BCR Publishing

We are the leading provider of news, market intelligence, events and training for the global receivables finance industry.

Working with industry leading organisations, experts, governments and universities, BCR Publications delivers expertise in factoring, receivables and supply chain finance to a global audience.

BCR has long been a beacon of innovation and excellence in the realm of receivables finance, playing an instrumental role in shaping the industry’s international landscape. Through its comprehensive conferences, insightful publications, and thought leadership, BCR has facilitated crucial dialogues and connections among industry professionals, driving forward the development of receivables finance globally.

Best read articles of all time – PSD 2: a lot of opportunities but also big challenges (Part I)

| 15-05-2018 | François de Witte |

PSD 2

PSD2 will cause important changes in the market and requires a thorough preparation. In this article, we are summarizing the measures and highlighting the impact on the market participants. In today’s Part I we will focus on abbreviations and main measurers introduced by PSD2.

List of abbreviations used in this article

2FA : Two-factor authentication

AISP : Account Information Service Provider

API : Application Programming Interface

ASPSP : Account Servicing Payment Service Provider

EBA : European Banking Authority

EBF : European Banking Federation

EEA : European Economic Area

PISP : Payment Initiation Service Provider

PSD1: Payment Services Directive 2007/64/EC

PSD2 : Revised Payment Services Directive (EU) 2015/2366

PSP : Payment Service Provider

PSU: Payment Service User

RTS : Regulatory Technical Standards (to be issued by the EBA)

SCA : Strong Customer Authentication

TPP : Third Party Provider

Main Measures introduced by PSD2:

The PSD2 expands the reach of PSD1, to the following payments:

A second important measure is the creation of the Third Party Providers (TPP). One of the main aims of the PSD2 is to encourage new players to enter the payment market and to provide their services to the PSU (Payment Service Users). To this end, it creates the obligation for the ASPSP (Account Servicing Payment Service Provider – mainly the banks) to “open up the bank account” to external parties, the so-called, third-party account access. These TPP (Third Party Providers) are divided in two types:

· AISP (Account Information Service Provider) : In order to be authorized, an AISP is required to hold professional indemnity insurance and be registered by their member state and by the EBA. There is no requirement for any initial capital or own funds. The EBA (European Banking Authority) will publish guidelines on conditions to be included in the indemnity insurance (e.g. the minimum sum to be insured), although it is as yet unknown what further conditions insurers will impose.

· PISP (Payment Initiation Service Providers): PISPs are players that can initiate payment transactions. This is an important change, as currently there are not many payment options that can take money from one’s account and send them elsewhere. The minimum requirements for authorization as a PISP are significantly higher. In addition to being registered, a PISP must also be licensed by the competent authority, and it must have an initial and on-going minimum capital of EUR 50,000.

Banks will have to implement interfaces, so they can interact with the AISPs and PISPs. However, payment initiation service providers will only be able to receive information from the payer’s bank on the availability of the funds on the account which results in a simple yes or no answer before initiating the payment, with the explicit consent of the payer. Account information service providers will only receive the information explicitly consented by the payer and only to the extent the information is necessary for the service provided to the payer. This compliance with PSD2 is mandatory and all banks will have to make changes to their infrastructure deployments.

A third important change is the obligation for the Payment Service Providers to place the SCA (Strong Customer Authentication) for electronic payment transactions based in at least 2 different sources (2FA: Two-factor authentication) :

The EBA (European Banking Authority will provide further guidance on this notion in a later stage. It remains to be seen whether the current bank card with pin code is sufficient to qualify as “strong customer authentication”. This “strong customer authentication” needs to take place with every payment transaction. EBA will also be able to provide exemptions based on the risk/amount/recurrence/payment channel involved in the payment service (e.g. for paying the toll on the motorway or the parking).

PSD2 also introduces some other measures:

In a second article soon to be published on treasuryXL, François de Witte will focus on the impact PSD2 has on market participants.

[button url=”https://www.treasuryxl.com/community/experts/francois-de-witte/” text=”View expert profile” size=”small” type=”primary” icon=”” external=”1″]

[separator type=”” size=”” icon=””]

Best read articles of all time – FX Swaps vs Libor and EURIBOR: Arbitrage opportunities?

| 10-05-2018 | Rob Söentken |

As we are getting closer to the end of the month, end of Q2 and end of H1 of 2016, it is interesting to see financial markets are maneuvering to get the right liquidity on board for the balance sheet. Or get rid of the unwanted liquidity. For firms with liquidity in various currencies the best means for liquidity management is FX swaps.

What is an FX swap?

In a very simple definition the FX swap is like an exchange of deposits. The big advantage is that the counterparty risk is reduced due to the exchange of notional. Operationally an FX swap is booked as two FX transactions: one to convert and another to revert. The conversion rate is against the prevailing exchange rate. The reversion rate is against the conversion rate plus or minus some ‘swap points’, which reflect the interest rate differential between the respective currencies. During the tenor the exchange rate could change, which creates counterparty risk on the mark-to-market value of the reversion. Mark-to-market risk for tenors up to 1 year is still a small when compared to full notional risk.

How would an FX swap work in theory?

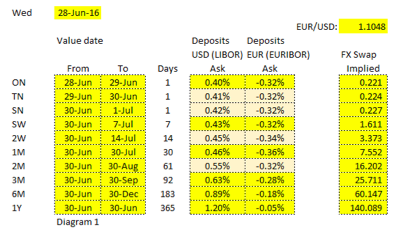

In diagram 1 the Libor and Euribor fixings for USD and EUR are listed for the respective tenors. Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows:

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows:

For the conversion date we take value spot (ie 2 days, in this case that is per June 30th) and we agree to exchange EUR 1 Mio vs USD 1.1048 Mio (because EUR 1 Mio at current spot of 1.1048 is USD 1.1048 Mio)

For the reversion date we take the value date for 1 year from today’s spot date. We calculate the following amounts including interest:

EUR 1 Mio x (1 + -0.05% x 365 / 360) = EUR 999,493.06

USD 1.1048 Mio x (1 + 1.20% x 365 / 360) = USD 1,118,241.73

Dividing the USD amount by the EUR amount gives the exchange rate for the reversion on the forward date, in this case that is 1.1188089. This is called the ‘forward rate’ The difference to the spot exchange rate is 0.0140089. For simplicity reasons this is multiplied by 10,000 to 140.089. This reflects the interest differential.

When executing an FX swap the EUR amounts are kept constant for both the spot and forward dates. But the USD amounts are calculated using the spot and forward exchange rates as calculated above. Therefor the interest differential is reflected in the USD amount being different between spot and forward date.

How does it work in reality?

As I mentioned at the beginning of this article, the current situation is special because we are getting close to a date special and important for balance sheet reporting. Supply and demand may push the market in a direction.

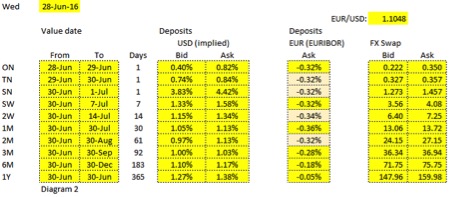

When looking at the actual FX swap rates and taking the EUR Euribor fixings as given, we can deduce the implied USD funding rates (see diagram 2). First observation is that the FX swaps appear to reflect either a substantial demand for USD from June 30th to July 1st, or a EUR supply. It is interesting to see that the 1 week fixing for EUR was not affected, while the 1 week FX swap was affected maybe 20 bppa. One reason could be the timing of the rates. Euribor is taken at one moment during the day, while FX swaps are affected by events during the day. Because w e are looking at a single day FX swap, the annualized rate could swing a lot.

e are looking at a single day FX swap, the annualized rate could swing a lot.

Another observation is that the interest rate differential between EUR and USD is actually bigger than implied by the fixings. For one month tenor the difference is 0.59% p.a.. It would seem possible that supply – demand forces can push FX swaps away from the deposit markets. Likely the counterparty limit constraints on pure deposits keep them from being arbitrages vs FX swaps, like they used to be many years ago.

How can a treasurer benefit from FX swaps?

Each individual and organization should determine for itself what he/she or it needs. And I do not want abstract from discussions around documentation requirements, collateral financing and administration, and the operational extra work. It seems obvious that there are opportunities to investigate.

One key area would be to look at the bid-offer spreads on cash liquidity in various currencies as provided by house-banks and compare those rates with and without using FX swaps. Also I could imagine non-house banks could be more competitive in providing FX swaps, while the counterparty risk is substantially smaller than when pure lending is concerned.

Rob Söentken

Ex-derivatives trader

Best read articles of all time – Beleggen in obligaties met een hoge rente – een bespiegeling

|09-05-2018 | Douwe Dijkstra – Fastned- Het Financieele Dagblad |

Hoe interessant is beleggen in bedrijfsobligaties met een hoge rente? Hoe aantrekkelijk is deze financieringsoptie voor ondernemingen? Wij hebben onze experts Douwe Dijkstra en Pieter de Kiewit om een kort commentaar gevraagd naar aanleiding van de obligatie uitgifte van Fastned.

Op de site van Fastned was begin december 2016 te lezen:

‘U kunt nu investeren in Obligaties Fastned met 6% rente’. Later in de maand ging de tekst verder: ‘We zijn verheugd u te kunnen mededelen dat Fastned de inschrijving is gestart voor de uitgifte van obligaties. De obligaties hebben een looptijd van 5 jaar en keren per jaar 6% rente uit. Dit is een mooie kans om (verder) te investeren in de groei van Fastned en een duurzame wereld.’

Vervolgens werden de belangrijkste kenmerken van Obligaties Fastned genoemd.

Dat de obligaties zeer gewild waren blijkt vandaag. Op de site van Fastned verschijnt nu een tekst dat alle obligaties geplaatst zijn. En Fastned vervolgt:

‘Gezien de grote interesse in obligaties Fastned zijn er zeker voornemens om binnenkort nog een uitgifte te doen.’

In het Financieele Dagblad kon men op 6 december een Bartjens commentaar lezen over de Fastned obligaties: Het principe is simpel: een wankel bedrijf leent geld. Beleggers willen de relatief grote kans op wanbetaling gecompenseerd zien met een behoorlijke vergoeding: dus een hoge rente. In de VS zijn junkbonds populair, hier is het een kleine markt. Maar deze week is er weer een onvervalst speculatieve obligatie uitgegeven. Fastned. Het bedrijf dat een Europees netwerk van snellaadstations voor elektrische auto’s bouwt, leende € 2,5 mln. De lening heeft een looptijd van vijf jaar. De couponrente is 6%. Ter vergelijking: de Nederlandse Staat (superveilig) leent voor vijf jaar tegen 0%, Shell (behoorlijk veilig) leent voor vijf jaar tegen een coupon van 1,25% en Gazprom (Russisch, iets minder veilig) leent in Zwitserse frank voor vijf jaar tegen 2,75%. De 6% van Fastned impliceert dus behoorlijke risico’s. Het bedrijf is klein, jong en verlieslatend. Het heeft geen reserves en een negatief eigen vermogen, zo blijkt uit het prospectus. Maar goed, ‘de cost gaet voor de baet uyt’ en juist nu moet Fastned investeren.’

Expert Douwe Dijkstra vult hierop aan:

Voor beleggen in Fastned obligaties geldt hetzelfde als voor elke andere investering. Het rendement is omgekeerd evenredig aan het risico. Zolang niemand weet of de koers van aandelen Koninklijke Olie omhoog of naar beneden gaan, weet zeker niemand of beleggen in een 6% obligatie van Fastned achteraf wel of geen goede investering zal blijken te zijn geweest. Het lijkt mij enkel aantrekkelijk voor beleggers die wel een gokje durven te wagen met een te overziene inzet die ze wel kunnen missen. Of voor beleggers met een ideologische wereldvisie. Vorige week las ik in een ander artikel nog dat die investeerders met een loep gezocht moeten worden.

En Pieter de Kiewit zegt:

Investeren in start-ups gaat mijns inziens gepaard met een andere investeringsanalyse dan in volwassen ondernemingen. Daarbij is de ‘groene factor’ voor vele beleggers reden anders naar een onderneming te kijken. Dit is bijvoorbeeld heel zichtbaar bij Tesla. Persoonlijk vraag ik me af of een avontuurlijke investeerder in dit geval niet beter een equity investering kan doen.

Vanuit Fastned perspectief kan ik, met hun vertrouwen in hun business case, begrijpen dat ze liever obligaties uitgeven dan nieuwe aandelen..

Douwe Dijkstra

Owner of Albatros Beheer & Management