| 19-12-2017 | Lionel Pavey |

On 29th November treasuryXL attended a seminar organized by Fitch Ratings in Utrecht. It was a presentation by Fitch that explained the approach they had taken to determine credit ratings for 2 different entities within the Dutch healthcare industry: Stichting Elisabeth-Tweesteden Ziekenhuis in Tilburg – a hospital, and Stichting GGZ Noord-Holland Noord – a mental healthcare institute. There was a fair amount of interest in this seminar as more than 35 people attended, representing banks, financial advisors, healthcare industry and insurance companies.

Whilst both entities are in the healthcare industry there are distinct differences in focus and size: Elisabeth-Tweesteden caters to the surrounding area and had 632,000 hospital visits in 2016 and 4,000 FTEs, GGZ has 10,000 patients and 1,240 FTEs.

What is a credit rating?

A credit rating agency (Fitch) attaches a credit rating to an entity (debtor). A rating is an opinion as to the entity’s ability to meet financial commitments on a timely basis. It measures the ability of the debtor to repay principal and interest of loans on time and in full, together with the probability of default. To be able to come to a conclusion for the rating, the entity needs to supply all relevant information to the rating agency, which can then perform the necessary analysis to judge their creditworthiness.

Applying the criteria

Fitch uses two criteria to rate healthcare entities: the recently updated Government Related Entities Rating Criteria (currently published as an exposure draft) and the Revenue Supported Debt Rating Criteria. The first determines the likelihood of exceptional support in the case of financial difficulties at the Government related entity. The latter determines the Standalone Credit Profile.

An entity is defined as being government related if they are semi-publicly owned/controlled by the government and/or local authority has majority economic or voting control over the entity. Fitch assesses whether a government is likely to support an entity in financial distress to avoid negative socio-political repercussions of a default, or if the entity fulfills an important public policy mission. The Government Related Entity Criteria covers four key factors:

- Status and control

- Support track record and expectations

- Socio-political implications of default

- Financial implications of default

In order to determine the Stand-alone credit profile the Revenue Supported Debt Criteria is used that covers revenue defensibility, operating risks and financial profile. Fitch concluded that both entities were able to receive a long-term credit rating of single A.

For investment grading criteria, Fitch applies a highest rating of AAA and a lowest rating of BBB-. A single A rating is a high credit quality. ‘A’ ratings denote expectations of low default risk. The capacity for payment of financial commitments is considered strong. This capacity may, nevertheless, be more vulnerable to adverse business or economic conditions than is the case for higher ratings.

What are the advantages of a credit rating?

- Enhances access to capital markets

- Facilitates risk pricing for funding

- Improves bargaining power with banks and suppliers

- Recognition amongst peers and in international capital markets

- Rating process provides improved transparency and financial discipline for the rated entity

- Annual Rating report may be used as a standalone marketing instrument

What are the implications in the Netherlands?

At present, the Dutch government has majority control in many companies including transport – NS; infrastructure – Prorail, Schiphol; energy – Gasunie, Tennet; and financial services – BNG (Fitch rated AA+, Stable, FMO (Fitch rated AAA/Stable). Furthermore local authorities also have majority control in local companies including transport – GVB, HTM, RET, energy – Eneco, and household waste – AEB, HVC. All the companies require funding, the majority of which is covered with either a national or local government guarantee, or direct participation. Fitch rates all types of government related entities, and with a rating it may be possible for these entities to further their scope for acquiring finance.

An important question that arises is: should national and local government restrict themselves to issuing guarantees and allowing the free market to determine the funding, or should they proactively engage in lending money to companies? Only if more entities were in the possession of a credit rating, could a clear decision be taken. At a time of low interest rates and a shortage of “prime” graded loans, it could possibly be advantageous if the loan market could be opened to more lenders – secure in the knowledge that the loans were guaranteed.

If you are interested in learning more, please contact us via email at [email protected]

Lionel Pavey

Lionel Pavey

Cash Management and Treasury Specialist

Over the last year there have been impressive price gains in Greek Government bonds leading to equally impressive falls in yields. Greek 2-year bonds are now yielding 1.35% – down from around 7% at the start of 2017. Similarly, 10-year bonds are now yielding 3.66% – a significant fall since the start of 2017. In fact, the yield on Greek 2-year bonds is now lower than in USA where the current yield is 2.09%. Last week S&P upgraded Greece’s long term credit rating to ‘B’ from ‘B-‘. It would appear that Greece is doing everything right. Right?

