Treasury ABC Part II

| 14-07-2016 | Jan Doosje |

For many people Treasury is, as they think, something that is not concerning. Because there are many items that could be mentioned and listed here, I chose to mention the items that have effect on our daily lives, even if we are not aware of the existence of the described item. Last week I started off with the first part of the treasury ABC which I’ll call the Treasury ABC for normal citizens.

F is for Floor

A floor is a technical term for an interest option. When buying a floor you are “ensured” to receive an interest rate at the level you pay for. Even if the actual interest is lower, you will be compensated for the difference.

G is for Gold Standard

A Gold standard is the monetary system where a currency unit is equal to a certain weight of gold. So, for every banknote the central bank has a stock in its bank safes. The system of the Gold Standard no longer exists.

H is for Hedge fund

A Hedge fund is a fund that has the purpose of lowering risk for a restricted group of investors by buying and selling shares. When the market as a whole goes down, a hedge fund tries to keep on the same level/rate as the hedge fund started with so the investors are “ensured” to get their investment back without a loss. Nowadays hedge funds are also sometimes speculating and can be confronted with big losses when the hedge fund manager doesn’t do his job right. Be sure of all risks and opportunities before you step into a hedge fund.

I is for Instrument

Not every instrument is made for the making of music. Looking in the perspective of treasury an instrument is used to achieve a goal from the investor e.g. lowering risk or optimize rentability. Treasury instruments can be divided for the following purposes:

- Interest risks

- Interest swaps

- Forward rate agreements

- Options

- Currency risks

- Options

- Currency swaps

- Forward contract

- Money market instrument

J is for Jumbo.

In 1972 the United States Department of the Treasury issued a Jumbo Bronze medeal Huge 8 ounces. This is the category of useful information.

Talking to our readers and contributors we have noticed that there are treasury related words with many different understandings. We’ve asked Jan Doosje to kick off a treasury ABC. Of course this is not binding and there are letters which can be connected to several treasury related words We need your input to make a complete treasury ABC. Would you like to contribute to the treasury ABC? Please contact our community manager Stephanie Derkse.

Owner of Fimterim Advies & Consultancy

An increasing number of bankers come to my recruitment desk wanting to make a transfer to corporate treasury. This transfer can be made successfully but there are a number of things to take into account. Below the 8 career hurdles, I hear most about, in a transfer from banking to corporate treasury.

An increasing number of bankers come to my recruitment desk wanting to make a transfer to corporate treasury. This transfer can be made successfully but there are a number of things to take into account. Below the 8 career hurdles, I hear most about, in a transfer from banking to corporate treasury.

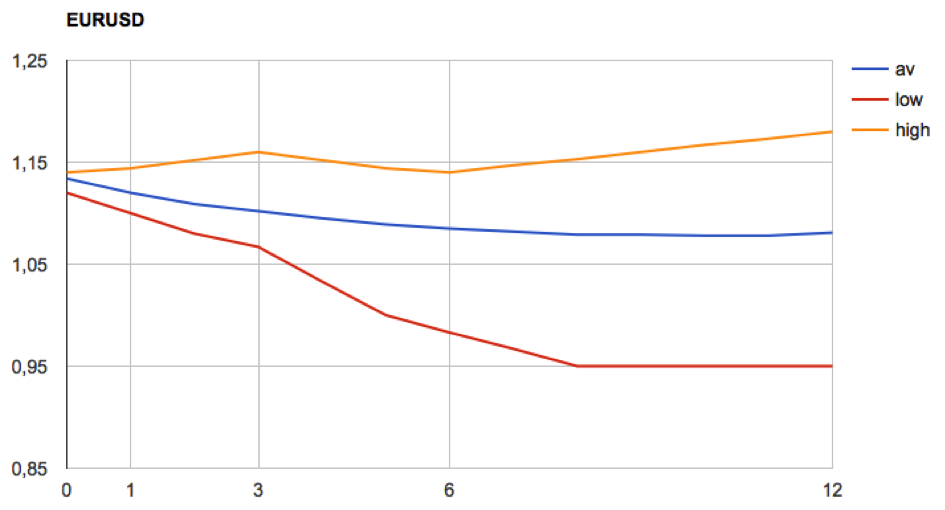

De afgelopen week zijn er grote verschillen gezien in de koers van de Britse pond na de uitslag van het referendum. In januari 2015 werd de markt ook al eens verrast door een onverwachte gebeurtenis: De Zwitserse Centrale Bank (SNB) veroorzaakte toen een schokgolf met het onverwacht loslaten van de ‘peg’ tussen de EUR en de CHF.

De afgelopen week zijn er grote verschillen gezien in de koers van de Britse pond na de uitslag van het referendum. In januari 2015 werd de markt ook al eens verrast door een onverwachte gebeurtenis: De Zwitserse Centrale Bank (SNB) veroorzaakte toen een schokgolf met het onverwacht loslaten van de ‘peg’ tussen de EUR en de CHF.  René Schilder – Co Owner at 2FX Treasury BV

René Schilder – Co Owner at 2FX Treasury BV Already over a decade the treasury community agrees that the modern treasurer does not act out of an ivory tower. Still, a lot of the treasury stories about funding, I hear in treasury recruitment, are about technical details. I learn in detail about USPP’s, interest hedging strategies and convertible bonds. Between these technical stories I notice other ones. I think they are inspiring and would like to share two of them.

