Blockchain: Playing in the sandbox

| 13-09-2016 | Carlo de Meijer |

A new – but important – chapter can be added to the blockchain story. The World Federation of Exchanges , the WFE, recently urgently called for the creation of regulatory sandboxes for distributed ledger technology. This should help industry efforts “to explore and understand the impact of blockchain-based services in the capital markets”. The Federation added that regulatory bodies should collaborate with the industry on new developments to minimise unintended consequences.

A new – but important – chapter can be added to the blockchain story. The World Federation of Exchanges , the WFE, recently urgently called for the creation of regulatory sandboxes for distributed ledger technology. This should help industry efforts “to explore and understand the impact of blockchain-based services in the capital markets”. The Federation added that regulatory bodies should collaborate with the industry on new developments to minimise unintended consequences.

Regulators enter the stage

This is a very important signal to the regulators that they should take this technology serious and needed to enter the blockchain stage in order the give regulatory clarity. Innovations like blockchain should be primaly industry driven, and “not be unnecessarily impeded by regulatory intervention”, said the WFE. (see also my Blog: “Blockchain and regulation: do not stifle ….”, published 4 April).

Collaboration with the industry will allow regulators to understand the technology, how the future infrastructure will look like and what the impact will be on the financial markets. But above all how they could most effectively perform their regulatory tasks. With the insight and knowledge obtained, regulators will be better placed on the changes necessary to evolve the regulatory environment to not only better regulate these businesses, but also continue to ensure that the legislation does not frustrate this innovation.

Regulatory sandboxes

Regulatory sandboxes have proven to be a useful tool for the wider fintech industry in various jurisdictions. “Promising innovations may be stifled and opportunities missed as firms may be unclear on whether a new product or service complies with legal and regulatory requirements, and consequently may choose not to pursue their new product or service further”.

That is where the ‘regulatory sandbox’ comes in. They have been formed to provide a safe environment for businesses to test their innovative products. These sandbox allow firms to experiment with fintech while providing the appropriate safeguards to contain the consequences of failure for the customers.

New entrants to the financial services market, can use the sandbox to test products, services, business models and delivery without first needing to meet all of the normal regulatory requirements and incurring the considerable costs of putting in place the complex structures and processes to successfully apply for regulatory authorisation.

This should allow appropriate collaboration and exchange of information between industry and regulators.

Regulatory sandboxes: an overview

Since this year these regulatory sandboxes have been extended to distributed ledger technology in a number of countries including UK, Hong Kong, Singapore, Australia and Abu Dhabi. And now also other regulators are thinking about introducing such a testing environment.

- Regulatory Sandbox Open for Play in the UK

The UK regulator FCA launched a regulatory sandbox early May this year. This is a next step for the FCA, the Financial Conduct Authority as part of Project Innovate, which aims to boost competition and growth in financial services. Goal is to help banks and other financial service providers reduce the time it takes to bring innovative ideas to the market.

The FCA’s sandbox will allow business to test disruptive technologies including distributed ledgers in a live environment “without immediately incurring all of the normal regulatory consequences”. The FCA however said that consumer protection will be a significant focus, and will be considering appropriate consumer safeguards.

Application

Fin-techs could apply to the UK’s regulatory sandbox from 9 May till 8 July. The second ‘cohort’ will have an application deadline of mid-January 2017.this year

The FCA uses an inclusive approach to defining potential users. That means anyone from a start-up to a multinational can benefit from the sandbox. For authorised users and suppliers, the FCA has identified three key tools to businesses on a case-by-case basis (individual guidance; waivers; and, no enforcement letters). Unauthorised business will use the sandbox predominantly to facilitate testing without the need for full authorisation from the FCA.

Accessing the FCA sandbox is however not straightforward. A firm must meet a number of key eligibility criteria including: be in an in-scope business; demonstrate a genuine innovation; deliver a consumer benefit; demonstrate a need for the sandbox; and, be ready for testing. It should also be noted that the sandbox will not be available for activities which fall outside of the Financial Services and Markets Act 2000. For example, payment service providers and e-money issuers already potentially benefit from the lighter touch regimes in the PSRs and the Electronic Money Regulations.

