESG-oriented investors.

The implementation of a sustainable finance framework also demonstrates a company’s commitment to sustainability, which can lead to a better reputation among stakeholders, and enhance the company’s credibility and trust. This may translate into a wider pool of investment options and stronger relationships with suppliers, customers, and other stakeholders.

Thank you for reading!

01-12-2022 | Anastasia Kuznetsova | treasuryXL | LinkedIn |

The expression “Money makes the world go round” probably underscores the importance of the finance community for the transition to a greener economy. Financial market participants can significantly accelerate the transition to a more sustainable world by directing capital flows to the most sustainable projects, assets and companies.

Corporate Treasurers can have a substantial impact on business sustainability by allocating capital to green projects as well as incorporating ESG factors in their risk management processes. Below I will summarize some of the instruments Corporate Treasurers could use to support companies on their way to sustainability.

ESG debt is perhaps one of the most common instruments that may help companies to meet their ESG goals. For instance, to achieve environmental objectives, some companies issue green bonds. The proceeds from green bonds can only be spent on funding climate-related projects, including renewable energy, construction of green buildings, installation of air pollution control systems and etc. Most green bonds issued are “use of proceeds” bonds, which determine a range of eligible green project categories for which capital raised can be used. These bonds are also backed by the entire balance sheet of the issuer. Project bonds are another popular type of green bonds for which the proceeds are earmarked for specifically identified projects and are exclusively backed by the project’s assets. While green bonds might be more relevant for large public companies, private companies may still add ESG debt in their capital structures by arranging green loans which serve the same purpose as their public market bond equivalents.

Another type of ESG debt is sustainability-linked loans (SLLs), which are even more popular than green bonds and loans. The rise in popularity of SLLs may probably be explained by higher flexibility when it comes to the use of debt proceeds. Hence, the proceeds from SLLs can be spent on general corporate purposes but not exclusively earmarked for environmental projects. Moreover, SLLs are normally structured in the form of revolving credit facilities, which enables companies to fund their daily liquidity needs if they encounter a working capital deficiency. The purpose of SLLs from an ESG perspective is to encourage companies to achieve sustainability as quickly as possible. This is done by linking loan margin to a borrower’s sustainability performance. At first, sustainability performance targets (SPTs) for the borrower are established. After that, the borrower’s progress toward SPTs is monitored on annual basis via Key Performance Indicators (KPIs). If the targets are achieved, the loan’s margin will be reduced, enabling the borrower to benefit from lower interest payments. If the targets are missed, a step-up provision applies, increasing the loan’s margin and, thus, interest payments. Such an ESG Margin Ratchet provision incentivizes the borrower of SLLs to not only achieve but also maintain a certain level of ESG performance. The public markets equivalent of sustainability-linked loans is sustainability-linked bonds (SLBs) whose coupon payments are reduced (increased) if SPTs are met (missed).

On top of ESG-related loans and bonds, hybrid instruments such as green convertible bonds are becoming more and more popular. Thus, in 2020, Neoen, a French producer of renewable energy, issued €170M of the first ever green convertible bonds in Europe. This year, the company launched another €300M offering of green bonds convertible into new shares and/or exchangeable for existing shares.

Finalizing the topic of ESG debt, it is worth mentioning that when it comes to the EU’s finance providers, and particularly credit institutions who will soon have to disclose the percentage of green assets on their balance sheet under the EU Taxonomy, it is reasonable to expect that sustainability-linked debt will be favored by creditors. Specifically, being an underwriter of ESG debt could add prestige, and improve reputation and market positioning. In contrast, non-ESG debt may experience a pricing premium since such loans are likely to worsen the “greenness” of capital providers’ balance sheets.

Although currently ESG is not widely incorporated in foreign currency trades, some banks have already started to develop FX products that have a similar structure to SLLs. Such FX products will be linked to sustainability KPIs that will measure a company’s sustainability performance against pre-defined SPTs. If SPTs are successfully achieved, then a company may receive a rebate on its FX trades or a reduction in the required FX margin.

