Meet our Expert | 8 questions for Patrick Kunz, the Passionate Treasurer

01-03-2022 | Patrick Kunz | treasuryXL | LinkedIn |

We are happy to interview treasuryXL expert, Patrick Kunz.

With Patrick’s impressive career within the World of Treasury, you can really say that he lives and breathes Treasury.

Patrick is performance driven. He is an open minded, outgoing, rational person who is comfortable communicating and convincing on all levels of management.

Patrick is owner of Pecunia Treasury & Finance with several independent treasury and finance consultants and founder of treasuryabonnement.nl. Furthermore he owns an online FX trading and payment platform with a connection to a big FX broker.

Patrick has worked with both international corporates from all fields of business as well as national non-profit organisations.

We recommend to visit Patrick’s LinkedIn profile to see his stunning career and activities. But first….

We asked him 8 questions, let’s go!

INTERVIEW

1. How did your treasury journey start?

During my study at Maastricht University I knew I wanted to work in the “world of finance” and more specifically trading or investment banking. In my 3rd year of university I got the opportunity to work as an intern for a Swiss Investment bank in Zurich which was a great first experience into wealth management and client exposure with high net worth clients. It also showed me that the client comes first, even though the client was not always right. This made me wonder if it was more fun on “the other side” at the buy side. It slightly frustrated me that a bank would not always provide the best solution.

After graduation I left on a trip around the world backpacking for 1,5 years. Enjoying ultimate freedom and fun before starting a career. When I came back to the Netherlands I applied for treasury roles at multinationals and landed my first job as cash & treasury manager at the German multinational Metro Group (the wholesaler, not the Dutch free newspaper). This was the start of my treasury career which until now I would never leave.

2. What do you like about working in Treasury?

It’s the core of a company. In the end its all about the money. Independent on what products you are selling and how you are selling them. Cash in vs Cash out. Without cash a company has a problem. Cash is king and profit is an opinion so in my opinion managing cash is very important and therefore fun. The more complex the more fun. Managing a multinational company with hundreds of bank accounts in different currencies around the global; finding the optimal treasury setup and solutions is great fun. Lastly, treasury teams are smaller compared to accounting or controlling, which make the lines shorter and the team tighter.

3. What is your Treasury Expertise and what expertise gives you a boost of energy?

I started in cash management and FX trading which are great basic skills for every treasurer. My first company also had very short treasury lines and I quickly was involved in global treasury solutions, financing solutions and group companies corporate finance. When I moved on to my second role as group treasurer of a regional housing association, I also got exposure to interest rate derivatives and guarantee management. Afterwards when I started my own consultancy and interim management company 8 years ago I got to do the full spectrum of treasury. So without arrogance I can say in treasury I have done it all. The last years I am doing a lot of TMS/Payment hub implementations, which I enjoy doing. After finishing an implementation it is nice to look back and compare the old way of treasury processes and the new and see how it improved after a couple of months. Very rewarding.

4. What has been your best experience in your treasury career until today?

Building a treasury from scratch is most rewarding and fun to do. 2 years ago I got the opportunity to build the treasury role at the Dutch born AEX company Takeaway.com. There were treasury processes in place but scattered in different departments. Also some of them were sub-optimal. My role was to bring them together and optimize them. Besides increasing the reporting and importance of treasury to management this also brought significant cash savings on bank and FX costs. A couple of months into the rule, the merger/acquisition of Just Eat was approved and the integration with the existing treasury team in London could start, making the team suddenly 400% bigger. After 5 months my work was far from finished but it was time to hand it over to the existing/new team. Looking back what was done in this short time this was one of my greatest experiences in treasury. And a great company to work for.

5. What has been your biggest challenge in treasury?

Nowadays: Opening a company bank account in a short timeframe without difficult KYC questions, especially for companies with difficult or complex structures. I was with a client last year, a scale-up, that moved fast in several countries in Europe. Treasury processes needed to be implemented from scratch in each country while operations was much further ahead but legal and treasury still needed to start. Working with this fixed go live we had to make sure we could receive payments from day 1 onward. In one country we were actually live on day -1 with no room for error. Stressful but successful.

As a consultant I sometimes face tight deadlines or difficult projects that need to be delivered but are dependent on other stakeholders. That is not always easy but this gives me energy to make it happen.

6. What’s the most important lesson that you’ve learned as a treasurer?

You can go fast on your own but you go far together. Sounds cliché but it is especially true in treasury as the treasury department is dependent on data from other departments to make it function. You cannot run risk analysis if you have no exposure data. Same for FX. Doing cash flow forecasting? You need data from procurement, AR and FP&A.

Also visibility and transparency is key. Even the other financial departments accounting and controlling sometimes see treasury as this special people that they have no idea what they are exactly doing. Make sure they understand (and vice versa) what each department does and how you can work together and what data can be shared. Also to avoid duplicating work. So leave the ivory tower and go out there and collaborate.

7. How have you seen the role of Corporate Treasury evolve over the years?

The speed and amount of information has increased and is increasing. Also the complexity of treasury departments. Luckily also the solutions available to manage them has improved. Next to swift solutions we now see advanced TMS solutions or payment hubs that can be implemented within a couple of months giving you full visibility. A treasurer nowadays needs some tech skills to be able to understand the information to implement the TMS or hub. Because the tool will be only be as good as it is being used; garbage in is garbage out. During the many implementations that I have done I have learned a lot about technical connections (sFTP, h2h, API), information exchange formats, XML file types, swift messages etc. This knowledge now helps me a lot in implementations and supporting the IT department determining the information needs and sources.

8. What developments do you expect in corporate treasury in the near and further future?

Instant payments are a big thing in treasury which is cool but will not necessarily bring much added value to the treasury. Instant information processing is more important especially in e-commerce. Clients expects instant service. If they pay online they expect to get the service or goods asap. Treasury can help with this by connecting their PSP’s or bank information to their systems. Not necessarily linking the payment to an invoice which is an accounting reconciliation process. More importantly linking the positive acknowledgment (the customers has paid) to the sales. Customers start demanding this more and more and treasury has to adapt to this instant world. This means more automation.

Clients also demand more payment options, some of them are not available at banks. This means that treasurers will have to move away from the traditional model of banking partners for cash management but to a more hybrid model of cash at bank, cash in transit at PSP’s, virtual credit cards, wallets etc. Maybe even crypto or CBDC deposits/balances. This will all add to the complexity of the cash and risk management.

Isn’t treasury the best department to be in? 😊 I already get excited saying this.

Get in touch with Patrick

Click here for his Expert Profile

Join Patrick and experts from Kyriba and Deloitte at the Panel Discussion: How Can Treasurers Overcome Today’s Security Challenges?

When? March 9

Start: 4.00 pm CET

Register here

Thanks for reading!

Kendra Keydeniers

Director Community & Partners, treasuryXL

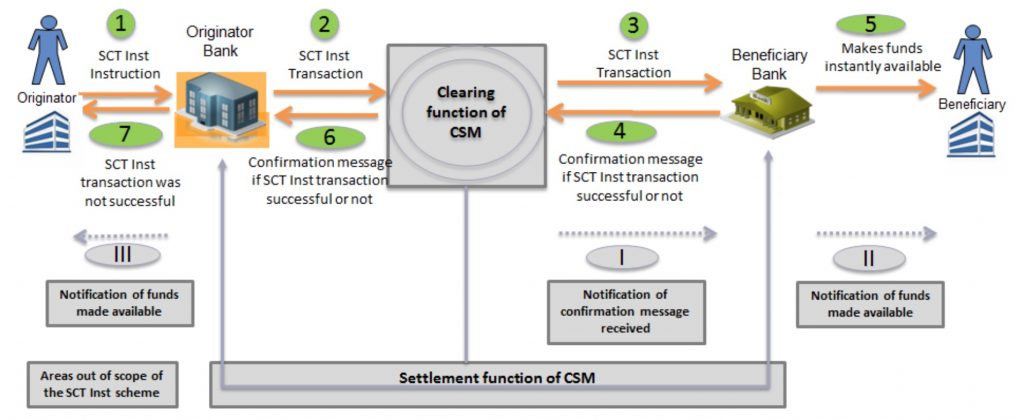

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.