- Hong Kong Monetary Authority (HKMA) plans to create a regulatory sandbox

HKMA last week announced plans to create a regulatory sandbox, where start-ups and banks can test solutions and express their ideas before applying for authorisation. The sandbox allows banks to conduct tastings and trials of newly developed technology such as blockchain on a pilot basis. Within the sandbox, banks can try out their new fintech products without the need to achieve full compliance with the HKMA’s usual supervisory requirements.

In a related initiative, the HKMA has set up a ‘fintech facilitation office’ with its own dedicated e-mail account to act as a platform for the exchange of ideas between the regulatory body and banks and tech firms. Industry players, such as banks, payment service providers, fintech start-ups, the HKMA, etc. can get together at this facility to brainstorm innovative ideas, try out and evaluate new fintech solutions, conduct proof-of-concept trials, and gain an early understanding of the general applicability of creative solutions for banking and payment services.

- ASIC released consultation paper on regulatory sandbox

Also Australia plans a regulatory sandbox for fin-techs technology innovations including blockchain. The Australian Securities and Investments Commission (ASIC) released a consultation paper on this issue, detailing proposals for a testing ground for innovative robo-advice providers and other similar services. It also highlighted ASIC’s views about some regulatory options already open to fin-techs under the current law.

The sandbox will allow new entrants to test a service for up to 100 retail clients for up to 6 months without holding an AFSL. The service can only relate to advice and “arranging” for dealing, catering primarily to robo-advisers. Product issuers such as payment facility providers and marketplace lenders are excluded, as is advice about general and life insurance. Start-ups will not need to apply to ASIC to be admitted to the sandbox (unlike comparable sandbox arrangements in other jurisdictions), but may need to be vetted by a “sponsor”, such as a hub, co-working space or venture capital firm.

A final regulatory position is expected by December.

- MAS proposes regulatory sandbox for fintech

Early June, the Monetary Authority of Singapore (MAS) released a consultation paper detailing guidelines for a ‘regulatory sandbox’. With this sandbox approach the MAS hopes to encourage and help firms experiment with innovative solutions to support their development, and bring fintech solutions to the mainstream.

Any interested firm can adopt a sandbox to experiment within a well-defined space and duration; the MAS will provide the appropriate regulatory support and will relax certain legal and regulatory requirements. This sandbox will however have to meet certain evaluation criteria (technologically innovative; benefit consumers and address a significant problem or issue; intention and ability to deploy the solution in Singapore on a larger scale; report to the MAS on the test progress; major foreseeable risks have to be assessed and mitigated; etc.).

In April, the country expressed its desire to become the leading hub in Asia for blockchain-technology and fin-tech start-ups. MAS aims to provide a responsive and forward-looking regulatory approach that will enable promising fin-tech solutions to develop and flourish. The sandbox will help reduce regulatory friction and provide a safer environment for fin-tech experiments.

- Abu Dhabi FSRA seek blockchain start-ups for fintech sandbox

The Financial Services Regulatory Authority (FSRA), the independent regulatory authority of Abu Dhabi’s newest financial free zone, has released a consultation paper in which it detailed its plans to create a sandbox environment for fin-tech under which start-ups would be allowed to work under a flexible regulatory framework for up to two years. The FSRA is seeking to promote the development of blockchain start-ups as part of a drive to create new efficiencies in the regional financial sector.

The FSRA’s proposal would seek to limit start-ups accepted into the program to those that “promote significant growth, efficiency or competition in the financial sector”. To give some clarity where they are focusing on the paper goes on to cite examples of technologies that fit this description.

“The advent of robo-advisers that offer lower costs, simplicity and real-time portfolio analytics and monitoring; or leveraging on the application of blockchain technology and distributed databases to facilitate price discovery, smart contracts, settlement of financial transactions, etc that may lead to safer [and] better products, and higher productivity and growth.”

Benefits for startups

The benefits of these regulatory sandbox are manifold. Both start-ups, the whole industry and regulators may profit.

There ought to be clear benefits :

- First of all from a time and cost point of view.

Most immediately, the ability of businesses to safely test their products and also be engaged in direct dialogue with the regulator without first having to expend time and money on a speculative application for regulatory authorisation should relieve start-ups of high costs they often cannot afford.

- From a compliance point if view

At the same time, the businesses can adapt their offerings to better ensure regulatory compliance.

- From an investor point of view

Once through the process, and assuming the road-testing has produced a successful outcome for the business, the task of attracting investors should be simpler as a major unknown will have been removed.

