Award-winning Fintech company, SurePay, integrates the IBAN-Name Check into your business processes. This prevents fraud and errors and allows you to realize more efficient processes.

SurePay was founded in 2016 and has been providing the IBAN-Name Check to all major Dutch banks since 2017. In the years that followed, the group of customers expanded to corporates and partners. Today, SurePay provides the Confirmation of Payee service in the UK, while at the same time introducing new services in the Netherlands. At the beginning of 2020, SurePay became a Private Company and an independent part of the Rabobank Group.

Experience the benefits of the IBAN-Name Check in your business processes

Entering, using and checking customer data is often labor-intensive. By integrating the SurePay IBAN and name check into your systems, you make your processes more efficient, safer and reduce the risk of fraud.

This way, the online registration of new customers runs more smoothly, you collect from and you pay to the right person. Moreover, you know whether you are dealing with a private or business account! Various organisations, like insurers, municipalities and energy companies already use the IBAN-Name Check for organisations. The same solution makes sure that the Covid-19 payments are delivered safely, at scale and to the right people in both the Netherlands and the UK.

2020 recap at a glance

SurePay saw a spectacular growth of 1719% in the number of checks for organisations. More than 125 organisations now use the IBAN-Name Check.

They use the service in the onboarding process of new suppliers and customers (KYC), in claims and payout processes, in direct debit processes and in fraud investigations. This makes processes more efficient, safer and reduces the risk of fraud and misdirection, avoiding all the damage and hassle that goes with it.

The results are impressive:

90% less drop-outs during onboarding

80% less fraudulent onboardings

50% less uncollectible invoices

Want to know more about the IBAN-Name Check for Organisations?

To know more about the IBAN-Name Check like features, roadmap, use cases and the team behind this proven solution, click on the following banner.

Thanks for reading, take care.

https://treasuryxl.com/wp-content/uploads/2021/02/Ontwerp-zonder-titel-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-24 07:00:512023-10-31 10:58:56SurePay | Prevent fraud and errors with The IBAN-Name Check for Organisations

23-02-2023 | Aastha Tomar | treasuryXL | LinkedIn | After two years of hiatus, here I am again to write for the team I love the most and the team whom I owe the most in Netherlands. treasuryXL has a special place in my heart, I got linked with them as soon as I shifted to Netherlands in 2019 and since then they have been a constant source of support for me.

https://treasuryxl.com/wp-content/uploads/2023/02/aastha-blog-200x200-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-23 07:00:152024-12-10 10:52:45What is Treasury in Banking?

22-02-2023 | treasuryXL | LinkedIn | On January 24th, 2023 we hosted a joint webinar with our partner Kantox about the Currency Management Priorities for 2023. In this 45 minute session we take you through the key trends and opportunities in currency management.

https://treasuryxl.com/wp-content/uploads/2023/02/Kopie-van-Kantox-webinar-2023.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-22 07:00:542023-02-22 09:27:09Recording | Your Currency Management Toolkit for 2023

When left unaddressed, foreign currency risk can wreak havoc on your bottom line. But it doesn’t have to be this way. To keep foreign currency fluctuations under control and drive predictability in financial statements, many companies turn to FX hedge programs.

Here are 5 frequently asked questions about foreign currency risk and FX hedge programs.

#1. What is Foreign Currency Risk?

Foreign currency gains and losses occur when a company transacts in a currency other than their home currency.

A foreign currency transaction results in either a payment or receipt of that currency and the amount of U.S. dollars it will take to pay the payment or collect from the receipt changes with exchange rates.

When companies have hundreds or thousands of these types of transactions, the gains and losses due to the exchange rates can add up quickly.

#2. Are Gains from Foreign Currency Fluctuations a Good Thing?

Even though a large gain on your bottom line seems appealing – especially compared to a large loss – it also indicates instability in your financial statements month-over-month and year-over-year. Not to mention, the nature of fluctuating exchange rates means times of gains are temporary and large losses are inevitable.

An FX hedge program protects the amount of home currency needed to make a foreign payment or receive from a foreign currency collection. In doing so, it eliminates a majority of the foreign currency gain and loss noise in financial statements you may have been experiencing. Large swings in either direction will no longer happen, which means you’re able to explain your true business results more effectively to your Board.

#4. Does a Hedge Program Create Zero FX Gain/Loss?

A hedge program doesn’t mean zero FX, but it does reduce a majority of the fluctuations. What’s left over can be explained by a handful of “buckets” – such as un-hedged currency impacts or under-hedging a currency amount.

#5. Can an FX Hedge Program be Implemented Quickly?

Yes! Starting a hedge program can be done quickly. Many times, a foreign currency risk problem can be fixed in just a few weeks or months – especially when you work with a partner that puts programs together every day. Supported by automation, your FX hedge program can get up and running fast – and continue to run seamlessly from there.

