Alternative Risk Finance Part 3 – Cell Company 101

| 02-11-2020 | Mark Roelands | treasuryXL

The introduction to a most utilized form and key alternative to a traditional captive

As described in this series: an in-house insurer can be of great added value to your company. In the current hard insurance market, the possibility to utilize an own vehicle instead of the turbulent market is a direct and tangible benefit. But it is not a free alternative, the cost of setup of an insurer and operating it in a compliant manner might be too high to generate an overall positive business case. That issue is being addressed in utilising a centralised facility taking care of a.o. most of capitalisation and compliance matters, while the risk taker can operate an in-house insurer. This light-weight route is what can be named a “Cell Company”.

A Protected Cell Company, Incorporated Cell Company, Segregated Accounts Company, Segregated Portfolio Company are all different names for a centralised facility each buidling on local legislation, which we will collectively name “Cell Companies”.

In this part of the series of Alternative Risk Financing the generalised concept of a Cell Company is described.

Structure explained

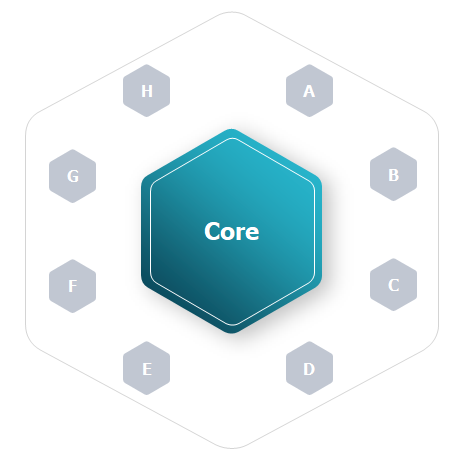

Where a fully-owned captive insurance entity imposes the full requirements on the parent company, the Cell Company utilises a centralised facility, a “Core”, which provides the infrastructure to be leveraged by multiple insurance entities. In the illustration the full hexagon is the Cell Company, with the Core representing the infrastructure.

The Small grey hexagons represent the Cells, which are segregated units within the facility and which belong to a specific client. Assets and Liabilities and legally segregated from other Cells and the Core. Cell A will for instance belong to Company A, while Cell B belongs to Company B. In most Cell Company structures the number of cells is not limited to 8 but is practically unlimited. In order to generate the segregation a split is made between Cellular Assets and Cellular Liabilies (the A-H hexagons) and non-cellular assets and liabilities (The Core).

Owning Cell A will enable a client to participate in an insurance program in a compliant manner, while building on the centralised facility which provides both a compliant governance structure, as well as the required capital amount.

As an individual client a key requirement however is to fund the ‘risk gap’, any open underwriting exposure being retained by the Cell needs to be collateralised somehow. Either via a guarantee. Letter of Credit, Capital or perhaps reinsuring more of the cover. This also ensures that each cell is able to sustain itself.

Key question: Is it safe?

Leveraging on the infrastructure of another company, which also facilitates other companies raises the obvious question: is it safe? Are my funds secure, and can I be held liable for the liabilities of other companies?In short: Yes it is safe … but …it builds on carefully drafted agreements, hence careful due diligence is required.

Basically, it comes down to default legislation of the domicile involved. In the Netherlands for instance there is no separate legal form of a Cell Company, and legal segregation critical fort he structure cannot be achieved. In Malta the for instance the “Cell Companies Act” recognizes the type of entity and segregation involved. A recent Montana case also recognized the structure including legal segregation.

Domiciliation

As mentioned several times, in order to make use of a Cell Company, legislation needs to be in place recognizing this particular form of a captive. Domiciliation is one of the the key considerations when an alternative risk finance structure is considered, as has been explain in Part 1 and Part 2 of this series.

In the Netherlands the required legislation for a Cell Company is not available. Within Europe therefore either Malta, Guernsey, Isle of Man or Gibraltar needs to be utilised. With Malta having the edge being within the EU. Ireland and Luxemburg have hinted on establishing Cell Company legislation as well, but Brexit (and moving insurance companies into these domiciles) has shifted supervisory priorities and no information has been published on any plans for a few years now. While Vermont is often the go to domicile within the US, there are more States with Cell Company legislation like Montana. Establishing a Cell Company close to an office of your company could be regarded to be beneficial. Vermont however does have an extensive captive servicing industry which is also a benefit.

Within Asia Vanuatu or Labuan would be interesting domiciles and the popular captive domiciles of Bermuda and Cayman Islands also both enable Cell Companies, and both have a solid supporting industry. This however needs to pass tax requirements in the organisation.

What’s next?

In Part 1 and Part 2 Captive Insurance and Building the Business Case is described. A Cell Company can possibly allow a business case to be positive, as the cost of operating and capitalising the Company is much lower then a fully-owned Solvency II compliant Insurance company. For building the business case please review Part 2, but when considering a Cell Company also take the following into consideration:

- Due diligence on the Cell Company itself

- Lock-in effects with a facility provider: brokers and insurers provide the facilities, but there are also some independent facility providers

This may unlock the potential for an in-house insurer allowing you to pool your risks centrally and finance them in the most efficient manner, while operating in the most light weight manner.

Check my previous blogs of this serie:

- Alternative Risk Finance in a hardening insurance market

- Alternative Risk Finance Part 2 – Building the Business Case

Risk and Compliance Specialist

")