Ripple is making blockchain waves

| 23-03-2018 | Carlo de Meijer |

Almost a year ago I wrote my blog “Blockchain and the Ripple effect: did it Ripple?”. Now twelve months later we may conclude it did. And even more than that. Ripple is making many waves. A lot happened both in broadening their offerings and in enlarging their network. A growing number of banks and payment providers, increasingly join RippleNet, Ripple’s decentralized global network, to “process cross-border payments efficiently in real time with end-to-end tracking and certainty”. By using the growing set of Ripple solutions they are able to expand payments offerings into new markets that are otherwise too difficult or too expensive to reach. The focus of Ripple therefor has especially moved towards emerging markets.

Almost a year ago I wrote my blog “Blockchain and the Ripple effect: did it Ripple?”. Now twelve months later we may conclude it did. And even more than that. Ripple is making many waves. A lot happened both in broadening their offerings and in enlarging their network. A growing number of banks and payment providers, increasingly join RippleNet, Ripple’s decentralized global network, to “process cross-border payments efficiently in real time with end-to-end tracking and certainty”. By using the growing set of Ripple solutions they are able to expand payments offerings into new markets that are otherwise too difficult or too expensive to reach. The focus of Ripple therefor has especially moved towards emerging markets.

BROADENING RIPPLE OFFERINGS

Ripple was set up in 2012 to create a streamlined, decentralized global payments system named RippleNet, using technology inspired by the blockchain, to record transactions between banks. RippleNet is an enterprise-grade blockchain platform, that nowadays has over 100-member banks and financial institutions. These partners can use all the Ripple offerings.

Solutions

Ripple makes software products based on blockchain technology and sell them to banks, payment providers and others to be used on RippleNet. These are aimed to make cross border payments truly efficient for these players and their customers. Next to their digital asset XRP, the XRP Ledger, and xCurrent, that helps banks settle transactions, Ripple has added a number of new services/offerings to the platform including xRapid and xVia. This in order to attract more clients to enter RippleNet. Ripple is now taking the next step to help build the Internet of Value (IoV), by establishing an Infrastructure Innovation Initiative.

a. XRP: digital asset

From the outset, XRP, Ripple’s digital asset was expected to be an important part of Ripple’s decentralised payment system. Ripple uses its own XRP cryptocurrency as a payment method to make it easier for banks to move money internationally. Banks and payment providers can use Ripple’s digital asset XRP to further reduce their costs and access new markets. One rationale for using XRP is that unlike Bitcoin, the token has one narrowly defined (payments method!) but clearly useful purpose: to help banks move cash faster and more cheaply, especially across borders. The token could be used as a kind bridge currency between fiat currencies. For example South African rands in Johannesburg could become XRP, which could then be turned into baht in Thailand. That could help banks avoid the time consuming and expense of tying up money in different currencies in accounts at other banks.

b. xCurrent: processing payments

RippleNet is powered by xCurrent, for payment processing. xCurrent is the new name of Ripple’s existing enterprise software solution that enables banks to instantly settle cross-border payments with end-to-end tracking (and bidirectional messaging across RippleNet). It provides real-time messaging, clearing and settlement of financial transactions. The xCurrent messaging platform however does not involve XRP. It includes a Rulebook developed in partnership with the RippleNet Advisory Board to standardise all transactions across the network. That ensures operational consistency and legal clarity for every transaction. The Interledger Protocol (ILP) is the backbone of the solution and makes it possible for instant payments to be sent across a variety of different networks.

Read the full article of our expert Carlo de Meijer on LinkedIn

Economist and researcher

On Tuesday 13th March 2018, RTL Z – a television channel – broadcast a “Cryptoshow” to explain how the Blockchain works and what it could mean for the future. They attempted to make the technology and information as simple as possible to show what uses the Blockchain could have in the world for consumers and businesses. One of the main areas of interest relates to Smart contracts. What are they? What are the advantages and disadvantages? What changes can they bring?

On Tuesday 13th March 2018, RTL Z – a television channel – broadcast a “Cryptoshow” to explain how the Blockchain works and what it could mean for the future. They attempted to make the technology and information as simple as possible to show what uses the Blockchain could have in the world for consumers and businesses. One of the main areas of interest relates to Smart contracts. What are they? What are the advantages and disadvantages? What changes can they bring? Long-time regulators world-wide took a wait-and-see attitude towards the non-regulated markets for Bitcoin and cryptocurrencies. But that is changing rapidly. With the growing popularity of the crypto market, the large number of unregulated cryptocurrencies (more than 1300, greater attention is now being paid by Governments and other stakeholders around the world.

