Currency markets impacted by a number of factors as we open a new decade

| 9-1-2020 | treasuryXL | XE |

The markets have been exposed to some real turmoil. In the wake of the tensions in the Middle East, we have seen a general decline of stocks and move toward typical risk on plays – treasuries are up overall, gold is trending higher and so is oil. Very generally there are a number of themes affecting the major crosses.

Let’s get up to speed and examine these broadly:

GBP:

On one hand, there have been an increase of investment monetary inflows based on economic data. Add to this a general sentiment of rate hikes from the Bank of England still being on the table and a very likely sense of uncertainty or even fear from European exporters with the ECB under a great deal of pressure to stabilise/raise inflation (and be inventive in doing so) and Italy dragging the boat down somewhat there is every opportunity for the trade items to play out in a buoyed GBP. There are a few ‘watch out’ aspects, though. These may include things like monetary policy having been kept on hold due to Brexit (and there could be a case to see the Conservatives attempt to waylay Bank of England’s efforts to raise rates) and the possibility that investors have priced a recession into investment outlook. When reviewing 17 institutional banks’ forecasts for 2020, the consensus is for a rate to the Dollar of 1.3400.

USD:

Again, a tale with two sides to the coin. The Federal Reserve has added liquidity to the repurchase market (short version of this mini-crisis is: that the amount of available cash in this market dropped exactly as the demand for borrowing jumped which made interest rates look outlandish – the added liquidity settles this and resumes a better velocity of money, or speed of funds flowing through the economy). There are still some divisions remaining in terms of the Fed’s outlook for rates, meaning that stabilising and stopping rate cuts isn’t technically off the table. The uncertainty in the Middle East in the clash between the States and Iran means that investors have flocked to the safe-haven currency of the Dollar and add to this some very real concerns about the strength of the global economy and growth forecasts, meaning that safe haven movement could have longer to garner flight to the Dollar all could point to a near to medium term robust USD. Temper this view with some very conflicting US economic data, muted inflation price pressures and China getting rid of bonds – which would force the States to increase its balance sheet.

EUR:

The EUR has had a short-term increase in currency strength versus the GBP, but this is largely from uncertainties of how trade will be arranged in finalising Brexit. There are widespread concerns that, if a deal may not be organised in the timeframe allotted, the UK could default to trading with the EU on World Trade Organisation terms, which are far less favourable than a direct agreement. As earlier mentioned, though, the EU has significant issues brewing in the form of inflation control via the ECB and from a very poor economic performance by Italy in the last 8-12 months in particular. There are green shoots of good news, though, with preliminary German consumer inflation figures looking far better than expected – a significant contribution to solving their issues given Germany’s size and relative impact on the bloc. All things said and done, against the context of uncertainty from geo-political risks and fiscal/trade uncertainties as well, the EUR could well be the net loser in the coming weeks.

Elsewhere in the world, the cost of the bush fires in Australia are touted at being ~$2bn AUD and climbing, but of course, the cost of people’s lives and the lives and environment for their unique and rich wildlife ecosystem will be immeasurable. Our hearts go out to the people of Australia and the brave service people fighting the disaster.

GBPEUR: 1.1800

GBPUSD: 1.3198

EURUSD: 1.1183

The figures are based on the live mid-market rate, correct as of 08:30 GMT on 07/01/2020, and are provided for indicative purposes only. Live mid-market rates are not available to consumers and are for informational purposes only. The rates we quote for money transfer can be selected via the page on our website ‘Live Money Transfer rates’.

Get in touch with XE.com

About XE.com

XE can help safeguard your profit margins and improve cashflow through quantifying the FX risk you face and implementing unique strategies to mitigate it. XE Business Solutions provides a comprehensive range of currency services and products to help businesses access competitive rates with greater control.

Deciding when to make an international payment and at what rate can be critical. XE Business Solutions work with businesses to protect bottom-line from exchange rate fluctuations, while the currency experts and risk management specialists act as eyes and ears in the market to protect your profits from the world’s volatile currency markets.

Your company money is safe with XE, their NASDAQ listed parent company, Euronet Worldwide Inc., has a multibillion-dollar market capitalization, and an investment grade credit rating. With offices in the UK, Canada, Europe, APAC and North America they have a truly global coverage.

Are you curious to know more about XE?

Maurits Houthoff, senior business development manager at XE.com, is always in for a cup of coffee, mail or call to provide you detailed information.

![]()

Visit XE.com

Visit XE partner page

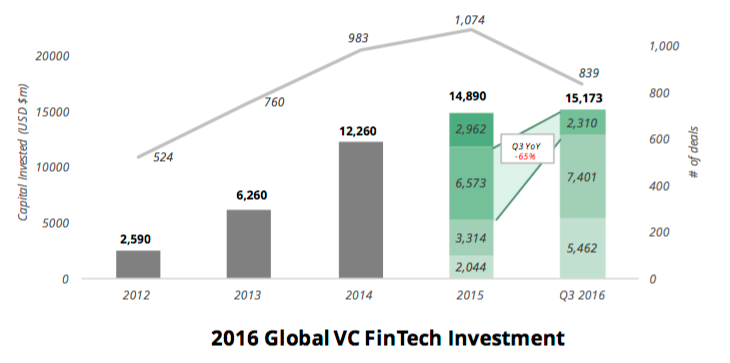

With the steady rise of Fintech within the finance industry some people are already calling for the demise of banks as the historical financial partner of choice for corporates. Certainly, Fintech is showing itself to be very dynamic, offering many new products and solutions, and being a lot swifter than the banks. Banks seem to have grown too big and complacent, are being weighed down by new rules and regulations, are less prominent in the field of funding for corporates, and possibly have lost their focus on what used to be core businesses. But let us examine the relationship between bank and client.

With the steady rise of Fintech within the finance industry some people are already calling for the demise of banks as the historical financial partner of choice for corporates. Certainly, Fintech is showing itself to be very dynamic, offering many new products and solutions, and being a lot swifter than the banks. Banks seem to have grown too big and complacent, are being weighed down by new rules and regulations, are less prominent in the field of funding for corporates, and possibly have lost their focus on what used to be core businesses. But let us examine the relationship between bank and client.

FinTech is a term that is becoming popular in the financial world. Only one third of the financial experts know what this means and understands what consequences it has for their business. How this innovation is currently changing the ecosystem of money, is still relatively unknown.

FinTech is a term that is becoming popular in the financial world. Only one third of the financial experts know what this means and understands what consequences it has for their business. How this innovation is currently changing the ecosystem of money, is still relatively unknown.