Sustainability-linked derivatives (SLDs) are another instrument that can be adopted by Treasurers to facilitate a transition of businesses to greener operations. SLDs are particularly relevant for companies, operating in “high-impact climate sectors” such as energy and agriculture. Cash flows of SLDs are connected to the sustainability performance of counterparties that is monitored via KPIs. Having met KPIs, a counterparty in a derivative transaction may receive a higher incoming payment, or be able to make a lower payment if the transaction results in a cash outflow. SLDs are OTC derivatives, meaning that counterparties can customise the derivatives’ terms and, thus, embed other ESG incentives, i.e. reduction in margin/spread, or payment of rebate upon achievement of pre-agreed sustainability targets.

Sustainable supply chain is one of the current ESG trends, particularly among retailers whose total carbon footprint mainly consists of Scope 3 emissions, which are essentially emissions of suppliers. That is why, more and more companies are trying to encourage procurers to reduce their emissions and, hence, decarbonize the supply chain. Corporate Treasurers can make a substantial contribution to this objective by arranging sustainable supply chain finance programmes. Programmes are based on early-payment principles. As a first step, a company sets up sustainability KPIs to monitor the ESG performance of its suppliers. The performance of suppliers may be measured once or twice per year. After meeting at least one of the established KPIs, a supplier is paid earlier than originally agreed. Hence, highly sustainable procurers will effectively receive better payment terms, which should encourage more suppliers to improve their sustainability performance.

Almost all the above-mentioned ESG products require the establishment of sustainability targets and KPIs. This unfortunately cannot be done by Treasurers on their own but instead should be done at the strategic level by company management. Sustainability targets must be ambitious, meaning that their achievement would require a substantial transformation of business models, e.g. switching to more sustainable suppliers; divestment or restructuring of high-carbon footprint units. Practice shows that not all management teams are capable of setting ambitious targets relevant to the business. Thus, the least Treasurers could do, besides the arrangement of ESG debt or other sustainability-linked products, is to question the adequacy of the chosen sustainability objectives within their organisations. In other words, Treasurers could make sure that the answer to the question “Why did your company set up its net-zero objective?” is not “Because everyone does it” but “Because it is relevant for our core business operations”.

Thank you for reading!

19-10-2022 | Philip Costa Hibberd | treasuryXL | LinkedIn |

We sent our expert Philip Costa Hibberd to the SIBOS conference to discover and explore the World’s Premier Financial Services event.

Last week, the SIBOS conference took place in Amsterdam. Sibos 2022 brought together more than 10,000 participants in Amsterdam and online, as this event returned in-person for the first time in three years.

Philip is delighted to share his experience with you. Happy reading!

The Sibos conference is an annual event organized by Swift that brings together leaders in the payments, banking, and financial technology industries. The conference provides a forum for attendees to discuss the latest trends and developments in the industry, but – as it turns out – it is mostly used as a venue where bankers meet other bankers with the occasional FinTech thrown in the mix.

During the 4 days of the 2022 edition, I learnt that little focus is given to the needs of the corporate treasurer. Throughout the conference, a few interesting recurring themes emerged nonetheless, which I’ll describe in the paragraphs that follow.

Queen Maxima – acting as the “United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development” – kicked off the opening plenary by speaking about the importance of financial inclusion and access to banking services for all.

The first priority is to make sure we do no harm […] but we have a chance today of moving beyond doing no harm to actually doing good. So, beyond transaction volume and customer acquisition can we create the rails for transformative change to help users become more financially healthy?

Sadly the answer I heard from the bankers speaking on stage during the sessions that followed was not promising. “Maximising shareholder value” was still the dominating mantra… which – as experience teaches us – has seldom led the banking industry to “doing no harm”, let alone “doing good” in the past.

A bit more hope for the industry “doing good” came from the voice of FinTechs on stage. As it turns out, a mantra based on “innovation and disruption” makes it easier to attract scarce resources (such as talent) and ironically deliver shareholder value as a consequence.

It was interesting to observe the evolution of the Bank-FinTech relationship. The change in how banks perceive FinTechs today compared to a few years ago was remarkable. Once seen as a threat, FinTechs are today considered an ally by banks.

When asked “Are FinTechs Friend or Foe?”, bankers gave answers as:

“Partnership with FinTechs is our main strategy”.

“Partnership with FinTechs is crucial. They bring agility and they are a matter of survival for us”.

It was hardly a surprise then to learn on day 2 of the conference about BNP Paribas’ acquisition of Kantox, a leading fintech for automation of currency risk management. The relationship between banks and FinTechs will probably only get warmer and tighter from here… but only time will tell if that is good news for us.

Besides FinTechs, another often cited source of innovation for banks was “the regulator”.

Singapore was the most cited example of successful regulator-driven innovation. Its central bank has been encouraging innovation in the financial sector with generous grants to adopt and develop digital solutions, AI technology, cybersecurity capabilities, etc. On top of that, it has developed an exceptionally accommodating regulatory framework. It has for example introduced a “regulatory sandbox” for FinTechs and banks to test their products and services in a live environment without them having to be concerned with compliance hurdles (at least for the delicate initial phases of innovation).

There are hopes that Singapore’s success will be taken as an example by other regulators across the globe, but the most basic expectation from the industry is for regulators to at least set guidelines to improve standardization across the market. As nicely put by Victor Penna, there is still a lot of work to be done:

“Can you imagine if I sent an email from Singapore to Belgium and they couldn’t process it? That is exactly what is happening today with payments. This has to change.”

One last often cited trend where regulators are expected to play a dominant role in innovations, are Central bank digital currencies – CBDC in short.

CBDCs are digital currencies issued by central banks. Typically central banks have two kinds of liabilities:

CBDCs are a third form of liability that complements cash and central bank deposits: they take a digital form and are directly available to the general public.

More than 100 central banks are estimated to be working on their own projects. They are important in the context of innovating the financial sector because they have the potential to provide greater efficiency and transparency in financial transactions. Additionally, CBDCs could help to reduce the cost of financial services and increase access to financial services for underserved populations.

There is still little consensus today on what exactly the impact will be, not least because of the fragmentation of all the initiatives. For example, when it comes to the digital Euro project, the impact on corporate treasury payments is expected to be limited. The project is still in the validation phase, but the assumption is that even if/when the project were to move into the realization phase (decision expected in September 2023) usage will be limited by design with the introduction of low limits to the maximum balances which could be held (exact limits need to be defined, but think of a few thousand euros max).

Banks have invested a lot in the technological backbone needed to support open banking and instant payment requirements across the world and seem to be puzzled by the modest adoption. The ambition is to move away from batches, cut-off times, and end-of-day statements in favour of instant payments 24/7 and provide information-on-demand via APIs.

From a treasury perspective, this brings some challenges. Moving to APIs can be hard, especially if you have a fragmented ERP/TMS/Banking landscape. But the biggest challenge is probably the way that we organize our work and our processes. As jokingly put by Eddy Jacqmotte group treasurer at Borealis:

“Instant Treasury is nice: but I don’t like the idea of instant treasury on Saturday and Sunday”.

The ever-decreasing cost of storage and processing information, combined with the ever-increasing flow and value of user data has transformed the “AI” and “(big) data” brothers from geeky kids in the corner to rockstars in the centre stage.

Besides the obvious use cases such as fraud detection, sanction screening, reconciliation, payment repair, etc. the new trend is to use AI to generate new tailored content and to feed it to users to measure their interest in a specific topic and nudge their behaviour. Instead of asking you directly if you are interested in a mortgage, the algorithm might casually inform you about the price per square meter of properties in the neighbourhood where you go for coffee every weekend. If you interact with the prompt, the algorithm will take notice and will keep on feeding you with “property-related” information, until you find yourself asking for a mortgage…or showing interest in something else that the bank can do for you.

