25-11-2024 | The discussion explored various aspects of AI technology, including its potential benefits, real-world applications, and the impact on the job market within the finance and treasury sectors.

30-10-2024 | Join our webinar in partnership with Embat: AI-Powered Finance, The CFO’s and Treasurer’s Secret Weapon for Growth & Efficiency | Sign up for free

07-09-2023 | In a recent live session “Empowering Treasurers, Trade Finance Management Strategies,” industry experts provided valuable insights into the world of trade finance.

17-08-2023 | treasuryXL and Surecomp would like to invite you to join us for an exciting live session on the topic of: “Empowering Treasurers: Trade Finance Management Strategies”

Recently, we had a panel discussion about a few major treasury trends for 2023 together with Nomentia and experts Pieter de Kiewit, Patrick Kunz, Niki van Zanten, and Huub Wevers. If you didn’t get the chance to attend the webinar, you can find the recording here.

During this interactive live discussion we covered some of the following topics:

Market and FX Risk management in current times of uncertainty.

Top treasury technologies to consider for 2023. Will APIs deliver their promises?

Building the bridge between Ecommerce and treasury.

The rapidly changing role of treasury to facilitate business success

A friendly reminder that next week at 11 AM CET (November 17th), we’ll be collaborating with Nomentia.

Participate in our live panel discussion regarding 2023’s predicted treasury trends. We invited industry experts to join us and have an open debate about the issues that treasurers would need to think about in 2023. Additionally, there is the option to ask questions.

Date & Time: November 17, 2022, at 11 AM CET | Duration 45 minutes

Some of the topics we’ll cover:

Market and FX Risk management in current times of uncertainty.

Top treasury technologies to consider for 2023.

Will APIs deliver their promises?

Building the bridge between Ecommerce and treasury.

The rapidly changing role of treasury to facilitate business success

Pieter de Kiewit, Owner of Treasurer Search (Moderator) Patrick Kunz, Independent Treasury Expert (Panel member) Niki van Zanten, Independent Treasury Expert (Panel member)

Huub Wevers, Head of Sales at Nomentia (Panel member)

https://treasuryxl.com/wp-content/uploads/2022/11/webinar-treasury-trends-200-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-11-10 07:00:242022-11-09 14:04:28Only one week left! Live Panel Discussion: Treasury Trends for 2023

Join us on our live panel discussion about treasury trends for 2023. Together with Nomentia we invited industry experts who will have an open discussion on the things you need to consider as a treasurer in the year 2023. There’s the possibility to ask questions as well.

Some of the topics we’ll cover:

Market and FX Risk management in current times of uncertainty.

Top treasury technologies to consider for 2023.

Will APIs deliver their promises?

Building the bridge between Ecommerce and treasury.

The rapidly changing role of treasury to facilitate business success

Pieter de Kiewit, Owner of Treasurer Search (Moderator) Patrick Kunz, Independent Treasury Expert (Panel member) Niki van Zanten, Independent Treasury Expert (Panel member)

Huub Wevers, Head of Sales at Nomentia (Panel member)

https://treasuryxl.com/wp-content/uploads/2022/10/TT-2023.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-10-25 07:00:012023-03-07 15:50:04Live Panel Discussion: Treasury Trends for 2023

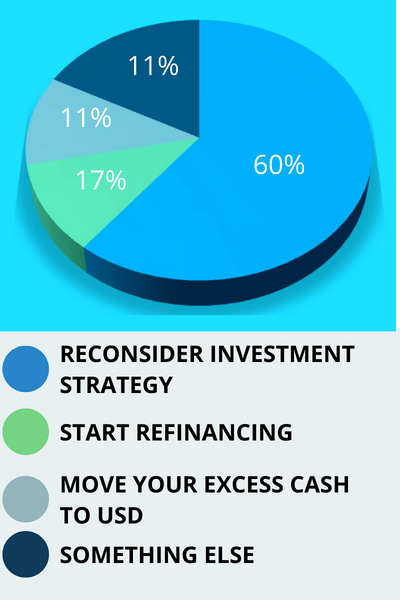

Welcome to the second edition of this newsletter where we discuss the latest treasuryXL poll on current issues in corporate treasury. We will take you through what treasurers think about a current topic by their votes, and a couple of treasury experts will explain their views on the subject. In this edition, we discuss what treasurers should do first to control against sharp increases in interest rates.

In last month’s poll, we discussed the impact of the recent interest rate increases on treasury. The poll received 35 votes, the results can be found in the image below.

We clearly notice that the majority of the treasurers are of the opinion that the first thing to do to control sharp interest increases is to reconsider the investment strategy of excess cash. We asked a number of treasury experts to explain why they voted for the other options than for a reconsideration of the investment strategy.

Niki voted for the option to move excess cash to USD.

“Place excess cash in USD requires a holistic approach, the right time and knowledge, but if applied correctly, will manage your cash like a pro”

Treasurers want to manage certain risks, and often there is a silo approach. Liquidity risk is managed with loans and deposits, Interest risk (and returns) are managed with products such as interest rate swaps and FX is managed with FX spot, forwards and swaps. Once the incoming data (think bank balances, forecasts, markets rates) is structured, the data becomes information and is sufficient to act as treasurer with clear objectives (these are often defined in the above silos).

The next step would be to validate whether the approach meets the objectives. So, far nothing to worry about….until the market exhibits unexpected behavior. For example, a disconnect between FX swap points and underlying interest rate differentials (Jan 2015 USDCHF as a reference), or perhaps a need to optimize interest rates. In this case (and when provided time and knowledge is available), a holistic approach to FX, interest rates and cash can provide the opportunity to place excess cash in a higher-yielding currency without adding FX risk to your portfolio.

In short, it may make sense to place excess cash in USD if it does not shift FX risk or if this shift is managed by FX swaps and the pricing between swaps and deposits is compared. Again, this requires a holistic approach, the right time and knowledge, but if applied correctly, will manage your cash like a pro.

Some considerations may be to look at the efficiency of FX swaps versus deposits, as FX swaps tend to be more efficient, automation of solutions, and tracking and identifying market behavior.

Jeremy voted for the option to choose something else.

“Analyze how your company is exposed to the economic cycle ”

First, analyze how your company is exposed to the economic cycle – a study I saw in the early 2000s showed that the best position for airlines was to be 100% floatig, because their business was effectively in lockstep with the business cycle.

In theory, when an entity is part of an industry that is closely aligned with the economic cycle, it has a natural hedge for its interest rate exposure, in that it can afford to pay higher interest rates when the economy is booming, and get some relief from lower interest rates when the economy is slowing. The study I’m referring to involved a major German airline; at the time, the airline’s funding was 80% fixed, and their comments at the time were not very favorable to switching to such a large floating exposure. Fast forward 15 years, or so, and I checked their Financials. They were 85% floating at the time, so they had clearly stepped into the results of the study.

The biggest risk for them would be an extended period of Stagflation, so I hope they do well in the current circumstances!

Vincenzo voted for the option to move excess cash to USD.

“My view here is that a treasurer should take a conservative approach”

Macro themes continue to drive financial markets. One does not have to look much further than the inverted US yield curve or the collapse in copper to understand that investors continue to re-price global growth prospects lower.

This is possibly because: (a) European activity is more exposed to the Russian energy supply shock and b) the U.S. economy has entered this global tightening cycle with more momentum and a positive output gap.

Inverted yield curves are typically bad news for pro-growth currencies (commodity exporters + Europe & Asia ex-Japan) and typically good news for the dollar, the Japanese yen, and the Swiss franc. This environment looks set to continue over the summer months as the Fed continues its tightening policy.

Recall that the German Bundesbank estimated that the Germany economy could take a 5% GDP hit if gas is rationed. It now appears that we are now not far from such a scenario. The pressure on European growth has caused the Eurostoxx benchmark equity index to fall 22% year-to-date, versus -20% for the S&P 500. The question will be how much more the ECB can tighten before the growth valves come down.