Over the last year there have been impressive price gains in Greek Government bonds leading to equally impressive falls in yields. Greek 2-year bonds are now yielding 1.35% – down from around 7% at the start of 2017. Similarly, 10-year bonds are now yielding 3.66% – a significant fall since the start of 2017. In fact, the yield on Greek 2-year bonds is now lower than in USA where the current yield is 2.09%. Last week S&P upgraded Greece’s long term credit rating to ‘B’ from ‘B-‘. It would appear that Greece is doing everything right. Right?

Despite interest rate being very low for the last few years, general consensus is that rates will eventually rise – rates will become more normal. Rates are being held down by the actions of central banks with their quantitative easing. As QE is scaled backed and stopped this should allow rates to rise from their current low levels. The big question is – how high will rates rise? The Euro is not yet 20 years old and that means that whilst there is a lot of data, it does not require looking through 50 or 60 years of data to try and find the norm.

Despite interest rate being very low for the last few years, general consensus is that rates will eventually rise – rates will become more normal. Rates are being held down by the actions of central banks with their quantitative easing. As QE is scaled backed and stopped this should allow rates to rise from their current low levels. The big question is – how high will rates rise? The Euro is not yet 20 years old and that means that whilst there is a lot of data, it does not require looking through 50 or 60 years of data to try and find the norm.

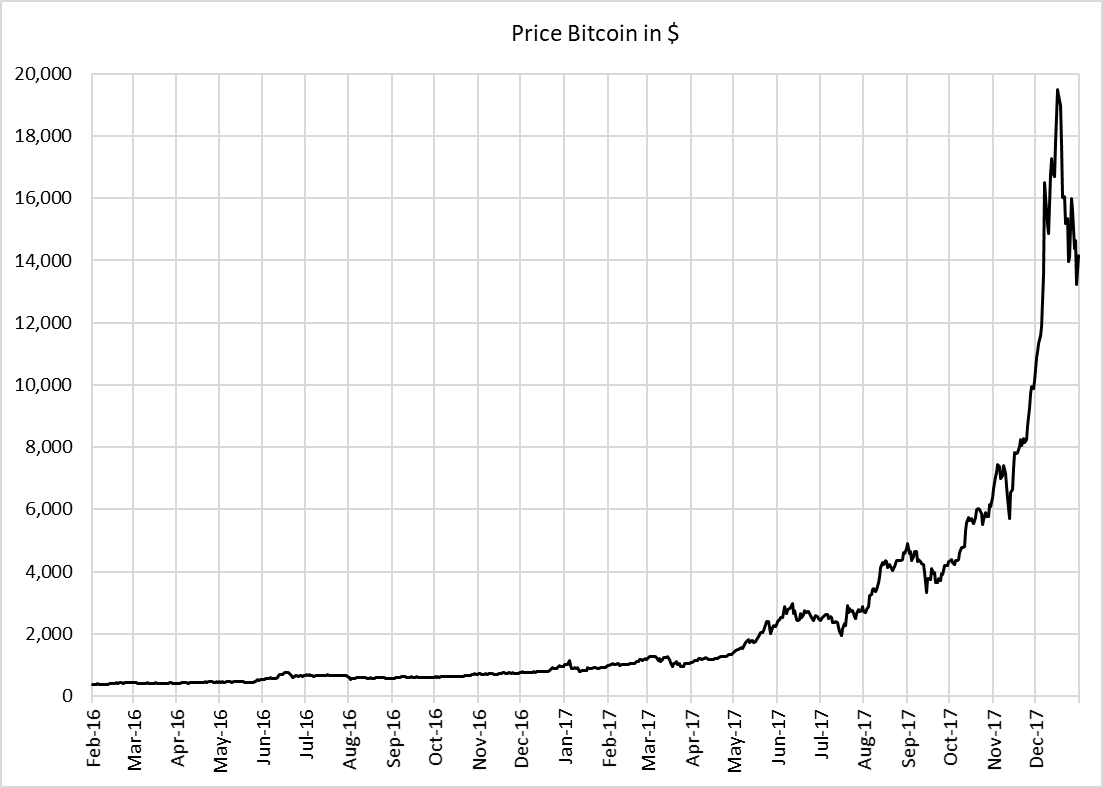

Having spent my working life in international finance, I have patiently listened to all the news about the Bitcoin over the last few years. During 2017 whilst the Bitcoin was on a spectacular price rise, my interest was awakened in this new phenomenon – is this the future? I attended seminars, read articles, learnt the difference between the Bitcoin and the Blockchain, searched and investigated via the web, and tried to form an opinion. These are my findings:

Having spent my working life in international finance, I have patiently listened to all the news about the Bitcoin over the last few years. During 2017 whilst the Bitcoin was on a spectacular price rise, my interest was awakened in this new phenomenon – is this the future? I attended seminars, read articles, learnt the difference between the Bitcoin and the Blockchain, searched and investigated via the web, and tried to form an opinion. These are my findings: Such a stellar performance should mean that the trade volume has increased dramatically.

