| 14-11-2017 | treasuryXL |

Every day we enter into transactions in our own domestic market. Goods are priced in our own currency and we settle purchases in our own currency. Here in the Netherlands that means everything is priced and settled in Euro’s. It is a clear and concise system – of course we might argue about the price of goods, but that is another matter. Now consider what happens when we sell our goods to a counterparty domiciled in a different country – we shall assume from the United States. We would prefer to invoice in EUR as this is our domestic currency, whilst our counterparty would prefer to settle in USD. This makes sense as in both instances neither of us would be exposed to fluctuations in the exchange rate between the EUR and USD.

There are 3 basic choices to trade with a foreign based counterparty:

- Price in our currency, but run the risk that they will not trade with us

- Price in their currency, win the trade but do nothing about the risk

- Price in their currency, but adjust our price for the perceived FX risk and sell their currency for our currency as soon as the deal is closed

As we are keen to expand our export markets we agree to charging the buyer in USD, but what price should we charge in USD? By accepting payment in USD we are now assuming a foreign exchange risk as the value of the USD could fall in relationship to the EUR before we have sold the USD for EUR. If the fall was large it could take away all our profit from the original transaction, possibly even leading to a loss on the order.

We must therefore enter into a transaction to sell USD and to receive EUR to book our profit and to neutralize the FX risk. This leads us into the world of Foreign Exchange (FX) trading.

In FX trading quotations are always shown for a pair of currencies such as EUR/USD – but what does this mean?

- The first currency – EUR – is called the base currency

- The second currency – USD – is called the quoted currency

- The spot rate is shown as 1.1595

- This means that every unit of the base currency is equal to 1.1595 units of the quoted currency

If our order was for EUR 100.000,00 then the USD equivalent would be USD 115.950,00

In this example it is the USD price that fluctuates as it is the quoted currency, but this does not mean that fluctuations are only caused by changes in the value of USD. The value can also fluctuate because of changes in the value of EUR – even though this is the base currency.

Most major currency pairs are quoted to 4 decimal places – with the 3rd and 4th places being called “pips”. Pips are the expression traders use to describe their profit or their market spread.

If we traded EUR 1 million into USD, we would have an equivalent of USD 1.159.500,00

The value of 1 “pip” would be USD 100,00

When we approach a bank for a quotation in spot EUR/USD, the bank quotes a 2-way price such as 1.1592/97

The lower price – 1.1592 – represents the bank’s bid price. This is the price at which the bank buys EUR and sells USD.

The higher price – 1.1597 – represents the bank’s offer price. This is the price that at which the bank sells EUR and buys USD.

If the bank quoted this price into the market and one clients hit the bid at 1.1592 and another took the offer at 1.1597, both in EUR 1 million, then the bank would book a profit of USD 500,00 – or a profit of 5 pips on EUR 1 million.

FX is one of the largest markets in the world – daily turnover exceeds USD 5 trillion per day. That means 5 followed by 12 zeros – every working day.

With such a large daily turnover, prices are constantly changing. The market consists of price makers (who make the prices), price takers (who take the prices), intermediaries like brokers who assist the market by transmitting the prices and placing orders, and clients who place orders at specific levels. Prices are only valid for a few seconds before they change either because the market has traded on the quoted price or a new order replaces the existing price.

When you trade on the quoted price then you have entered into a binding contract with the counterparty. Settlement is normally 2 working days after the trade date. If you sell USD then you must ensure your counterparty receives the agreed USD amount on their account in 2 working days, and you receive the agreed EUR amount on your account in 2 working days.

Trade settlement is very important and means that you must have a complete operational procedure in placing to effect settlement, establish positions, agree counterparties, have trading limits etc.

Traditionally spot FX trades were done with banks. Now trades can also be transacted via electronic exchanges, electronic brokers etc. It is always important to know who your counterparty is – it could be that your internal operational control prohibits you from trading with specific counterparties.

Most major currencies can be traded against each other without restrictions such as exchange control. Therefore, currency pairings can be found everywhere such as USD/JPY and EUR/GBP and ZAR/CHF.

Spot FX transactions are not traded on listed exchanges; these trades occur “over the counter” with a clearly identifiable counterparty.

Lionel Pavey

Cash Management and Treasury Specialist

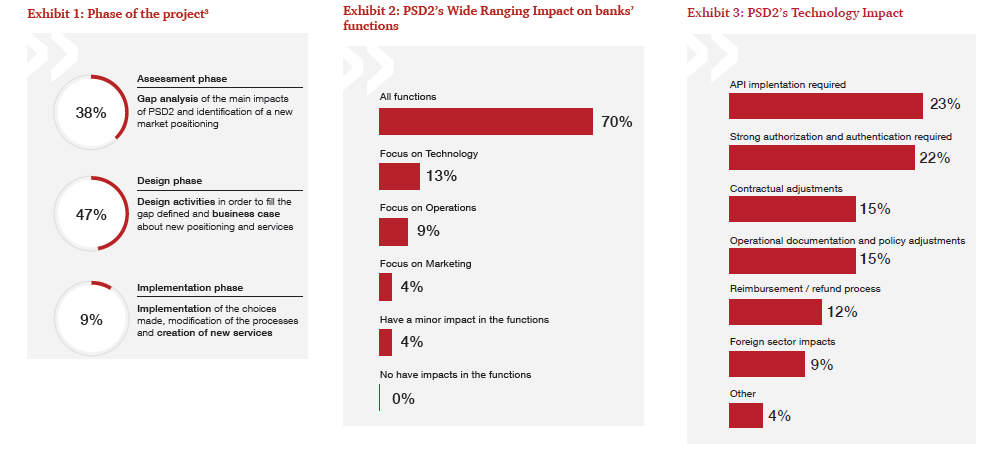

In 2018, when PSD2 comes into force, banks will lose their monopoly on payment services and customer’s account details. Bank customers will be able to use third-party providers (TPP) to administer their payments. When a customer agrees on using the services of a TPP, then their bank has to give access to TPPs to their accounts. TPPs are then able to build and offer services that compete with the existing bank services. During the summer 2017, I published a Summer Update on PSD2. Since then, a lot of things have moved, and hence I found it the right moment to provide an update to you on some developments on PSD2, in this area.

In 2018, when PSD2 comes into force, banks will lose their monopoly on payment services and customer’s account details. Bank customers will be able to use third-party providers (TPP) to administer their payments. When a customer agrees on using the services of a TPP, then their bank has to give access to TPPs to their accounts. TPPs are then able to build and offer services that compete with the existing bank services. During the summer 2017, I published a Summer Update on PSD2. Since then, a lot of things have moved, and hence I found it the right moment to provide an update to you on some developments on PSD2, in this area.

François de Witte – Founder & Senior Consultant at

François de Witte – Founder & Senior Consultant at

The DACT (Dutch association of Corporate Treasurers) will be holding their annual Treasury Fair in Noordwijk at the Hotel van Orange on 23rd and 24th November 2017 – the most important annual treasury event in the Netherlands. Discover treasury best practices, learn about the latest trends and exchange experiences. It will contain 9 practical workshops throughout the day on topics including, trade finance, supply chain finance, liquidity forecasting, cyber security and the Blockchain. There are more than 50 exhibitors present at the Trade Fair including Cashforce – a partner of treasuryXL, who are also presenting a Workshop.

The DACT (Dutch association of Corporate Treasurers) will be holding their annual Treasury Fair in Noordwijk at the Hotel van Orange on 23rd and 24th November 2017 – the most important annual treasury event in the Netherlands. Discover treasury best practices, learn about the latest trends and exchange experiences. It will contain 9 practical workshops throughout the day on topics including, trade finance, supply chain finance, liquidity forecasting, cyber security and the Blockchain. There are more than 50 exhibitors present at the Trade Fair including Cashforce – a partner of treasuryXL, who are also presenting a Workshop. The DACT (Dutch association of Corporate Treasurers) will be holding their annual Treasury Fair in Noordwijk at the Hotel van Orange on 23rd and 24th November 2017 – the most important annual treasury event in the Netherlands. Discover treasury best practices, learn about the latest trends and exchange experiences. It will contain 9 practical workshops spread out throughout the day on topics including, among others, trade finance, supply chain finance, liquidity forecasting, cyber security and the Blockchain. There are more than 50 exhibitors present at the Trade Fair including Tipco Treasury & Technology GmbH- a partner of treasuryXL.

The DACT (Dutch association of Corporate Treasurers) will be holding their annual Treasury Fair in Noordwijk at the Hotel van Orange on 23rd and 24th November 2017 – the most important annual treasury event in the Netherlands. Discover treasury best practices, learn about the latest trends and exchange experiences. It will contain 9 practical workshops spread out throughout the day on topics including, among others, trade finance, supply chain finance, liquidity forecasting, cyber security and the Blockchain. There are more than 50 exhibitors present at the Trade Fair including Tipco Treasury & Technology GmbH- a partner of treasuryXL.