TRAINING: PSD2 & Open banking: impact on the financial ecosystem and new challenges

| 23-11-2020 | Francois De Witte

On December 16th, our Expert Francois de Witte will present a Webinar in collaboration with Febelfin-Academy, regarding PSD2 & Open banking: impact on the financial ecosystem and new challenges.

This training program prepares participants for 2 major challenges of the upcoming years in banking: PSD2 & Open Banking. This will have a major impact on the financial ecosystem and will create new challenges.

The goal of this training course is to:

- Make participants aware of the ways PSD2 & Open Banking affect banks and other players in Europe;

- Understand the impact of the technical requirements with a focus on strong customer authentication;

- Outline the risks and responsibilities of the involved parties within the new regulatory framework;

- Understand the impact of Open Banking APIs (Application Programming interfaces;

- Understand the impacts of the PSD2 & Open Banking the financial ecosystem;

- Evaluate the risk and opportunities created by PSD2 & Open Banking the banks and the new players;

- Determine action plan for your company.

Target Audience

This training course can be followed by multiple target groups:

- Managers of a banks/PSP’s/Fintechs involved with the payments and digital strategy

- Product Development Experts (payments)

- Service providers involved with Open Banking

- Corporate Treasurers

- Compliance officers

Prior Knowledge

Advanced: offers practice-based applications to complement the theoretical knowledge already acquired through the “basic level” courses (in-depth learning).

There is no specific preparation required. For persons who are less acquainted with PSD2 and payments, some pre-course reading material can be made available.”

Program

This training program prepares participants for two key challenges of the upcoming years in banking: PSD2 and Open Banking.

Part I: PSD2 and Open Banking – overview:

- PSD2: Scope and Basic Principles

- XS2A (Access the Accounts)

- New Players: AISP and PISP

- SCA (Strong Customer Authentication)

- Consent and SCA

- Requirements for the Banks and TPPs

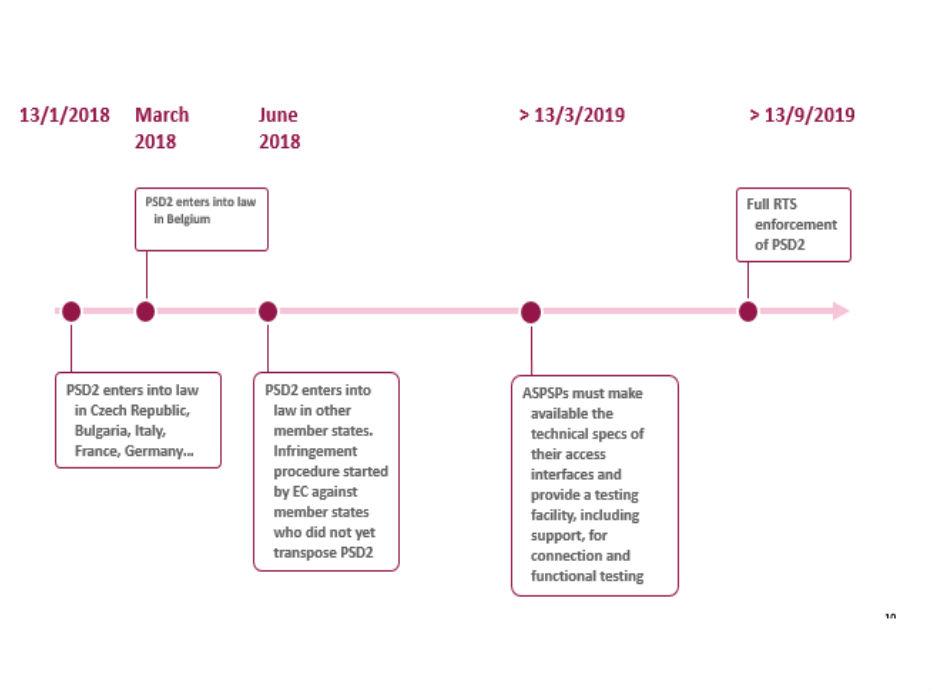

- Timetable

- Trends in Open Banking

Part II: Open banking architecture: Implications for banks and the New Players

- XS2A: Risks, Responsibilities and obligations of the related parties

- XS2A: Availability Requirements

- Setting up the SCA in Practice

- SCA: Optimization of the Exemptions

- Security requirements ensuring consumer protection

- Addressing the fraud and cyberattack risks

- Technology: building interfaces – APIs (Application Programming Interfaces)

- European initiatives to standardize the interfaces

- Practical aspects – Role of Aggregators

- Group Exercise

Part 3: PSD2: Potential impact on the market and next steps

- Global impact on the market – New Players

- Impact on the Payments Landscape

- Impact on the Cards and Digital Payment Instruments

- Impact on the Merchants and the e-commerce

- Impact on corporates

- FinTech Companies: ready to disrupt banks?

- Implication on the Digital Banking Strategy

- The new role of competition and cooperation

- Action Plan for Banks and New Players

- Group Exercise

Practical information

Duration: One day training

Date: December 16, 2020

Hours: 9AM-5PM (6 training hours)

Location: This training will be given online

Additional information: This training course will be given in English

Pricing: Members (€510), Non-Members (€610), Partner BZB (€510)

François de Witte

François de Witte

Anja Biehler

Anja Biehler