Long-time regulators world-wide took a wait-and-see attitude towards the non-regulated markets for Bitcoin and cryptocurrencies. But that is changing rapidly. With the growing popularity of the crypto market, the large number of unregulated cryptocurrencies (more than 1300, greater attention is now being paid by Governments and other stakeholders around the world. There are various signals that a number of corporates are moving their blockchain projects towards production. We recently have seen the announcement of the IBM – Maersk project, to create a blockchain based corporate. If accepted in a sufficient way by the various players in the shipping industry supply chain that could mean a real breakthrough for blockchain and other distributed ledger technologies. “The big thing that is missing from this industry to digitize and unleash the potential of the technology is really to create a form of utility that brings standards across the entire ecosystem,” Maersk’s Chief Commercial Officer Vincent Clerc.

There are various signals that a number of corporates are moving their blockchain projects towards production. We recently have seen the announcement of the IBM – Maersk project, to create a blockchain based corporate. If accepted in a sufficient way by the various players in the shipping industry supply chain that could mean a real breakthrough for blockchain and other distributed ledger technologies. “The big thing that is missing from this industry to digitize and unleash the potential of the technology is really to create a form of utility that brings standards across the entire ecosystem,” Maersk’s Chief Commercial Officer Vincent Clerc. Payments is increasingly seen as an area that is ripe for disruption, having the potential to enhance payment processing. To overcome the current structural weaknesses in the payments area including low speed, high expenses, financial institutions are increasingly adopting the idea of blockchain or distributed ledger technology (DLT). This in order to offer (near) instant cross-border payments at lower costs, higher security and more reliability. Up till recently most of these trials have been non-interoperable stand-alone solutions. But that may change!

Payments is increasingly seen as an area that is ripe for disruption, having the potential to enhance payment processing. To overcome the current structural weaknesses in the payments area including low speed, high expenses, financial institutions are increasingly adopting the idea of blockchain or distributed ledger technology (DLT). This in order to offer (near) instant cross-border payments at lower costs, higher security and more reliability. Up till recently most of these trials have been non-interoperable stand-alone solutions. But that may change! Having spent my working life in international finance, I have patiently listened to all the news about the Bitcoin over the last few years. During 2017 whilst the Bitcoin was on a spectacular price rise, my interest was awakened in this new phenomenon – is this the future? I attended seminars, read articles, learnt the difference between the Bitcoin and the Blockchain, searched and investigated via the web, and tried to form an opinion. These are my findings:

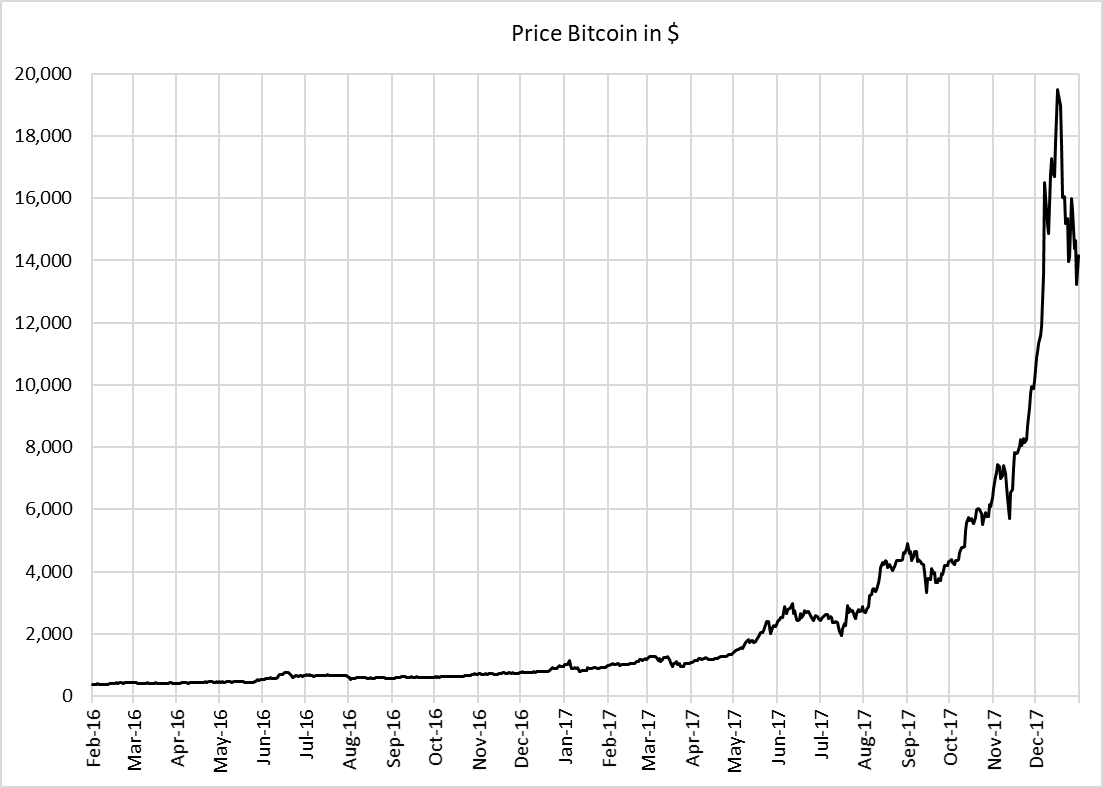

Having spent my working life in international finance, I have patiently listened to all the news about the Bitcoin over the last few years. During 2017 whilst the Bitcoin was on a spectacular price rise, my interest was awakened in this new phenomenon – is this the future? I attended seminars, read articles, learnt the difference between the Bitcoin and the Blockchain, searched and investigated via the web, and tried to form an opinion. These are my findings: Such a stellar performance should mean that the trade volume has increased dramatically.

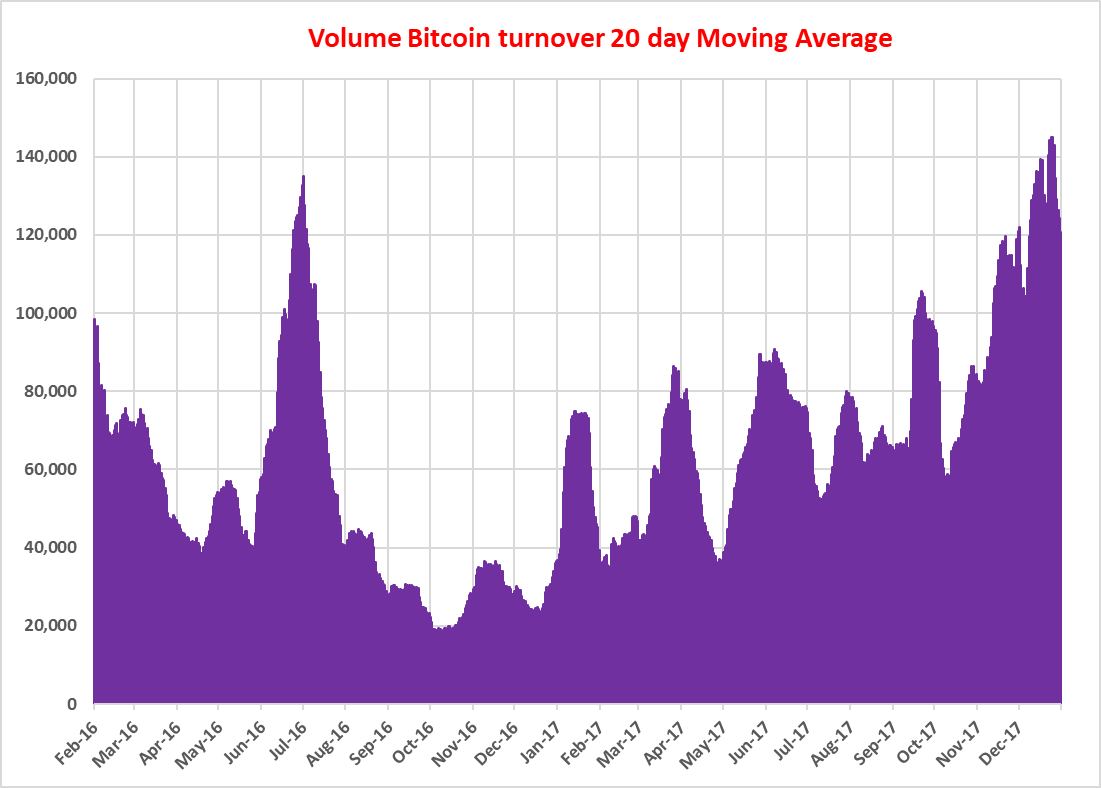

Such a stellar performance should mean that the trade volume has increased dramatically. The daily volume in September 2017 when the price was about $4,000 was the same as the start of February 2016 when the price was about $400. I had to create this chart as all the data I could find related to the $ value of turnover – which was phenomenal – and not the actual number of Bitcoins traded. Normally, when an asset sees a huge increase in price, this goes together with a corresponding increase in turnover. Clearly this has not happened with Bitcoin – why?