Conclusion

Companies operating internationally are exposed to currency risk – a risk to earnings driven by changes in currency exchange rates. The ones that hedge their currency risk have certain advantages over non-hedgers. For example, instead of just experiencing the changing exchange rate impacts, these companies are afforded predictable results and time to react to changes.

If you’re curious about implementing a hedge program or just got tasked by your Board to fix a problem Hedge Trackers can help – and fast.

https://treasuryxl.com/wp-content/uploads/2023/02/gtreasury-20e-200-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-20 07:00:192023-04-03 13:31:43Is Your Foreign Currency Risk Out of Control? 5 FAQs

Join us for a thought-provoking Live Session on Interim Treasury Management, where our experts will delve into the pros and cons of this exciting market.

Unlock the Benefits of Interim Treasury Management: Discover Why it’s a Must-Have for Your Business!

13-02-2023 | Dinesh Kumar | treasuryXL | LinkedIn | Imagine a setting where your treasury management system (TMS) and enterprise resource planning (ERP) system work together seamlessly, like a well-oiled machine. In this case, your treasury team has real-time visibility into financial transactions and can make informed decisions quickly and efficiently. The process of connecting a TMS to an ERP system may seem daunting, but it’s a crucial step in achieving a more streamlined, efficient and accurate corporate treasury operation.

https://treasuryxl.com/wp-content/uploads/2023/01/dinesh-200.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-13 07:00:002023-08-31 14:48:44How to connect your TMS to your ERP? A Comprehensive Guide by Dinesh Kumar

09-02-2023 | The year’s second edition features a discussion on the newest treasuryXL poll results, including a review of treasurer voting patterns and expert perspectives on effective currency management.

https://treasuryxl.com/wp-content/uploads/2023/06/poll-results-8-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-09 12:00:512023-06-13 10:19:28What is a successful Currency Management Strategy?

Join senior treasury peers on March 7th in London at EuroFinance’s 10th annual Effective Finance & Treasury in Africa. Understand changing developments and the unique opportunities and challenges of doing business in this dynamic region.

This year’s speaker line-up includes experienced treasurers – all active in African markets – including:

● Edward Collis, Treasurer, Save the Children

● Neiciriany Mata, Head of finance, Angola Cables

● Marta de Teresa, Group treasurer, Maxamcorp

● Chigbo Enenmo, Finance and treasury manager, Nigeria LNG

● Folake Fawibe, Integrated business service lead, Danone, Southern Africa

● Jan Beukes, Group treasurer, MultiChoice Group

They will discuss important topics including cash and FX, payments, liquidity and financing, digital transformation, share success stories and provide practical guidance on how to optimise your treasury operation for growth.

For the full agenda and to register, please visitt this link.

Quote discount code MKTG/TXL10 for an exclusive 10% discount for TreasuryXL readers.

If you have any questions, you can contact the EuroFinance team directly at [email protected].

https://treasuryxl.com/wp-content/uploads/2023/02/eurofinance-200.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2023-02-07 07:00:202023-02-06 10:33:56Effective Finance & Treasury in Africa | Eurofinance

