Instant Payments: the SEPA Instant Payments rulebook is published, what’s next?

| 20-2-2017 | Boudewijn Schenkels | Sponsored content |

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.

SEPA Instants Payments (also called SCT Inst – SEPA Credit Transfer Instant) will allow sending and receiving money 24/7 in seconds. European banking communities can go live from November 2017, the Dutch community has planned to go live from May 2019 with the first Instant Payments services. The development of the SEPA Instant Payments infrastructures of the banks and processors are in train. In april 2018 the start of the inter-CSM testing is planned, the end-to-end bank tests and the pilot phase from January until April 2019.

From our Instant Payments training classes for business professionals and IT staff, we find that participants are not fully aware of the large impact Instant Payments will have on the complete value chain and the opportunities it will bring. In order for you to understand the impact and opportunities, I will explain how Instant Payments are processed.

To give an impression of all the change aspects for users, the banks and the interbank processing side:

For corporates amongst others:

- Different and new initiation processes, including, if applicable, instant insight in the failure of the payment;

- New cash management and/or ERP applications or upgrades;

- Reconciliation aspects;

- Requirements for instant insight of bank account mutations;

- Changed processes to monitor late payments (as they can be delivered eg. in the weekend);

- Evaluate the potential of new services based on Instant Payments;

- 24/7 operation required?

- Possibilities in product differentiation.

For banks amongst others:

- Support new payments processes;

- Real time and 24/7 reporting;

- Extra notifications and reach filtering (as SEPA Instant Payments is not mandatory);

- Revised (24/7) operational processes;

- Changes to fraud/AML/sanctions management;

- New sales and product management activities and roles;

- Changes liquidity management processes and monitoring;

- New clearing channel(s).

For processors amongst others:

- New clearing and settlement processes;

- Revised operational processing and monitoring;

- New sales and product management activities and roles

As the launch dates come nearer it certainly triggers managers to now thoroughly evaluate scope and time scales for (required) internal projects and ensure to be ready and steady before launch in 2019 as well as business professionals to anticipate and grasp the potential opportunities.

The key differences between the current SEPA Credit Transfer and the new SCT Inst scheme are:

- 24/7 available (no downtime)

- real-time (5 seconds in Netherlands round trip)

- real-time failure notifications

- single transaction only

Instant Payments process

In our training, we also explain the differences between the normal payment flow (SCT) and the Instant Payments flow (SCT Inst). The process flow is described below in summary and will take place in several seconds.

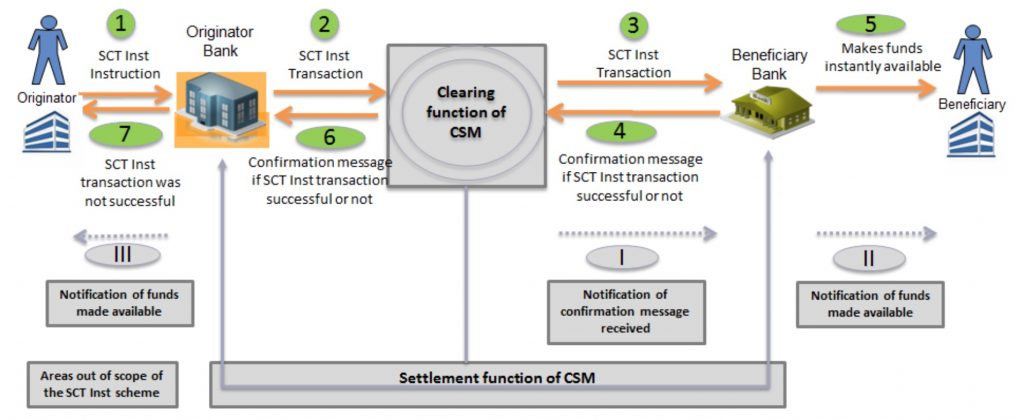

Figure 1. (Source: EPC Rulebook)

Several key actors are involved in the payments process:

- Originator: party sending the payment (payer, customer of the bank)

- Originator bank: the bank of the payer

- CSM: interbank party that clears and settles the payments between banks (Clearing and Settlement Mechanism)

- Beneficiary bank: the bank of the payee

- Beneficiary: the party receiving the payment (payee, customer of the bank)

The new process in summary:

The Originator Bank receives an SCT Inst Instruction from the Originator (Step 1). It verifies the instruction and sends the transaction to the CSM (Step 2), which verifies the message, ensures that the Originator bank has enough funds and instantly sends the SCT Inst Transaction message to the Beneficiary Bank. The Beneficiary Bank instantly verifies the payments and if it can be booked on the account of the Beneficiary (Step 3). The Beneficiary Bank confirms to the CSM if it was successful (positive confirmation) or not (negative confirmation with an immediate Reject) (Step 4). The Beneficiary can withdraw the funds (Step 5) instantly if in the previous step the confirmation was positive (and after the Beneficiary Bank has ensured that the CSM received the positive confirmation message). The CSM instantly reports to the Originator Bank if the SCT Inst Transaction had been successful (or not) (Step 6). In case the Originator Bank receives a negative confirmation about the SCT Inst transaction which indicates that the funds had not been made available to the beneficiary, the originator bank is obliged to immediately inform the originator (Step 7) and lift the reservation of the amount made in step 1.

All in seconds and 24/7!

This all means, that beside the flow of money, there is also a flow of messages between the customer and the bank. Both Beneficiary and Originator will be informed (in a few seconds) that the transaction is done (or not).

Are you interested in what the new SEPA Instant Payment will mean for your organization?

Come to our next open training (March 15 in Utrecht) or inquire about the possibilities of an in-house training.

More information at: www.paymentsadvisorygroup.com.

If you have any questions please contact us via: [email protected] .

Senior Consultant Payments @ Payments Advisory Group