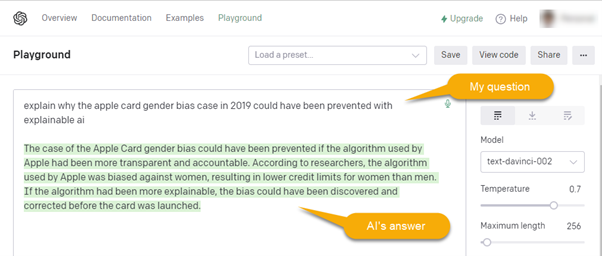

Sounds sketchy? It might be, that’s why another trend in this area has been making its way to the foreground: Explainable AI.

Explainable AI is a form of AI that can provide understandable explanations for its predictions and decisions. This is important especially in the financial industry because it can help to build trust with customers and regulators and avoid (or at least make explicit and controllable) unwelcome biases.

For example, the Apple Card / Goldman Sachs scandal in 2019 could have been prevented if the algorithm used by Apple had been more transparent and accountable. According to researchers, the algorithm used by Apple was biased against women, resulting in lower credit limits for women than men. If the algorithm had been more explainable, the bias could have been discovered and corrected before the card was launched.

In essence: AI is powerful, but transparency is key. On that note, I have a confession to make: the previous paragraph was written by an AI and not by me…

Thanks for reading!

29-03-2022 | Philip Costa Hibberd | treasuryXL | LinkedIn |

What are 3 key do’s and don’ts to keep in mind in your RPA journey? Find out in this article I wrote, which was originally published in the Summer Edition of the Zanders Magazine.

This article was originally published in the Summer Edition of the Zanders Magazine. Are you interested in knowing more about Process Automation in the realms of Finance, Treasury and Risk Management? Feel free to reach out to me on LinkedIn.

Last year’s spring, we organized a ‘jargon-free’ breakfast session to explore what robotic process automation (RPA) is all about. We had a look under the hood of a complex, hard-working robot and shared experiences on how to make the journey of deploying a digital workforce as smooth as possible. Find a brief summary below, covering (briefly) what RPA is about, what are the 3 main stages of the RPA journey, and what are the key do’s and don’ts per each stage.

RPA stands for Robotic Process Automation and is software that performs rule-based work, interacting with systems, websites and applications in the same way a human would. It is a powerful tool that, when applied to the complex industries we work in, allows us to focus more on the valuable activities that make our jobs interesting and less on the boring and repetitive tasks that no one wants to do. You can think of it as macros on steroids.

You can find the key takeaways from the Breakfast Session, in the form of do’s and don’ts, summarized below for each of the following 3 stages of the RPA journey:

✔Do: Have fun!

Did you enjoy playing with Lego when you were a child? Then you will probably enjoy tinkering with RPA. Just like with Lego, spend some time discovering all the different components that you have available and finding out all the different ways you can get them together to craft something useful and tailor-made to your needs. Did you like playing with Barbies better than Lego? That’s also great, don’t worry. Deploying RPA in your team will give you plenty of opportunities to put your role-playing experience to use. Understanding roles, responsibilities, objectives and requirements of a process and effectively communicating the benefit of automating via RPA are the pillars of a successful implementation.

❌ Don’t: Don’t forget to explore slightly more advanced components, such as queues, credential management tools, log management tools, robot orchestration and control rooms.

You don’t want to have to bulldoze and rebuild your shiny proof-of-concept automation in a later stage, just because you weren’t aware of these components. They will become critical once you have more than a few processes at hand.

To stay in the Lego metaphor: make sure to explore the features of the full Lego range and don’t just idle on the baby-friendly Lego Duplo.

✔Do: Make sure processes and solutions are well documented.

I get it. You want to start building your bot as soon as possible. But make sure to first invest some time in drafting the following documents:

• A Process Design Document to capture at the very least the As-is process flow

• A Solution Design Document to capture how you intend to automate the process

You will be happy to have the former if (when?) you start having discussions on the scope of the work that the bot is expected to perform. It can prevent misunderstanding about what the process is all about and what the bot can do. You will be happy to have the latter if (when?) you have to do some maintenance on the bot that you are now developing. This blueprint will help you to quickly zoom in on the component that you need to tweak.

Good documentation will become even more important as your team grows. Imagine how much karma you will earn when someone in urgent need of fixing the bot finds and reads your clear blueprint!

❌ Don’t: Don’t automate sub-optimal processes.

Get everyone familiar with the concept of GIGO – Garbage In Garbage Out – and its less polite brother SISO. A bad manual process will become a terrible automated process, because robots can only act based on predefined rules. The rules can be as complex as you like but there can’t be any room for discretionary judgment. The untiring robots lack that.

Make it clear that a process needs to be streamlined and standardized before it can be a candidate for automation. If it’s not, someone will have to cross the jungle of “It has always been done this way”, which usually stands between a ‘Garbage Process’ and a ‘Good Process’. Who knows, it might turn out that many tasks and subtasks in the process weren’t needed after all.

✔Do: Set up a clear RPA Governance.

Once you hit the stage of growth, where your team is rolling out one bot after another, clearly defining the process of automating processes becomes even more important than clearly defining the process that you are automating.

Does the RPA team sit in IT or with the business? Who is responsible for what, in case of a malfunction? How are Audit, Compliance and Risk Management going to adjust policies to include the changes brought in by your new digital workforce?

❌ Don’t: Don’t forget Security.

While designing your RPA Governance framework, don’t forget the more practical side of Security.

You wouldn’t want to allow anyone the temptation of circumventing the four-eyes principle you already have in place. For example, you must make sure it is still impossible for anyone to input a payment to themselves and have it released by the unaware robot accomplice.

Define as soon as possible how you are going to create, assign and manage the credentials that your bots will need to interact with your existing IT infrastructure. Particularly in the case of unattended bots, it would be best to create specific users for your digital colleagues, with clearly distinguishable usernames. You might even consider going as far as letting your robot change all its passwords to ones of its secret liking as soon as it gets in production.

30-08-2021 | Maximo Santos Miranda | treasuryXL

Máximo holds a PhD in Economics and is graduated in Law. After 18 years working in International Cash Management in several multinationals coordinating local treasury units with the headquarters or implementing new ones all around the world, he is working as a university professor of finance, treasury and business strategies in several Universities and Business Schools in Spain. He is also a regular contributor in international media such as Forbes México, Forbes Centro America or Revista Gestión of Ecuador for the last five years.

“My first job in treasury was the best you can wish for”

As a researcher he has published more than 30 articles in research journals about banking systems, treasury, finance in general, fintechs or international sanctions and at the same time he is a referee in postgraduate research journals. He also collaborates with Think Tanks and international institutions in different ways.

After finishing my studies in economics, my intention was to work for a bank. In fact, my first professional steps were in banking. However, one day I saw a job offer that looked very interesting and I applied for it. Normally, I always prepare the job interviews in detail but this didn’t happen at that time. So, I went to the interview with no visibility of the company I was applying for. After a couple of quick interviews, I was selected as a treasury analyst for Cemex European headquarters.

Everything was perfect. My first job in treasury was the best you can wish for. I was part of the team of international cash management and Cemex at that time was in the middle of fast growth movements. Cemex acquired different subsidiaries worldwide and I was in the center of all those financial flows. There was much stress but the work atmosphere was fantastic and the promotion possibilities were reachable.