My view here is that a treasurer should take a conservative approach and assume that there are no large loans to be repaid to the banks, existing cash in excess should be moved to USD or to CHF or to JPY at least until the end of this year.

Sooner or later, Ukraine and Russia war will come to an end, so the cycle will reverse and EUR will become more attractive for investors and for treasurers.

https://treasuryxl.com/wp-content/uploads/2022/08/Kopie-van-linkedin-poll-recap-2.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-07-25 07:55:452022-12-20 10:08:03What should treasurers do first to control against increases in interest rates?

The straightforward answer is ‘No’. Unfortunately, saying ‘No’ does not imply that you don’t play a part in the global casino named: The FX market. It could be a sane procurement, sales or investment decision that brings you a seat at the table. Unless you are a in this market to make commissions or in some rare instances a (successful) prop trader, you will most likely lose more then you gain when willfully playing the game.

The FX market is by far the largest market in the world easily exceeding equity, bonds markets or any other asset class. Estimates in daily turnover are north of 6 Trillion USD. The vast majority of trades have a USD leg and EUR is coming at a good second place making EURUSD the most traded pair. Comparing this to the Global Domestic Product (GDP) of let’s say 140 Trillion USD as a ballpark figure, the FX market monthly turnover exceeds the world’s annual GDP. Taking into account that not all global GDP related transactions in the world have a FX component, this tells us that a large percentage of the FX are not real money flows.

So what are they? For a part these are institutional investors like pension funds. Pension funds can choose to allocate in different currencies, but the more likely explanation is that a large part of the FX transactions are of a more speculative nature. Hedge funds for instance do not have a functional or group currency and therefore can freely take currency decisions when allocating assets.

So in summary, the largest market place in the world is driven by forces which are extremely difficult to predict by any form of scientific research or even looking into economic data like monetary flows. Not to imply that economic indicators and central bank policy don’t have its influence, but in the end, a market is primarily driven by supply and demand and there is vast speculation in buying and selling of currencies.

Switching to the corporate point of view, companies usually don’t want to be a part of the FX market. It’s the same story as you might wish to procure and/or sell in different currencies than your own for a variety of reason. It’s an open door to mention that this can be very beneficial but all cost need to be factored correctly before taking a decision. With Foreign Exchange this can be a difficult task and considering what is mentioned above, the FX market does not actually make things look better.

A basic example of why it’s hard to get a grip on the currency markets is available when looking at CNH (offshore RMB) forward markets in 2015 and 2016. Although there are structural differences between CNH and CNY in both spot and outright forwards, typically the pricing is at comparable levels (for the majority of us, at least the large China interest does not apply this). Yearend brought a liquidity squeeze and the forward markets showed huge spikes in volatility as well as extreme differences between the CNH and CNY yield curves. There are many more stories like this to share and recently even G10 doesn’t seem excluded from Emerging Market (EM) like volatility, particularly when looking at Brexit and the Swiss Franc peg release of January 2015.

So a few basic assumptions can be helpful when participating in the FX market for real money requirements

• Don’t think you can predict or beat the market

• Price in risk

• Risk can go both ways but spreads are by definition a cost

• If you choose to hedge make sure you get your exposure right and hedge to mitigate this exposure (in other words don’t use derivatives which don’t offset the hedged item)

• Be aware there is a difference between advise on a financial product and actually risk mitigation on a more holistic basis

• It’s hard to beat years of market experience, don’t hesitate to reach out to seasoned professionals who will prevent you from making expensive mistakes

Hope this was a good read and for any questions or feedback please share and keep things interactive.

https://treasuryxl.com/wp-content/uploads/2020/09/Blog-Nikki-200-x-200.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2020-09-02 07:00:192022-12-28 13:59:09The global FX market, do you want to be a part of it?

Technology in treasury is advancing at full speed. AI, tokenization, real-time payments, APIs, stablecoins and new data models are changing how treasury teams operate — and the pace can feel overwhelming, especially in lean teams.

In this joint session together with Kyriba, we bring clarity.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.