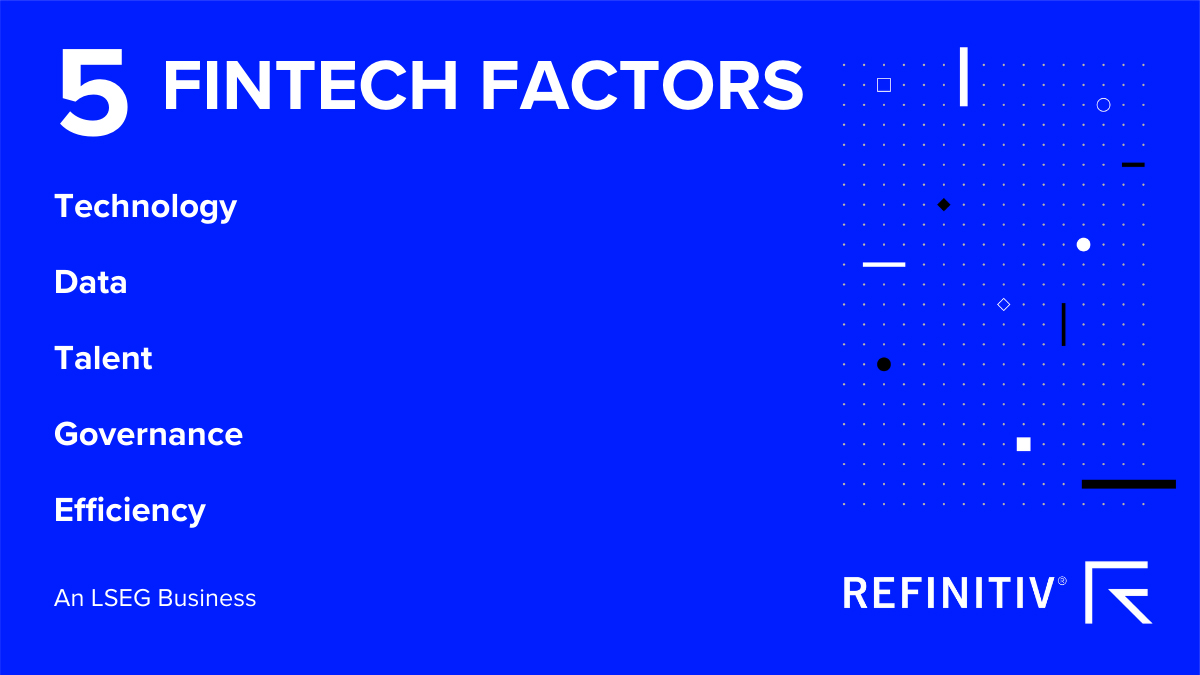

A recent white paper from Refinitiv – produced in collaboration with global consultancy, FINTRAIL – discusses the key elements currently shaping the evolving fintech space and the key trends that will be shaping the fintech landscape in 2023.

New findings from Refinitiv and FINTRAIL, based on interviews with experts from different fintechs across a range of geographies, have identified five key factors that are shaping fintechs today.

The white paper identified that the primary factors shaping fintech in 2022 were technology, data, talent, governance and efficiency, and it will continue in 2023.

Fintechs also have to keep tight control of the anti-money laundering (AML) processes to protect against widespread illicit activity and ensure regulatory compliance.

The fintech industry is one of dynamism and innovation; a space where agile players harness new technology and challenge the status quo of the traditional financial services industry every day.

Undoubtedly, this delivers substantial opportunity for those involved in the sector, but at the same time, financial criminals are similarly leveraging technology and using advancements to devise new ways to further their illicit activities.

In this fast-paced space, characterised by evolution and a growing financial crime threat, what key elements are at play and what factors have shaped and defined the industry in 2022, and will continue to do so in 2023?

Findings from Refinitiv and FINTRAIL, based on interviews with experts from different fintechs across a range of geographies, have identified five key factors that are shaping fintechs today.

Five factors shaping fintechs today

Technology

The fintechs we spoke to stress that the right technology can make all the difference when it comes to managing financial crime, with some describing machine learning and artificial intelligence (AI) as “indispensable tools”.

This view is in line with the recommendations of the Financial Action Task Force (FATF).

Leading technology needs trusted, comprehensive data, but fintechs highlight that striking a balance is key. Requiring too much information can damage the customer experience, while not enough leaves fintechs vulnerable to financial crime.

Collecting the right data – and the right amount of data – and then building a complete picture of risk is key to the combined fintech goals of maximising efficiency, keeping customers happy and protecting against financial crime.

Talent

Technology and data are critical in managing financial crime threats, but a third and equally critical element is invaluable human expertise. The right people across difference disciplines can make all the difference.

Those we interviewed said that engineers and data scientists are key, and further that the compliance profession is considered “recession-proof” – upskilling compliance team members should be a key priority for those in the sector.

Interviewees also highlighted that fintechs should concentrate on attracting and retaining key staff, but should also consider outsourced solutions for additional support and expertise.

Governance

Effective governance is a key consideration for fintechs as they grow and evolve. The nature of the industry and the rapid growth trajectories often followed by sector participants mean that effective AML controls and good governance need due attention.

Plus, fintechs agree that governance models should not be static – they need to adapt over time.

Efficiency

Efficiencies are increasing in the industry, with new technology now enabling fintechs to integrate specific data points alongside behavioural biometrics to help them spot suspicious activity.

For example, device identification data can identify if an account is accessed from a new device and this can be compared to a client’s history.

To further boost efficiencies, fintechs say that adopting a dynamic approach to risk is key and avoids wasting often scarce resources.

Discover more about our KYC and anti-money laundering solutions for the fintech industry

Keeping pace with changes in fintech

Fintechs can expect these top trends to continue in the year ahead and should especially take note of the powerful combination of tech, data and human expertise that are not only shaping the sector, but can enable better compliance and good governance, while boosting efficiencies.

As the industry continues to grow and develop at pace, many players are rightly concerned with ensuring an engaging and positive customer experience that offers connectivity and seamless interaction. They must, however, also keep tight control of the AML processes they will need to protect against widespread illicit activity and ensure regulatory compliance.

Cash flow and working capital are the lifeblood of your business. How are you protecting your cash positions and reducing risk in these times of increasing business volatility?

Today’s digital cash visibility and forecasting solutions provide amazing opportunities for companies and their decision-making processes. In this webinar, we provide an in-depth look at how these modern solutions help you, your department, and your company reach your full potential.

Jake Fernandez, GTreasury – Product Manager, will discuss:

The pros and cons of common cash forecasting practices using spreadsheets and ERPs.

How a modern treasury management platform can provide immediate value for cash visibility and forecasting.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them: