CHICAGO, Ill. – June 21, 2022 – GTreasury, a treasury and risk management platform provider, today announced that it has named Victoria Blake as GTreasury’s Chief Product Officer, and Ashley Pater as General Manager at Hedge Trackers. Recently acquired by GTreasury, Hedge Trackers is the global leader in accounting, consulting, and software services that protect clients against financial risk.

Victoria Blake joins GTreasury with more than 20 years of experience and success in product leadership roles across several SaaS and technology companies. Blake comes to GTreasury from Zapproved, where she served as the Vice President of Product. During her tenure at the e-discovery software provider, she led high-level strategy development, product definition, and market-facing thought leadership and vision. Before Zapproved, Blake was responsible for defining next-generation cloud services offerings as the Vice President of Product Management at Metal Toad, an AWS Consulting Partner. Blake has also held product management and leadership positions at WebMD Health Services, Jive Software, and Walker Tracker.

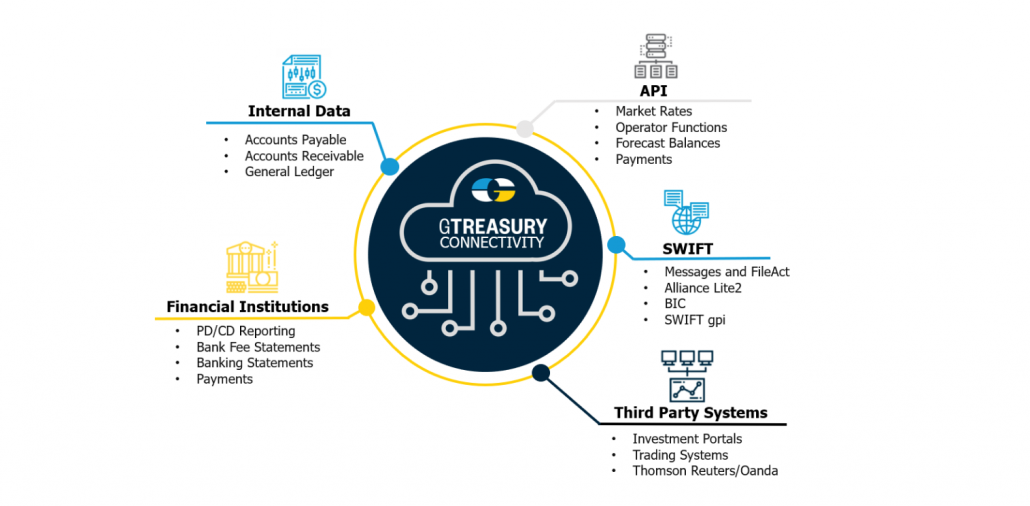

As GTreasury’s Chief Product Officer, Blake will lead the company’s global product and UX teams in developing and delivering innovative new solutions for GTreasury’s customers and partners. From modern automated treasury and transaction management to AI-powered SmartPredictions™ cash forecasting and visibility, GTreasury’s SaaS platform empowers treasury teams and the office of the CFO with the future-proof technology and capabilities required to drive confident financial decision-making. GTreasury has also continued to expand its broad ecosystem of connected partner technologies, via API integrations with ERPs, banks, and other external providers where instant data connectivity maximizes customer efficiencies.

“GTreasury has built its reputation as a leading treasury and risk management platform by harnessing innovative cloud, AI, machine learning, and emerging technologies that move our industry forward,” said Victoria Blake, CPO, GTreasury. “Just as importantly, GTreasury has always focused on product usability and ensuring that its powerful tools are always easily accessible and seamlessly connected for the teams that rely on them. I look forward to building on what GTreasury has created over the past three decades, and delivering even more next-generation tools to make CFOs and treasury teams more successful.”

Ashley Pater is now the General Manager of Hedge Trackers after more than a decade of leadership roles within GTreasury. Pater most recently served as GTreasury’s Chief Product Officer, where she was responsible for aligning product vision and strategy to the company’s business objectives. Pater previously held leadership positions in GTreasury’s marketing and account management functions, focusing on building global brand awareness, lead generation, event management, and cross-sell programs.

Pater will oversee daily business operations and lead growth strategy around Hedge Trackers’ FX, interest rate, and commodity price risk management services and consulting. Pater will also ensure alignment and integration opportunities within the broader GTreasury organization. Hedge Trackers offers best-in-class expertise and technical depth in meeting today’s unprecedented demand for effective hedging strategies, identifying exposure, managing risk, and meeting compliance and audit requirements. Under Pater’s leadership, Hedge Trackers will focus on bolstering its risk management expertise and bringing new solutions to market across the company’s risk product suite.

“Combining the strengths of GTreasury and Hedge Trackers makes us the clear market leader when it comes to both our treasury risk management products and our consulting acumen,” said Ashley Pater, General Manager, Hedge Trackers. “Today’s CFOs and financial leaders understand that risk management and hedging capabilities are critical to navigating volatile markets and achieving larger business goals. I’m excited to further our solutions and insight to equip customers with the solutions required for effectively and cost-efficiently managing their risk.”

“Both Victoria and Ashley possess the clarity of vision required to advance our GTreasury and Hedge Trackers products to meet our customers’ evolving needs today and well into the future—and both bring relevant, experienced, and proven leadership to accomplish those goals,” said Renaat Ver Eecke, CEO, GTreasury. “I’m glad to welcome Victoria and Ashley into their new roles and look forward to what’s to come from GTreasury and Hedge Trackers.”

About GTreasury

GTreasury is committed to connecting treasury and digital finance operations by providing a world-class SaaS treasury and risk management system and integrated ecosystem where cash, debt, investments and exposures are seamlessly managed within the office of the CFO. GTreasury delivers intelligent insights, while connecting financial value chains and extending workflows to third-party systems, exchanges, portals and services. Headquartered in Chicago, with locations serving EMEA (London) and APAC (Sydney and Manila), GTreasury’s global community includes more than 800 customers and 30+ industries reaching 160+ countries worldwide. Visit GTreasury.com