Most of my career in treasury has been focused on the international side and that provides an unpayable extra value. Thanks to being an international treasurer I have learned a lot about how treasury and finance work worldwide. I have had the opportunity to see how the banks work in many countries and how different companies from different sectors and industries adapt their cash management to their operative peculiarities and the markets where they are inserted.

International cash management is my greatest strength in the treasury world. Most of the time in my treasury career I have worked as a coordinator of local treasury units. That role has allowed me to see different approaches to similar issues in different countries.

In my first years in treasury, I had to coordinate the movement of funds (in three currencies) between different subsidiaries located in different countries and different banks on the same day. The number of funds moved was very high and the number of countries where the money passed through was also high (more than 20 countries in three continents). I was preparing the operation for a week and finally everything went fine. For me it was quite stressful as the operation was completed finally in 15 hours and it was necessary to compensate several delays in the intermediate transactions. When you prepare in detail a complex operation like that and everything is completed as forecasted you feel very proud of all the work done. After that operation, I have coordinated other operations quite similar but the level of stress has been much lower compared with the first one.

In the year 2005 Cemex sent me to Italy for three years to set up a new treasury unit in the country. For me it was a big challenge. First of all, because I didn’t speak Italian when I went there and soon I realized that to speak Italian is a key point if you want to do your job properly. Secondly because although I worked for a big multinational, the Italian subsidiary was quite small and the approach of the local banks was completely different to that I saw in the Cemex European headquarters in Madrid.

Things work if you prepare them in detail. You can have a very complex operation in your hands but if this operation is prepared in detail (forecasting different scenarios and alternative solutions) the final success is almost guaranteed. Good preparation is the key to success.

The function has changed a lot. When I started in treasury in the year 2001 the administrative workload was the most relevant part of the treasury function, at least in time-consuming. Today instead and thanks to technology the time spent on administrative issues have been reduced significantly. That reduction has allowed the treasurer to dedicate more time to other issues that generate more value for the company. A good treasurer today must know much more than before about technology applicable to the treasury function and must also have strategic thinking.

The treasury teams will be smaller in the future. The technology will reduce all the administrative treasury tasks to the minimum. The treasurer of the future should be focused on technology, strategic thinking and create additional value for the company. To reach that goal, the corporate treasurer should be passionate about the function and must be always informed of the latest developments in the market. The corporate treasurer should know the latest developments in technology, in treasury products, in treasury strategies… always learning. The treasurers of the future should communicate better and invest time in treasury education and build treasury networks to exchange knowledge with other colleges or experienced treasurers. To sum up, the treasurers of the future should increase their impact in the companies thanks to the technology developments.

19-04-2021 | Philip Costa Hibberd | treasuryXL

With over 12 years of experience in the financial industry with the last four years in treasury consulting, Philip has recently launched his own consulting activity, Automation Boutique, specialized in (robotic) process automation for Treasury, Risk and Finance.

“I have been coding for fun since I was a kid. This skill has been very useful throughout my career but has become my trademark in Treasury.”

He recently developed the tool that was awarded the “2020 Best Fintech Solution – Adam Smith award” by Treasury Today magazine. He now tries to focus on what he has always enjoyed the most during his career: solving problems at the intersection between ‘numbers’, ‘people’ and ‘technology’.

As for many of us, it started somewhat by accident. After working in other areas of finance for many years, a few ethical questions started nagging me. Add a sabbatical, some romance, and a few lucky phone calls and I found myself joining the great corporate treasury team at Zanders (a consultancy firm specialized in Treasury, Risk and Finance).

I love the diversity of challenges. You are dealing with the financial heart of the company and need to make sure that the right amount of blood reaches every cell. This necessarily means dealing with different kinds of issues, topics and people. This keeps Treasury fun and in constant evolution!

I have been working as a consultant on very different Treasury projects, from interim roles to system implementations. I guess I am what you would call a generalist, but with a knack for using technology and social skills to solve problems. I have been coding for fun since I was a kid. This skill has been very useful throughout my career but has become my trademark in Treasury.