The daily volume in September 2017 when the price was about $4,000 was the same as the start of February 2016 when the price was about $400. I had to create this chart as all the data I could find related to the $ value of turnover – which was phenomenal – and not the actual number of Bitcoins traded. Normally, when an asset sees a huge increase in price, this goes together with a corresponding increase in turnover. Clearly this has not happened with Bitcoin – why?

During our stay in South Africa I was reading an article in Die Burger (newspaper for Afrikaners) where a spokesman of Cape town-based PWC gave his ideas on the recent rise of Bitcoin and the future of Blokketting (Afrikaans for Blockchain). This inspired me to write this blog. Since I started writing about blockchain I categorically refused to use the term Bitcoin. But this time it is different. As Bitcoin nears the end of a record-breaking year, it seems an appropriate time to dive into this – by many traditional players said – over-hyped thing. Others describe this fascination for Bitcoins as a “speculative mania”. The broader public has discovered this phenomenon. I will not say it is (already) the end of the rise in Bitcoins or other crypto currencies. But let me be clear: Bitcoin is a lot not!

During our stay in South Africa I was reading an article in Die Burger (newspaper for Afrikaners) where a spokesman of Cape town-based PWC gave his ideas on the recent rise of Bitcoin and the future of Blokketting (Afrikaans for Blockchain). This inspired me to write this blog. Since I started writing about blockchain I categorically refused to use the term Bitcoin. But this time it is different. As Bitcoin nears the end of a record-breaking year, it seems an appropriate time to dive into this – by many traditional players said – over-hyped thing. Others describe this fascination for Bitcoins as a “speculative mania”. The broader public has discovered this phenomenon. I will not say it is (already) the end of the rise in Bitcoins or other crypto currencies. But let me be clear: Bitcoin is a lot not! In May this year, fintech start-up R3 raised $107 million from a consortium of the world’s top banks. The New York-based blockchain company that works in collaboration with more than 90 banks and other financial organizations world-wide, plans to use the money to invest in further developing the Corda platform (see my blog: Corda: distributed ledger ….. not blockchain! April 6, 2016) as well as “encouraging entrepreneurs to start building on the platform though training videos and hackathons”.

In May this year, fintech start-up R3 raised $107 million from a consortium of the world’s top banks. The New York-based blockchain company that works in collaboration with more than 90 banks and other financial organizations world-wide, plans to use the money to invest in further developing the Corda platform (see my blog: Corda: distributed ledger ….. not blockchain! April 6, 2016) as well as “encouraging entrepreneurs to start building on the platform though training videos and hackathons”.  My last blog was about IBM, triggered by a Juniper Research putting the company as the number one in the blockchain technology competition. One of the comments on this blog was that it looked like an IBM press release. But that is far beyond what is meant. I just looked at what the tech company was doing in the blockchain arena and why it could be adopted as the main blockchain model when blockchain adoption could become mainstream. In a previous blog I already talked about Microsoft’s CoCo platform, the number two in the Juniper Research asking myself if that could become a game changer (see my Blog: Microsoft CoCo Framework: blockchain game changer, August 29, 2017). Today I will go into some more detail in the blockchain activities of Accenture, number three according to the Juniper survey.

My last blog was about IBM, triggered by a Juniper Research putting the company as the number one in the blockchain technology competition. One of the comments on this blog was that it looked like an IBM press release. But that is far beyond what is meant. I just looked at what the tech company was doing in the blockchain arena and why it could be adopted as the main blockchain model when blockchain adoption could become mainstream. In a previous blog I already talked about Microsoft’s CoCo platform, the number two in the Juniper Research asking myself if that could become a game changer (see my Blog: Microsoft CoCo Framework: blockchain game changer, August 29, 2017). Today I will go into some more detail in the blockchain activities of Accenture, number three according to the Juniper survey.