Already over a decade the treasury community agrees that the modern treasurer does not act out of an ivory tower. Still, a lot of the treasury stories about funding, I hear in treasury recruitment, are about technical details. I learn in detail about USPP’s, interest hedging strategies and convertible bonds. Between these technical stories I notice other ones. I think they are inspiring and would like to share two of them. Op 26 mei jongstleden was ik uitgenodigd om de door

Op 26 mei jongstleden was ik uitgenodigd om de door

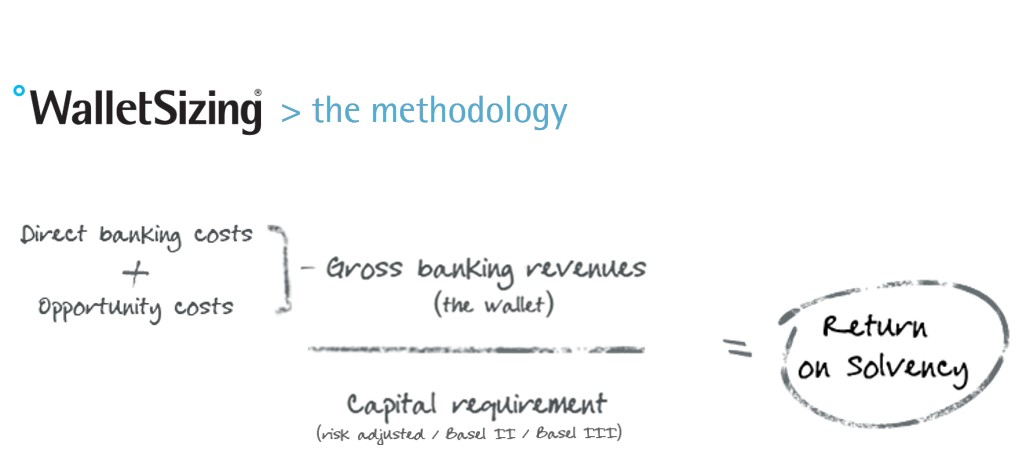

On april 13th of this year the Fintech innovation awards took place. Vallstein won the innovation award in treasury management with their Walletsizing® system. We asked Huub Wevers from Vallstein to give us an update on this new system. What’s new about it and who will benefit from using Walletsizing®?

On april 13th of this year the Fintech innovation awards took place. Vallstein won the innovation award in treasury management with their Walletsizing® system. We asked Huub Wevers from Vallstein to give us an update on this new system. What’s new about it and who will benefit from using Walletsizing®?

Huub Wevers is responsible for Corporate Solutions at Vallstein, the leading Bank Relationship Management specialist. Before joining Vallstein he has had eighteen years of experience in Banking at ABN AMRO and RBS, notably Transaction Banking. His responsibilities included Product Management, Account Management, Implementation and Operations, whereby his last role was the leadership of all Service & Operations in EMEA for RBS. At Vallstein Huub is responsible for building out the software solutions that Vallstein offers for corporates. Solutions that automate bank relationship management in order to assess the profitability that a corporate has for their banks, using all banking products and Basel III.

Huub Wevers is responsible for Corporate Solutions at Vallstein, the leading Bank Relationship Management specialist. Before joining Vallstein he has had eighteen years of experience in Banking at ABN AMRO and RBS, notably Transaction Banking. His responsibilities included Product Management, Account Management, Implementation and Operations, whereby his last role was the leadership of all Service & Operations in EMEA for RBS. At Vallstein Huub is responsible for building out the software solutions that Vallstein offers for corporates. Solutions that automate bank relationship management in order to assess the profitability that a corporate has for their banks, using all banking products and Basel III. Willem van Overveld beschrijft hoe een simpele SWAP constructie zonder margin calls toch lastig kan worden: de menselijk organisatorische kant van derivaten constructies krijgt vaak te weinig aandacht. Een voorbeeld uit de praktijk:

Willem van Overveld beschrijft hoe een simpele SWAP constructie zonder margin calls toch lastig kan worden: de menselijk organisatorische kant van derivaten constructies krijgt vaak te weinig aandacht. Een voorbeeld uit de praktijk: Willem van Overveld – Allround finance / treasury professional

Willem van Overveld – Allround finance / treasury professional Last week I visited an information session about financial postgraduate education. It was organized by the VU (Vrije Universiteit, Amsterdam). I noticed an increased interest in comparison to last years session, which is great. Information was provided about courses I see back in the CV’s of treasurers: CFA, RBA (Register Belegging Analyst) and of course RT (Register Treasurer) that has an overlap with the ACT courses. Education, specifically postgraduate, is a topic that returns in many of my meetings. This is what I notice on the topic:

Last week I visited an information session about financial postgraduate education. It was organized by the VU (Vrije Universiteit, Amsterdam). I noticed an increased interest in comparison to last years session, which is great. Information was provided about courses I see back in the CV’s of treasurers: CFA, RBA (Register Belegging Analyst) and of course RT (Register Treasurer) that has an overlap with the ACT courses. Education, specifically postgraduate, is a topic that returns in many of my meetings. This is what I notice on the topic: