The Top 5 Most Popular Articles of 2022 on treasuryXL!

02-01-2023 | treasuryXL | LinkedIn | Welcome to 2023! We are excited to present the Top 5 Most Popular Articles of the year on treasuryXL!

02-01-2023 | treasuryXL | LinkedIn | Welcome to 2023! We are excited to present the Top 5 Most Popular Articles of the year on treasuryXL!

| 07-12-2020 | Mark Roelands | treasuryXL

This series on alternative risk financing has been about alternatives to traditional insurance, which get are more important role in the current hard insurance environment. How to build the business case is explored in Part 2 and the alternative structure of Cell Companies is explained in Part 3. The last part of the 2020 series is about the future of alternative risk financing, risk trading and the role of treasury in insurance.

In a data driven era, with rapid advancing capabilities there may be more efficient manners to transfer or share risk, insight into risk scan be increased as well as the subsequent possibilities to retain or transfer. Although this is an outlook into the (not too distant) future, it is important to be aware of developments and get into the position to benefit from these developments preparing for 2021 and beyond, the hard market isn’t just a 2020 phenomenon.

Obviously, risk management is a critical part of Treasury processes. The scope of risks to be managed however within Treasury varies significantly between companies. Common risks in scope include operational risks within payment processes and financial risks like currency risk and interest rate risk. Insurable risks (like property damage and general liability) can be part of Treasury responsibilities, but can be part of legal or enterprise risk as well. Often this relates the the nature of the business as well as the size of the company. For instance, high liability type of businesses often have insurance within a legal function.

With advances in data as well as the analytics capabilities it is possible to expand the scope of insurable risks and thereby the responsibilities of Treasury. As will be explored, with further advances insurance is similar to hedging. This then comes down to matching the risk exposure with the transfer instrument, can this be matched appropriately?

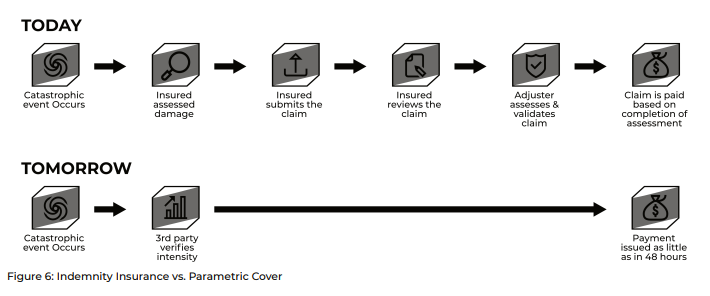

Traditional insurance is well suited to high frequency, low severity events which is covered in the lower part (in terms of limits) of the corporate insurance program. A captive might be part of that area of risk as well, which has a higher degree of predictability. A multitude of small-scale losses are easier to model and manage due to the richness of historic data and the fact that the law of large numbers will enable accurate macro level predictions. Indemnity cover is based on carefully drafted wordings, and a loss has to be established before ultimately (which may take some time) a claim payment is made. The principle of parametric insurance intends to speed this process up to a great degree, as shown below.

This is not intended to declare the end of indemnity cover, this can still be highly efficient. But parametric insurance is increasingly important to complements this traditional approach to improve both the efficiency as well as effectiveness of cover.

Critical is the carefully constructed payout trigger. Traditionally this has been weather related like rainfall or windspeed at a certain weather station. This is increasingly tailor made with on-site weather stations preventing any mismatch in hitting a trigger (“basis risk”). Next to that other perils are increasingly possible, production downtime for instance can be objective measured. Lockdown measures also provide a clear objective trigger, and this is being discussed extensively. With increasing amounts of data and advanced data analytics minimizing a potential mismatch can be done objectively for a large range of perils. Basis Risk in that sense is the equivalent of retained risks in indemnity cover.

Enabling parametric cover does however mean that data should be available as well is a clearly defined model how trigger and potential loss relate. That means that (risk) data needs to be governed and managed, ensuring good quality data available to the treasurer. This may also imply that the treasury or insurance professional needs to tap into more data sources in order to model the trigger and exposure optimally.

Parametric insurance was initially developed in the form of catastrophe bonds to provide extra reinsurance capital for major disasters. Still very often this is based on large volume transactions. Global capital markets dwarf reinsurance markets in terms of capacity. The Aon Reinsurance report 2020 estimates the global pool of reinsurer capital is $532bn. This is tiny when compared to the global equity market of $75tr, a global bond market of $100tr and a global derivatives market with a notional principal value of $700tr. Insurance provides a very interesting type of risk which is not or limited correlated with traditional investment risks and provides a very interesting new asset class. Being able to transact in smaller volume, while remaining the good trigger-exposure link is a challenge, but this is being resolved with a Risk Trading platform like Ryskex.

An In-house Bank structure is common treasury terminology, the in-house insurance structure is that fors ome treasurers. A Risk Trading hub enables to integrate the best of both worlds and create a shared risk pooling vehicle enabling efficient and effective sharing of risks within the organisation.

A key feature in this approach is Treasury Technology. The Treasury Management Platform or the Trading platform which most (dedicated) treasuries use will inevitably play a key role in the infrastructure of the Risk Trading hub. They provide the centralised point of entry and point of control for trading. Via API or other connectivity the link to a Ryskex platform is possible and allows the treasurer to trade a ‘traditional’ insurance risk as easily as USD risk, hedging any risks that the treasurer isn’t willing to retain.

Whether it is possible to have a parametric trigger or a step further to trade risks is work-in-progress, but as corporate insurance manager, treasurer, captive manager it is critical that initial steps are already being taken. Are you in control of your risk data (which is broader than an historical claims overview)? Which data are you able to utilize and is the data quality being managed? The roadmap for a future proof treasury starts today.

Risk and Compliance Specialist

| 02-11-2020 | Mark Roelands | treasuryXL

As described in this series: an in-house insurer can be of great added value to your company. In the current hard insurance market, the possibility to utilize an own vehicle instead of the turbulent market is a direct and tangible benefit. But it is not a free alternative, the cost of setup of an insurer and operating it in a compliant manner might be too high to generate an overall positive business case. That issue is being addressed in utilising a centralised facility taking care of a.o. most of capitalisation and compliance matters, while the risk taker can operate an in-house insurer. This light-weight route is what can be named a “Cell Company”.

A Protected Cell Company, Incorporated Cell Company, Segregated Accounts Company, Segregated Portfolio Company are all different names for a centralised facility each buidling on local legislation, which we will collectively name “Cell Companies”.

In this part of the series of Alternative Risk Financing the generalised concept of a Cell Company is described.

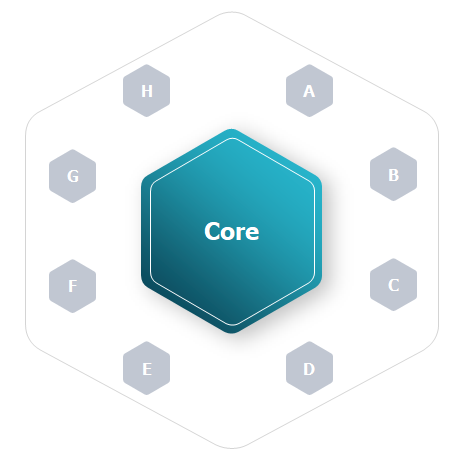

Where a fully-owned captive insurance entity imposes the full requirements on the parent company, the Cell Company utilises a centralised facility, a “Core”, which provides the infrastructure to be leveraged by multiple insurance entities. In the illustration the full hexagon is the Cell Company, with the Core representing the infrastructure.

The Small grey hexagons represent the Cells, which are segregated units within the facility and which belong to a specific client. Assets and Liabilities and legally segregated from other Cells and the Core. Cell A will for instance belong to Company A, while Cell B belongs to Company B. In most Cell Company structures the number of cells is not limited to 8 but is practically unlimited. In order to generate the segregation a split is made between Cellular Assets and Cellular Liabilies (the A-H hexagons) and non-cellular assets and liabilities (The Core).

Owning Cell A will enable a client to participate in an insurance program in a compliant manner, while building on the centralised facility which provides both a compliant governance structure, as well as the required capital amount.

As an individual client a key requirement however is to fund the ‘risk gap’, any open underwriting exposure being retained by the Cell needs to be collateralised somehow. Either via a guarantee. Letter of Credit, Capital or perhaps reinsuring more of the cover. This also ensures that each cell is able to sustain itself.

Leveraging on the infrastructure of another company, which also facilitates other companies raises the obvious question: is it safe? Are my funds secure, and can I be held liable for the liabilities of other companies?In short: Yes it is safe … but …it builds on carefully drafted agreements, hence careful due diligence is required.

Basically, it comes down to default legislation of the domicile involved. In the Netherlands for instance there is no separate legal form of a Cell Company, and legal segregation critical fort he structure cannot be achieved. In Malta the for instance the “Cell Companies Act” recognizes the type of entity and segregation involved. A recent Montana case also recognized the structure including legal segregation.

As mentioned several times, in order to make use of a Cell Company, legislation needs to be in place recognizing this particular form of a captive. Domiciliation is one of the the key considerations when an alternative risk finance structure is considered, as has been explain in Part 1 and Part 2 of this series.

In the Netherlands the required legislation for a Cell Company is not available. Within Europe therefore either Malta, Guernsey, Isle of Man or Gibraltar needs to be utilised. With Malta having the edge being within the EU. Ireland and Luxemburg have hinted on establishing Cell Company legislation as well, but Brexit (and moving insurance companies into these domiciles) has shifted supervisory priorities and no information has been published on any plans for a few years now. While Vermont is often the go to domicile within the US, there are more States with Cell Company legislation like Montana. Establishing a Cell Company close to an office of your company could be regarded to be beneficial. Vermont however does have an extensive captive servicing industry which is also a benefit.

Within Asia Vanuatu or Labuan would be interesting domiciles and the popular captive domiciles of Bermuda and Cayman Islands also both enable Cell Companies, and both have a solid supporting industry. This however needs to pass tax requirements in the organisation.

In Part 1 and Part 2 Captive Insurance and Building the Business Case is described. A Cell Company can possibly allow a business case to be positive, as the cost of operating and capitalising the Company is much lower then a fully-owned Solvency II compliant Insurance company. For building the business case please review Part 2, but when considering a Cell Company also take the following into consideration:

This may unlock the potential for an in-house insurer allowing you to pool your risks centrally and finance them in the most efficient manner, while operating in the most light weight manner.

Risk and Compliance Specialist

| 09-09-2020 | Mark Roelands | treasuryXL

In this 4-Part series on Alternative Risk Financing, our Expert Mark Roelands highlights upon the importance of Alternative Risk Financing.

Part I reflected the alternatives of risk financing in the current hard insurance market. Now, Part 2 reflects upon the business case and how to build it, in order to enable decision making and finally decide whether to pursue the alternative risk financing route.

Building internal support is critical in getting to the go / no – go decision. Defining the Business Case will go hand in hand with generating internal buy-in by involving internal stakeholders like tax and legal during the analysis process. This blog will be about the business case set up, and how the relevant stakeholders should be involved during the process. The business case setup then is managed together with a companies’ internal dynamic. Let’s find out how to build the business case with the relevant components……..

As introduced in Part I, a structured framework is required in order to get to structured decision making. The framework used is the Risk Financing Framework by Roelands GRC Consulting. The main question on whether to start an in-house insurer is divided in 4 sub questions with 4 modules

What is your strategy with respect to retaining risks? What risks are you willing to retain?

As a treasury department for instance, the currency exposures are managed and hedged. To a certain degree, hedging is either too costly or priced into forwards (with limited risk transfer implications). This also applies to insurable risk. A certain level of claims can be expected which will either be within the deductible level or priced into premiums. Critical is to understand what volatility is acceptable to the organisation. Stakeholder expectations and requirements can be key determinants. What headroom is available on financing arrangements and on what percentage deviations will supervisors and auditors start to raise questions? What quarterly earnings deviation would be possible, and has Covid19 changed that position? Bottom line, in most alternative risk financing structures the corporate retention is increased, and a crucial question therefore is when a negative scenario unfolds are you able to defend the impact of the insurable risk retention?

What is the ultimate objective to be achieved?

How would an in-house insurer fit within your organisation? This is about aligning internally on the conditions that need to be met for an in-house insurer. There are several countries or domiciles, and several forms of captive insurance which are possible. Within the organisation risk management resources and governance structures need to be aligned. Hence,

What form of captive would match your organisation best?

The trend in domiciliation, which is strengthened by BEPS, is offshoring or onshoring and to choose a domicile where there is substance. A treasury centre domicile would be a good alternative, as is the HQ domicile or certain domiciles which have a big captive insurance support industry. Within Europe, this would be Ireland, Luxemburg, Guernsey or Malta. Going outside of the HQ domicile may have some obvious tax consequences that will need to be addressed with the colleagues from tax. A Cell Company could be an interesting alternative, but it is important that this is understood correctly within the organisation (more on this in Part 3 of this series). The Legal department will need to be involved, and as this will have domiciliation implications, the Tax department as well. As a larger part of risk is retained within the company, it is critical that risk management processes are directed to managing the risk, and certain functions may need to be involved as well. For instance when employee benefits is a risk to be underwritten, then HR will definitely be involved as coverage provided is key.

Depending on the type of captive that is established and in what domicile certain governance structures may need to be established (for instance in the Netherlands, the Corporate Governance Codes applied as a captive is an NV, implying 2 independent members of the Supervisory Board), service providers need to be found and external resources may need to be purchased. These will often become partners which the company will be working with for multiple years, so how will they be selected? Brokers and insurers offer their captive or alternative risk finance facilities, which may be very good, but there is a certain lock-in aspect to it.

Therefore, decisions need to be considered carefully.

Relevant processes need to be established or adjusted to fit the new situation. From an operational point of view, adjustments will need to be made to ensure effective and efficient operations.

Sub question for the third part: How to align processes operationally, and to highlight relevant action points which will need to be addressed once a go-decision is made.

Deciding on whether or not to start an in-house insurer requires a well worked out quantified business case, based upon different scenarios in order to judge the risk appropriately. In order to generate a fair comparison, a total cost overview will need to be made. This compares the total costs, which will be paid externally i.e intercompany flows like premium to the inhouse insurer will thereby be excluded. Sub question of part four is whether the business case makes sense from a financial perspective. Which costs are in scope will be determined by the analysis resulting from the previous 3 steps. The simplified example business case below describes an imaginative Netherlands based captive insurance company. Although figures are purely indicative, the size of the amounts is representative of a captive business case.

Example Financial Business Case |

|||

| x 1.000 | Continuation – Expected | Captive – Expected | Captive – Negative |

| Total External Insurance Premium | 10.000 | 7.500 | 7.500 |

| Total Losses Retained | |||

| Below deductibles | 1.000 | 1.000 | 1.000 |

| Above (sub) limits | 0 | 0 | 0 |

| Excluded cover | 0 | 0 | 0 |

| Within in-house insurer | 0 | 750 | 5.000 |

| Operational costs | |||

| Insurance Premium Tax | 2.100 | 2.100 | 2.100 |

| In-house insurer costs | 0 | 350 | 350 |

| Insurance function costs | 200 | 250 | 250 |

| Risk Management costs | 15 | 15 | 15 |

| Total Costs | 13.315 | 11.965 | 16.215 |

| Change | – | 1.350 | -2.900 |

| Capital Required | – | 3.800 | 3.800 |

Premium observations

Losses retained observations

Cost observations

Overall observation

Bottom line, in the expected scenario here a positive result is projected, but when an incident occurs a negative result (compared to traditional insurance) is projected. This is a very common trade-off requiring a deliberate choice.

Deciding to start captive insurance is a structural decision (and forms a multiyear commitment) requiring a structured approach, it may help to involve external expertise from a broker, insurer, actuaries, or independent consultants as each business case is specific. The overview in this blog however does describe the main steps and considerations to be taken. When this business case is carefully set up, assumptions clearly described and financial projections are well worked out, this then already provides a solid basis for applying for an insurance license. The initial effort will pay-off at the end, so do not rush the decision making process

This is Part 2 of the Alternative Risk Finance Series, Part 3 will be “Cell Companies 101” and Part 4 will be “Risk Trading and Future Alternative Risk Finance”. Together this generates an overview of the current and future landscape of alternative risk financing.

Risk and Compliance Specialist

| 30-06-2020 | Mark Roelands | treasuryXL

Insurance premium rates are reported to increase on average with about 2% in Europe, confirming the overall market trend of a hardening insurance market. Some markets have, however, seen double-digit growth in premiums, like D&O and Motor Third Party Liability. Other markets witnessed important coverage elements actually being excluded from cover, making the premium comparison apples and pears. As Covid-19 is impacting claims experience across all lines as well as causing negative investment returns, the hardening insurance market trend is expected to continue and get worse in 2020. Premium increases are to be expected and retention levels are expected to be increased.

It is therefore critical to work with your insurance broker in time to understand and mitigate effects for the treasury and insurance function. What is the action plan when retentions are being driven upwards or when cover is disappearing? What alternatives are available next to traditional insurance? Will your organisation be forced to retain risk above the risk appetite or accept double digit premium increases?

