Alternative Risk Finance Part 4 – Risk Trading and the Future of Insurance within Treasury

| 07-12-2020 | Mark Roelands | treasuryXL

Intro

This series on alternative risk financing has been about alternatives to traditional insurance, which get are more important role in the current hard insurance environment. How to build the business case is explored in Part 2 and the alternative structure of Cell Companies is explained in Part 3. The last part of the 2020 series is about the future of alternative risk financing, risk trading and the role of treasury in insurance.

In a data driven era, with rapid advancing capabilities there may be more efficient manners to transfer or share risk, insight into risk scan be increased as well as the subsequent possibilities to retain or transfer. Although this is an outlook into the (not too distant) future, it is important to be aware of developments and get into the position to benefit from these developments preparing for 2021 and beyond, the hard market isn’t just a 2020 phenomenon.

Treasury Risk Management

Obviously, risk management is a critical part of Treasury processes. The scope of risks to be managed however within Treasury varies significantly between companies. Common risks in scope include operational risks within payment processes and financial risks like currency risk and interest rate risk. Insurable risks (like property damage and general liability) can be part of Treasury responsibilities, but can be part of legal or enterprise risk as well. Often this relates the the nature of the business as well as the size of the company. For instance, high liability type of businesses often have insurance within a legal function.

With advances in data as well as the analytics capabilities it is possible to expand the scope of insurable risks and thereby the responsibilities of Treasury. As will be explored, with further advances insurance is similar to hedging. This then comes down to matching the risk exposure with the transfer instrument, can this be matched appropriately?

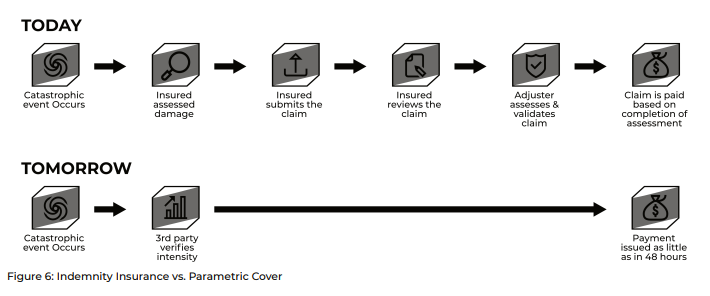

Parametric vs. Indemnity cover

Traditional insurance is well suited to high frequency, low severity events which is covered in the lower part (in terms of limits) of the corporate insurance program. A captive might be part of that area of risk as well, which has a higher degree of predictability. A multitude of small-scale losses are easier to model and manage due to the richness of historic data and the fact that the law of large numbers will enable accurate macro level predictions. Indemnity cover is based on carefully drafted wordings, and a loss has to be established before ultimately (which may take some time) a claim payment is made. The principle of parametric insurance intends to speed this process up to a great degree, as shown below.

This is not intended to declare the end of indemnity cover, this can still be highly efficient. But parametric insurance is increasingly important to complements this traditional approach to improve both the efficiency as well as effectiveness of cover.

Critical is the carefully constructed payout trigger. Traditionally this has been weather related like rainfall or windspeed at a certain weather station. This is increasingly tailor made with on-site weather stations preventing any mismatch in hitting a trigger (“basis risk”). Next to that other perils are increasingly possible, production downtime for instance can be objective measured. Lockdown measures also provide a clear objective trigger, and this is being discussed extensively. With increasing amounts of data and advanced data analytics minimizing a potential mismatch can be done objectively for a large range of perils. Basis Risk in that sense is the equivalent of retained risks in indemnity cover.

Enabling parametric cover does however mean that data should be available as well is a clearly defined model how trigger and potential loss relate. That means that (risk) data needs to be governed and managed, ensuring good quality data available to the treasurer. This may also imply that the treasury or insurance professional needs to tap into more data sources in order to model the trigger and exposure optimally.

Trading

Parametric insurance was initially developed in the form of catastrophe bonds to provide extra reinsurance capital for major disasters. Still very often this is based on large volume transactions. Global capital markets dwarf reinsurance markets in terms of capacity. The Aon Reinsurance report 2020 estimates the global pool of reinsurer capital is $532bn. This is tiny when compared to the global equity market of $75tr, a global bond market of $100tr and a global derivatives market with a notional principal value of $700tr. Insurance provides a very interesting type of risk which is not or limited correlated with traditional investment risks and provides a very interesting new asset class. Being able to transact in smaller volume, while remaining the good trigger-exposure link is a challenge, but this is being resolved with a Risk Trading platform like Ryskex.

Integration into Treasury Processes

An In-house Bank structure is common treasury terminology, the in-house insurance structure is that fors ome treasurers. A Risk Trading hub enables to integrate the best of both worlds and create a shared risk pooling vehicle enabling efficient and effective sharing of risks within the organisation.

A key feature in this approach is Treasury Technology. The Treasury Management Platform or the Trading platform which most (dedicated) treasuries use will inevitably play a key role in the infrastructure of the Risk Trading hub. They provide the centralised point of entry and point of control for trading. Via API or other connectivity the link to a Ryskex platform is possible and allows the treasurer to trade a ‘traditional’ insurance risk as easily as USD risk, hedging any risks that the treasurer isn’t willing to retain.

Conclusion

Whether it is possible to have a parametric trigger or a step further to trade risks is work-in-progress, but as corporate insurance manager, treasurer, captive manager it is critical that initial steps are already being taken. Are you in control of your risk data (which is broader than an historical claims overview)? Which data are you able to utilize and is the data quality being managed? The roadmap for a future proof treasury starts today.

Check my previous blogs of this serie:

- Alternative Risk Finance in a hardening insurance market

- Alternative Risk Finance Part 2 – Building the Business Case

- Alternative Risk Finance Part 3 – Cell Company

Risk and Compliance Specialist