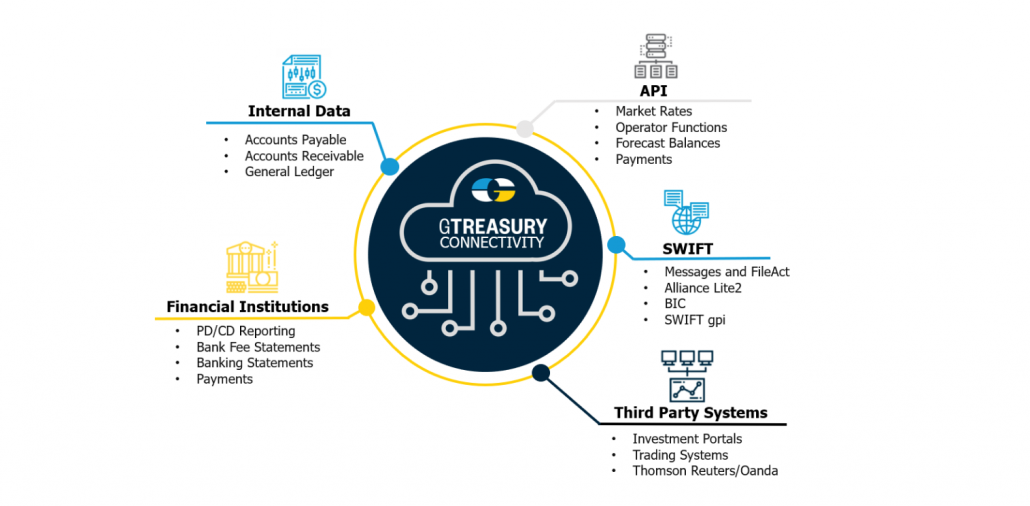

GTreasury Launches New Connectivity Suite for Treasurers

12-07-2022 | treasuryXL | GTreasury | LinkedIn |

Workflow Brings in Third-Party Banking, Payments, and Financial Data

ClearConnect ensures the fidelity of data essential to treasurers and CFOs

CHICAGO, Ill. – July 12, 2022 – GTreasury, a treasury and risk management platform provider, today announced the launch of ClearConnect. Featuring more than 80 API calls in a dozen key categories, ClearConnect offers the most robust connectivity suite available to treasury teams and the office of the CFO. The solution provides immediate access to the comprehensive data required for confident and actionable treasury insights, and ensures the fidelity and security of that data through purpose-built connections bolstered by GTreasury’s support.

While “API” is becoming a buzzword often associated with data connectivity solutions, the terms are not synonymous. API connections are only as powerful as the underlying workflows that support them. Activating an out-of-the-box API is not an instant panacea for an organization’s data needs. Without the right underlying workflows, APIs not attuned to a business’s specific requirements will drop or fail to capture all the data sets necessary to power effective analytics and data lakes. Given the complexity of treasury and risk management, those missing insights can result in significant consequences for treasury teams and CFOs.

ClearConnect provides both the powerful underlying workflows and the multifaceted purpose-built API-enabled connectivity to ensure that data capture is consistently done correctly and thoroughly—providing all the analytics an organization needs from a particular connection. The solution creates certainty, security, and seamless connections by integrating all data from business systems and financial institutions, and is capable of combining connection types for uniquely complete data sets and data fidelity.

Specifically, ClearConnect creates value for treasury teams and the office of the CFO by delivering:

- Secure connectivity across the financial value chain

- Extensions to corporate treasury workflows

- Access to specialist solutions within the integrated platform

- Lower bank fee costs through seamless connectivity

- Access to multiple innovative FinTech products and services

ClearConnect’s market-leading API catalog features over 80 API calls, augmented by host-to-host connectivity wherever needed to bolster capabilities. The solution enables robust functionality across a dozen categories, including payment approval rules, payment workflows, payments and templates, balances and transactions, general ledgers, deal management, bank accounts, bank account management, legal entities, forecasts, operators, and data extracts. ClearConnect’s flexible connectivity architecture uses best-in-class API-enabled connections to ensure fidelity and continuity of customers’ most vital data. Connectivity into Swift, Fides, and others provides a single source of truth and visibility into an organization’s cash and financial risk, and delivers transparent workflows for payments, bank file monitoring, and more.

GTreasury’s always-expanding partnerships with leading global financial institutions and market data partners ensure seamless bank and ERP connectivity, domestic and international transactions, and access to market insights. As client needs change, GTreasury’s active collaborations with product partners further ensure the creation and delivery of modernized products and services, securing ClearConnect’s place as a market-leading solution always aligned with customers’ current data requirements.

From risk management capabilities powered by Moody’s Analytics and KYOS, to market data provided by Refinitiv and Fenics MD, to banking, ERP, investments, and payments partners, ClearConnect now enables customers to wield the full power of the GTreasury ecosystem even more easily and completely.

“ClearConnect doesn’t just offer a significantly greater breadth of connectivity options than anything else available, it also underwrites those capabilities with foundational workflows for data integrity and ease of use,” said Pete Srejovic, Chief Technology Officer at GTreasury. “Investing in API technology only to realize that you are dropping crucial data is a nightmare that has come true for many CFOs and treasury teams. With today’s launch of ClearConnect, we’re proud to offer not only the largest and most powerful API connectivity solution on the market, but one that customers can entrust to deliver absolute data integrity along with the comprehensive and future-proof solutions of the GTreasury ecosystem.”

![]()

About GTreasury