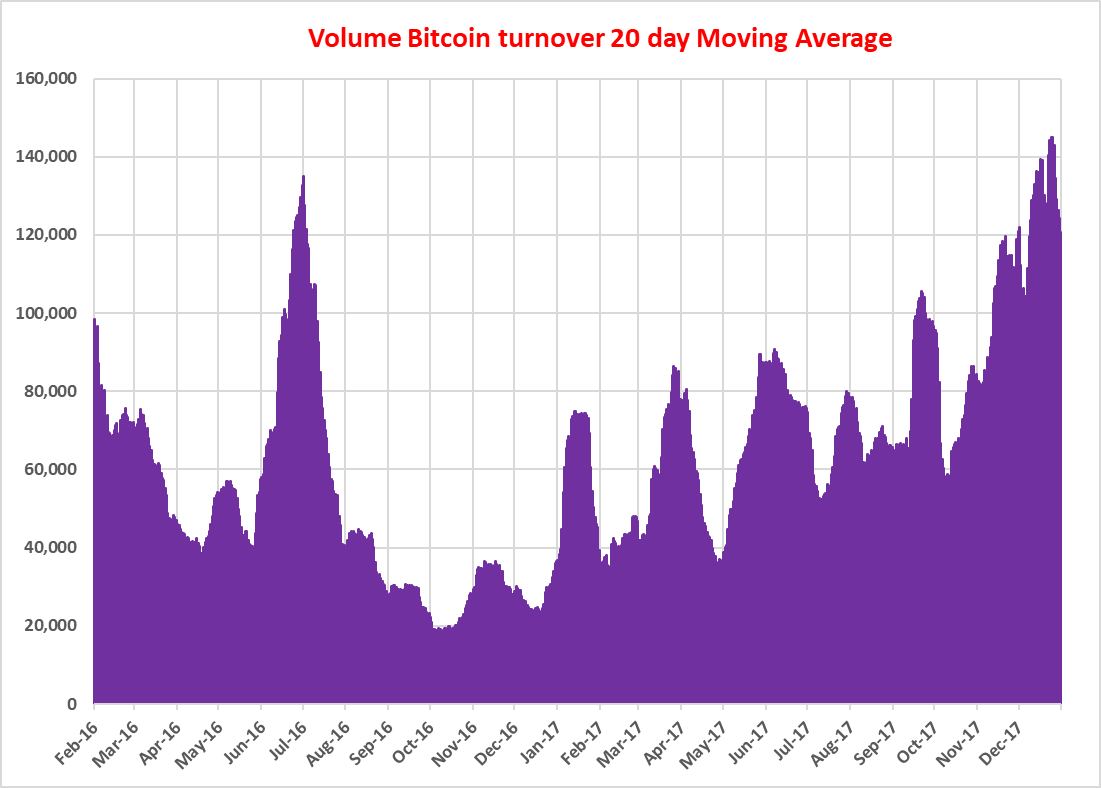

Such a stellar performance should mean that the trade volume has increased dramatically. The daily volume in September 2017 when the price was about $4,000 was the same as the start of February 2016 when the price was about $400. I had to create this chart as all the data I could find related to the $ value of turnover – which was phenomenal – and not the actual number of Bitcoins traded. Normally, when an asset sees a huge increase in price, this goes together with a corresponding increase in turnover. Clearly this has not happened with Bitcoin – why?

The daily volume in September 2017 when the price was about $4,000 was the same as the start of February 2016 when the price was about $400. I had to create this chart as all the data I could find related to the $ value of turnover – which was phenomenal – and not the actual number of Bitcoins traded. Normally, when an asset sees a huge increase in price, this goes together with a corresponding increase in turnover. Clearly this has not happened with Bitcoin – why?

PSD2 (Payment Services Directive) is an extension on the existing PSD within the EU. The objective is to increase competition in the payments industry, whilst increasing access from non-bank firms. This should lead to standard payment formats, infrastructure and technical standards – at first glance an improvement for consumers. However, there appears to be a particular threat to privacy and the threat of third parties gaining excessive access to personal data.

PSD2 (Payment Services Directive) is an extension on the existing PSD within the EU. The objective is to increase competition in the payments industry, whilst increasing access from non-bank firms. This should lead to standard payment formats, infrastructure and technical standards – at first glance an improvement for consumers. However, there appears to be a particular threat to privacy and the threat of third parties gaining excessive access to personal data.