Going back to the cardiovascular metaphor for Treasury, the best experience was probably when I was called by a client to solve an urgent clot which was at risk of causing severe damage. An apparently simple data migration exercise turned out to be much more complex than anticipated and was at risk of causing severe delays to a multimillion project. The solution involved a robot, a laptop being flown up and down Europe, a wedding and unreliable hotel wi-fi. Surprisingly, instead of being the ingredients for a bad joke, this led to a happy client and to an award-winning solution.

My biggest challenge in Treasury was witnessing the clash of American, Dutch, Indian, Japanese and many more cultures during a global SAP implementation (going live during a pandemic). Holding three nationalities and being exposed to different cultures from an early age didn’t help me as much as I would have hoped. I would encourage anyone working with different cultures to read Erin Meyer’s book “The Culture Map”. It will be helpful.

No one is rational and analytical all the time, not even experienced treasury professionals. Good communication is more important than perfect data and models, especially during a crisis. Without it you will lead or be led by emotion and will certainly miss the best course of action. When fear creeps in your own monkey mind, don’t be afraid to have a good conversation with it. Assess how big the actual threat is compared to the shadow being cast by your amygdala.

Corporate Treasury has come a long way from its more transactional origins and – as expected – is taking more of an advisory and strategic role within organizations. The boundaries with other specialized professions have faded (risk management and FP&A just to name a few) and I think that this is a good thing. Skilled professionals should be employed to solve interesting problems and come up with great ideas. The best problems and ideas are usually found at the intersection between disciplines and it’s only natural that we tend to all meet there more and more often.

For the near future I expect the focus on the hot topics of the moment to continue: cash visibility, cash flow forecasting, operational efficiency etc.

For the further future, I won’t adventure on guessing exactly what hot topics the next crisis will bring. I will instead share my best guess on the evolution on the corporate treasurer as a person.

My guess is that she or he will be less of a specialist and more of a generalist. The ideal corporate treasurer will be ‘renaissance polymath’ if you will. Our rapidly changing environment makes it more difficult to remain a (useful) specialist for long. Technology also tends to favour the generalist by democratizing specialist’s skills. There will certainly always be room for very specialized knowledge, but the risk of learning too much about too little in a dynamic environment, is that after a while you risk knowing everything about nothing.

28-07-2020 | Arnaud Béasse | treasuryXL

Welcome to the 10th and last (for now) interview of the ‘Meet the Expert’ series. This time we interviewed our brand new Expert Arnaud Béasse. Arnaud is founder of the advisory firm Arts+Brands and an expert in Debt Management. He started his career as Regional Financial Controller, cumulating the responsibility for IT.

Arnaud has more than 17 years experience in Banks focusing successively on Structured Asset Finance, Corporate Banking, DCM and in Multinational Corporates for their Energy and Metals trading and Project Finance. He created Arts+Brands to expand his entrepreneurial spirit by advising small ventures and start-ups (Fintech, Biotech, IT) for their Fund Raising and Finance strategy and also by getting involved in the daily operations.

Arnaud is fluent in English, German and French and is used to work in international, multi-cultural and virtual teams environments.

During my first assignment as a regional financial controller, I have been immediately confronted to a complex consolidation of cash streams from different emerging countries with different currencies and regulations. Finding secure and systematic solutions has been challenging but also interesting and fun. This was the beginning of my treasury discovery, from which I moved then to asset finance, project finance, trade and export finance and later to the complete « corporates and markets » solutions offered by a large European bank.

I find the central role played by treasury in supporting a business very motivating: it manages all financial resources a business needs to generate returns. Perfect understanding and anticipation of the needs (planning) and an accurate analysis of the resources available (controlling) are therefore essential. I also like the necessity of combining short term priorities like cash management and long term planning like investments.

Capitalising on my long banking and large corporates experience, I have acquired a strong knowledge of all kind of debt solutions associated with credit, regulatory, compliance competencies. I have specialised in Debt Management, Fund Raising, Asset Finance, Leasing, Cash Flow Management, Trade and Export Finance and Project Finance. I am currently focusing on Sustainable Finance to support firms aligning their finance resources with their commitments towards the environment.

The starting point of debt management is a careful analysis and control of the cash flows. Borrowings need to align with the business cycle of the company and eventually its equity profile. Once the needs of each business line and the corresponding cash flow generation are consolidated, the adequate debt structure can be designed with a mix of junior to senior, short term to long term solutions and a calibrated interest rates structure.

I remember a dramatic situation occurring during a local currency crisis in an emerging country, where we had arranged a large equipment finance. The debt repayment plan did not anymore match with the borrower’s cash flow generation and we were heading straight to a default situation. After long and numerous discussions, we managed to get transferred a large position on natural resources the company was owning but not operating and structured it in a way that the majority of risks were covered, the credit committees and respective boards were satisfied and ultimately the borrower managed to earn additional profit. I admit there is a part of luck in this experience but getting from this desperate situation to a point where all parties were so happy has been my most fulfilling experience so far!

I consider the toughest challenges in a company are almost always linked to human resources management and termination of assignments. But if we remain within the treasury topic, my biggest challenge so far has been to accept a board decision not to conclude an M&A transaction, whereby all indicators (profit, risk, market position, further opportunities) were very favourable for the group and I had worked for more than one year on the case. Some months later, upon publication of the yearly results, it became clear why the project was rejected!

Along the various experiences I had with treasury, the most important lesson might be to always seek the most simple and straight forward option. There are many ways of hedging a currency position, improving the average interest rate of a pool of debt facilities, leverage the value of an asset, optimise the return of positive cash position. But the risk and time associated to it can rapidly be disproportionate to the purpose and the size of the original transaction. Treasury shall normally create value, not necessarily profit!

Obviously, the role of Corporate Treasurer has become more and more complex. Treasury needs to deal with an increasing availability of alternative financial products, intensifying risk management requirements, regulatory and compliance constraints. But at the same time, the emergence of digital treasury platforms and integrated cash management systems are making the steering of treasury much easier and more accurate.

Treasury is between a rock and a hard place: as a consequence of the crisis, sales are dropping and cash flows are missing but the financial obligations (debt, salaries, rents, supply, …) remain and the access (if not the availability) of financial resources become difficult. For treasurers who had a prudent cash flow management with enough resources to bridge the gap, it has been a confirmation for their risk management strategy. For others with more lean structure, it is, in the best case, a very stressing moment trying to find last minute and costly (not only in terms of interest rates) funding solutions. Some businesses, which have bet on a very tight business model, will probably be restructured. The crisis will certainly lead corporates to adopt more careful models with sufficient reserves and flexible organisations but also postponed or reduced investments.

The main trend is definitively the further digitisation of the treasury functions, offering more reliable, more secure and faster execution of the transactions: payments, cash management, trading, trade and export instruments, guarantees, etc. As the execution of transactions will be more and more automated and integrated in the supply chain systems, treasurers will shift their focus on analysing and planning for the financial resources in order to formulate strategies.

Another interesting trend for the treasurer is the further development of the non-banking debt market. This shall broaden the borrowers’ horizon, balancing again the bargaining power in favour of the corporates and generating even more tailor-made/OTC debt solutions.

Running a business without a treasurer can only be considered for small businesses. For standard operations, managing the daily needs with modern digital tools will always become easier, even if substantial support shall be required during the implementation of a system. Once the system is running, the daily treasury tasks can be integrated in the accounting and finance agenda.

However, as soon as operations get more complex (investment, take-over, international development, restructuring…), the support of a specialist remains essential, be it for a limited period of time like part-time or ad interim…