- From a financial industry point of view

The regulatory sandbox may help to foster innovation in financial services and that is good for the whole industry and their customers.

- From a regulatory point of view

With the insight and knowledge obtained from that role, the regulator will be better placed to assess the changes necessary to evolve the regulatory environment to not only better regulate these businesses, but also continue to ensure that the legislation does not frustrate the competition that the FCA wishes to promote.

Global regulatory collaboration

Given its global reach, the level of complexity and the interconnectedness of financial markets, and the level of complexity and the interconnectedness of financial markets, regulatory bodies worldwide should collaborate to ensure that no different regulatory environments are created and regulatory arbitrage is excluded. National and foreign regulators must coordinate to create a common principles-based approach for blockchain oversight A special role should be given to bodies like the IOSCO and the G-20 Financial Stability Board.

Economist and researcher

Simon Knappstein

Simon Knappstein The B2B Fintech: Payments, Supply Chain Finance & E-Invoicing Guide 2016 has been released by the

The B2B Fintech: Payments, Supply Chain Finance & E-Invoicing Guide 2016 has been released by the

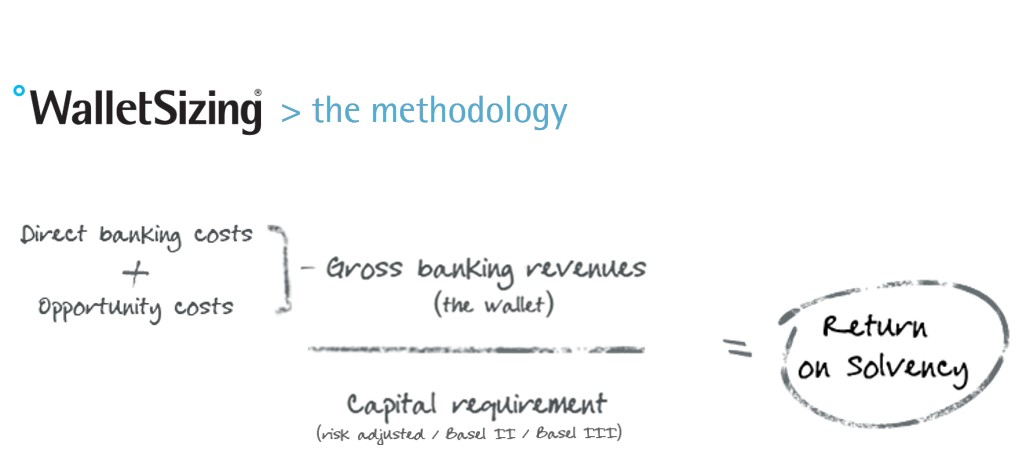

On april 13th of this year the Fintech innovation awards took place. Vallstein won the innovation award in treasury management with their Walletsizing® system. We asked Huub Wevers from Vallstein to give us an update on this new system. What’s new about it and who will benefit from using Walletsizing®?

On april 13th of this year the Fintech innovation awards took place. Vallstein won the innovation award in treasury management with their Walletsizing® system. We asked Huub Wevers from Vallstein to give us an update on this new system. What’s new about it and who will benefit from using Walletsizing®?

Huub Wevers is responsible for Corporate Solutions at Vallstein, the leading Bank Relationship Management specialist. Before joining Vallstein he has had eighteen years of experience in Banking at ABN AMRO and RBS, notably Transaction Banking. His responsibilities included Product Management, Account Management, Implementation and Operations, whereby his last role was the leadership of all Service & Operations in EMEA for RBS. At Vallstein Huub is responsible for building out the software solutions that Vallstein offers for corporates. Solutions that automate bank relationship management in order to assess the profitability that a corporate has for their banks, using all banking products and Basel III.

Huub Wevers is responsible for Corporate Solutions at Vallstein, the leading Bank Relationship Management specialist. Before joining Vallstein he has had eighteen years of experience in Banking at ABN AMRO and RBS, notably Transaction Banking. His responsibilities included Product Management, Account Management, Implementation and Operations, whereby his last role was the leadership of all Service & Operations in EMEA for RBS. At Vallstein Huub is responsible for building out the software solutions that Vallstein offers for corporates. Solutions that automate bank relationship management in order to assess the profitability that a corporate has for their banks, using all banking products and Basel III.