Although retaining additional risk may not be the worst solution, as premium increases may not reflect the actual risk that is being transferred and there are awareness benefits to being exposed to risks, the possibility to transfer alternatively is very valuable in the current hardening market.

A captive is an in-house insurer, enabling efficient and centralized risk pooling while providing cover to operating companies and thereby bridging the gap between corporate and local risk appetite. Key arguments for establishing a captive are to smooth the impact of hardening insurance markets as well as provide additional flexibility in cover. The current market environment is therefore a textbook example for establishing an insurance entity. However, a captive is a licensed insurance company that comes with added costs and a compliance burden. This is especially true since Solvency II became active in 2016. As a general rule of thumb a minimum threshold of captive premium of EUR 2Mio would be required for a Dutch based captive, allowing for claims expenses (70-80% claims ratio), operating costs as well as building some reserves. Establishing a captive in other jurisdictions can make sense, as the route to licensing might still be feasible in 2020 (for the Netherlands at least 6 months are to be expected) as well as the opportunity of some more light-weight operational structures.

An interesting alternative to the fully owned, traditional captive is a Cell Company; either an Incorporated Cell Company (ICC) or Protected Cell Company (PCC). These alternatives provide the benefit of a shared structure (including initial capitalisation) and enable a ring-fenced environment for your organisation. In order to arrange that ring-fencing, specific legislation is required, which is found in Malta in the EU. Guernsey (leaving tax considerations aside) might be very interesting as well. Ireland and Luxemburg did give some hints for establishing cell company legislation but after Brexit this was delayed indefinitely. A Cell Company can provide the same functionality as a fully owned captive, but treasury and insurance will have to work with legal and tax to get a solid business case in place in order to address questions proactively.

Both Aon-Willis and Marsh have Cell Companies and would be able to assist, but insurers can also facilitate this (which has a lock-in effect) while there are also more independent providers like Artex, SRS (completing the top 5 of largest captive managers 2020) and firms like Atlas or Robus which can potentially be of added value as well.

Next to captive insurance, parametric insurance is a promising route to follow.

Parametric insurance has historically been connected to weather insurance (e.g. rainfall exceeding a threshold leading to a pay-out) as well as longevity cover for pension funds (in the form of Insurance Linked Securities, Longevity Swaps). Parametric products enable a highly transparent and quick risk transfer and enable the route to other markets than the insurance market. A parametric product can be structured in an insurance structure but in a derivative structure as well. Conceptually an insurance-linked derivative will not be different than the plain vanilla currency instruments that are traded.

Covid is also attracting significant attention for parametric cover, as lockdown measures can be clear-cut triggers for parametric cover. Most importantly, for parametric cover clear risk information and data analysis is required and both are increasingly available. Increasingly better data and analysis techniques enable to minimise basis risk i.e. the risk in which an incident occurs but the derivative trigger is not being met. For instance site-specific weather stations are set up to ensure rainfall or water level at your organisations’ sites are being monitored. Increasingly, non-weather risks are being covered, for instance Ryskex GmbH and Axis Capital have worked together to develop parametric cyber-insurance cover.

Where traditional insurance has deductibles and exclusions, parametric risk transfer has basis risk which needs to be managed. Next to that other operational processes may be impacted, claims management for instance and therefore it is recommended to make a well founded and analysed decision.

Starting financing risks in a different manner is not a decision to be made in isolation and to be done quickly. It is a structural decision requiring a structured approach. In our practice, we use our Risk Finance Framework which is composed of (1) Foundation, the objectives to be met (2) People & Organisation, matching the organisation, policies and people involved (3) Processes, adaptive, effective and efficient (4) Data and Technology, the business case based on solid risk information.

In our view, this provides a very practical and structured approach allowing stakeholders like tax and legal to be involved throughout the process. Back planning from a January renewal date, it is critical that conversations with your broker and insurers are taking place in order to ensure no last-minute surprises are presented as a treasury or Insurance professional. In parallel, the (internal) business case can be analysed in order to make a decision.

Therefore, it is recommended to start preparations early, or actually on an asap basis.

Alternative Risk Financing can be highly interesting, but it is not an instant go-to solution and requires some preparations.

Risk and Compliance Specialist

Join treasuryXL as a partner!

The treasuryXL Partner Program is designed for organizations offering products or services in treasury, cash and risk management.

Newsletter & eBook

Subscribe to our free weekly newsletter and receive your 41 pages ‘easy-to-read’ eBook, What is Treasury?