Commercial Paper – alternative short term funding

| 03-05-2018 | treasuryXL |

Instead of just relying on banks to provide short term funding, large corporations are also able to access the European Commercial Paper market (ECP). This is an alternative market that can assist in meeting short term funding requirements. This provides a good alternative to products previously mentioned – such as lines of credit. In this article we shall look at what ECP is, how it can be issued and what the market for this paper is.

Definition

Commercial Paper is a promissory note that is unsecured with a maturity shorter than 1 year. A corporation will, initially establish a CP programme which determines the terms and conditions – such as maximum allowable issuance amount, termination date of the programme or open ended, currencies, bank dealers etc. The issue is subject to a credit rating and the paper is rated. It is also possible to issue your own paper instead of through a dealer, though this is not used as much.

Issuance

The issuer has 2 approaches: issuing paper as and when funding is needed, or being informed by the dealer that there is demand from the market for additional paper. As the paper is negotiable, clearance and settlement is provided via one of the major clearing houses – Euroclear, DTC etc. Settlement is the same as a spot transaction – taking place two working days after transacting. As ECP is in competition with other forms of short term investment, it is necessary to have an active presence in the market – lenders need to know that there is demand for their funds and issuers are in direct competition with other issuers.

Use

ECP allows issuers to fund themselves in a more flexible manner than traditional bank lending – this can be seen in both the issuance amount and the tenor of the paper. Issuers with the highest credit ratings can often achieve funding below the cost of Euribor/Libor. This allows issuers to fund a significant portion of their total funding requirements on a short term basis. As short term rates are normally lower than long term rates, this leads to a reduction in the average cost of funding. An ECP programme for as little as EUR 250 million can be established, though it is more common to see programmes for more than EUR 1 billion.

Motivation

An issuer needs to ascertain that there is a definite funding requirement and that an ECP programme can successfully be utilised. There are ongoing costs involved, so it is not just a question of setting up a programme and then leaving it there in place without using it.

An issuer needs to know if there is a true appetite in the market for their paper. No issuer wants to find that having established a programme that there is no demand for their paper.

How does the short term funding fit into the funding requirements of the issuer on the whole? Not only do they get access to cheap funds, they also gain access to potential borrowers who could be interested in supplying alternative long dated funding.

Conclusion

ECP offers a lower cost of funding, flexibility in both issuance timing and maturity, and is unsecured. As the paper is tradable, investors can always sell their paper on in the secondary market. This must be weighed up against factors such as cost of programme maintenance, reduction in lines of credit, and the fact that only top rated issuers are accepted.

For large corporations an ECP programme is attractive, but needs constant maintenance and attention. It offers an attractive bespoke alternative to traditional bank funding.

If you have any questions, please feel free to contact us.

Met het huidige nieuws rond beursgangen (IPOs = initial public offering) heb ik gezocht op het steekwoord beursgang op treasuryXL en vond geen resultaten. Wellicht omdat de treasury beroepsgroep communiceert in het Engels. Voor Non-Treasurers ga ik bij deze kort in op de basisbeginselen van een beursgang en waarom hier zoveel aandacht voor bestaat.

Met het huidige nieuws rond beursgangen (IPOs = initial public offering) heb ik gezocht op het steekwoord beursgang op treasuryXL en vond geen resultaten. Wellicht omdat de treasury beroepsgroep communiceert in het Engels. Voor Non-Treasurers ga ik bij deze kort in op de basisbeginselen van een beursgang en waarom hier zoveel aandacht voor bestaat.

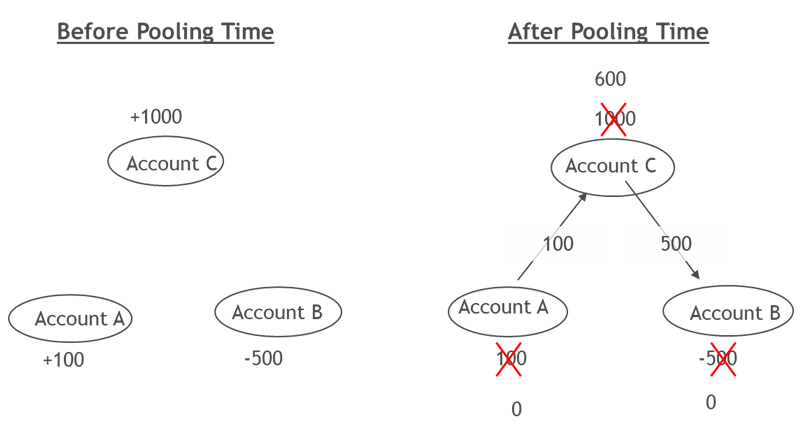

There are also other forms of cash concentration:

There are also other forms of cash concentration: