Online checkout starts before the payment solution (Dutch Article)

| 17-11-2021 | treasuryXL | EcomStream | Ramon Helwegen |

Het sleutelmoment in de e-commerce-funnel is de betaling. Online betalen blijft een hobbel, zeker in vergelijking met het gemak van contactloos en zonder pincode betalen in de winkel. Snelle en gemakkelijke betaling online verdient daarom speciale aandacht.

Het is goed om je te realiseren dat een klant online meerdere processen doorloopt voordat een conversie kan plaatsvinden. Tijdens dit proces bied je de klant zoveel mogelijk aandacht, beleving en gerichte informatie over dat waar hij of zij naar op zoek is. Dit alles binnen de ‘wetten’ van de optimale online klantbeleving.

Snel betalen

Maar zodra de klant de keuze definitief heeft gemaakt volgt het betaalproces. Voor jou als verkoper is dat een belangrijk proces op weg naar conversie, maar voor je klant is het een noodzakelijk kwaad waarin hij inhoudelijk veel minder geïnteresseerd is. De keuze is gemaakt en je klant wil gewoon zo snel mogelijk weg. In dit proces is snelheid dus van het grootste belang. Hoe sneller je klant kan betalen en vertrekken, hoe kleiner de kans dat hij alsnog afhaakt.

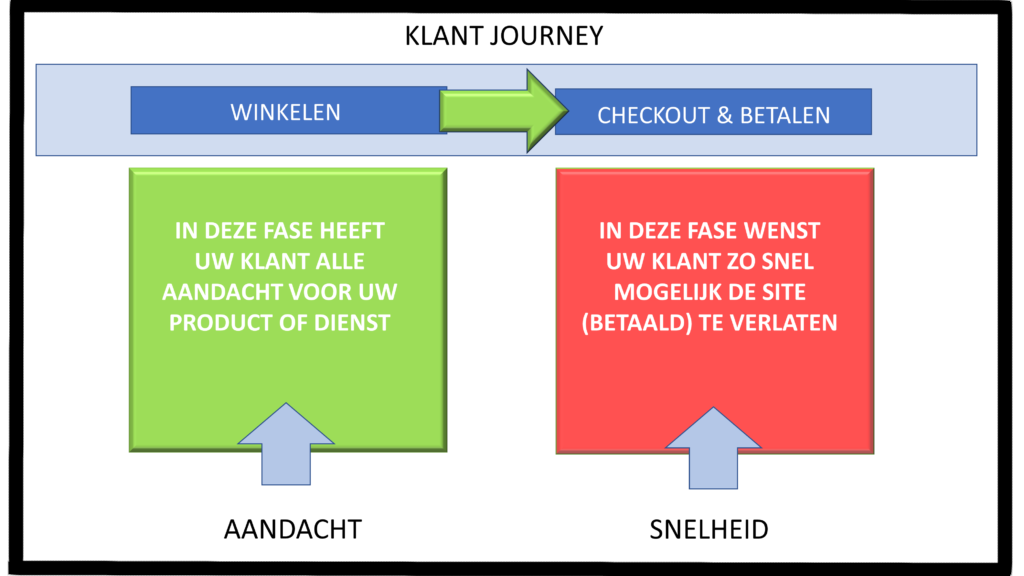

De online sales funnel is geen lineair proces. Knip het daarom in tweeën:

- Online shoppen = Aandacht en beleving

- Online afrekenen = Snelheid

Schematisch zou je er zo naar kunnen kijken:

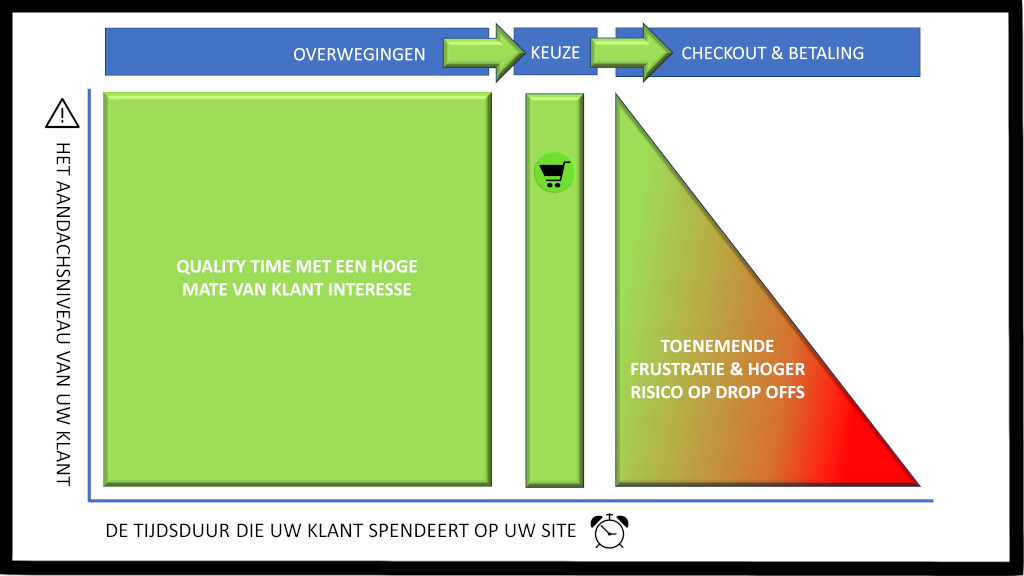

De snelheid van het afrekenproces bepaalt mede of je klant het inderdaad gaat halen tot en met de betaling. Hoe meer tijd je klant kwijt is aan dit proces, hoe groter de kans op afhakers (drop-offs).

Het grootste deel van het afrekenproces bevindt zich overigens buiten het domein van de betaalprovider. Er zijn uitzonderingen, bijvoorbeeld wanneer je klant met PayPal betaalt, maar dan gaat het dus om een situatie zonder vrije keuze van de betaalmethode. Ook is de afweging vanuit het ‘kosten-versus-conversie’-oogpunt in dit geval vaak uitdagend.

Het online afrekenproces eindigt bij de betaaloplossing

Mooi zo: je klant heeft het gehaald tot aan de betaalpagina. In dit laatste gedeelte van de checkout is de betaaloplossing van je betaalprovider wél van grote invloed op de conversie. Zowel net vóór de betaling als net ná de betaling door je klant.

Enkele aspecten van net vóór de betaling waarbij de betaaloplossing van invloed is op de conversie lees je hieronder. Het gaat hier over zaken die van toepassing zijn op de betaalpagina. Het gaat hier over aspecten die van toepassing zijn op de betaalpagina. Dus vanaf de keuze van betaalmethode, ofwel het moment dat je klant daadwerkelijk wil gaan betalen. Ook noem ik aspecten van net ná de betaling waarbij de betaaloplossing van invloed is op de conversie. Het gaat hier om aspecten waarbij je klant het hele checkout-proces met succes heeft doorlopen, op de laatste betaalknop heeft gedrukt, en er toch een kink in de conversiekabel komt.

- De juiste mix van relevante betaalmethoden. Je PSP kan je hier onderbouwd inzicht in geven. Welke betaalmethoden zijn in je marktsegment noodzakelijk om een optimale conversie te behalen. Kijk hiervoor ook naar verschillende landen en voorkeuren. Maar maak per betaalmethode ook de ‘kosten-versus-conversie’-afweging.

- Zorg dat alleen klanten voor wie de betaalmethoden relevant zijn deze te zien krijgen op de betaalpagina. Het heeft bijvoorbeeld geen zin om een Engelse klant te confronteren met iDEAL als mogelijke betaalmethode.

- Zorg ervoor dat je klant de betaling doorloopt in de look & feel van je bedrijf. Ook als je nog gebruik maakt van een redirect-pagina naar je betaalprovider.

- Geef klanten de mogelijkheid om betaalgegevens op te slaan. Dat stimuleert niet alleen herhalingsaankopen, maar het invoeren van een 16-cijferig creditcardnummer geeft een grote kans op fouten.

- Een responsive mobiele klantbeleving met een finger-friendly numeriek toetsenbord en een numerieke veldherkenning is wel zo prettig voor je klant.

- De ‘achtergelaten winkelwagen’-recovery. Een verlaten winkelwagentje opvolgen in een branded e-mail kan je klant motiveren om toch af te rekenen.

- Retries: wordt de betaling toch niet geaccepteerd? Zorg er dan voor dat je klant een alternatieve betaalmethode krijgt aangeboden, maar zonder dat de winkelmand per ongeluk wordt geleegd.

- Fraude: een klant kan met een gestolen credit card afrekenen, of het geleverde ter discussie stellen. In beide gevallen staat de conversie op losse schroeven. Verkoop je een fraudegevoelig product of een fraudegevoelige dienst, zorg dan voor een goede fraudemanagementoplossing waarmee je de balans tussen je conversie en je frauderatio goed kunt managen.

- Het optimaliseren van autorisatie-success rates op creditcardtransacties: dit is vooral interessant als je veel naar relatief ‘exotische’ landen verkoopt waar de autorisatie success rate op creditcards laag kan zijn. Steeds meer PSP’s bieden netwerkoplossingen waarmee ze de autorisatie-success rate kunnen verbeteren.

Conclusie

In de winkel betalen kan tegenwoordig makkelijk en snel. Je houd je telefoon dicht bij de terminal en klaar. Online betalen is helaas vaak nog tijdrovend. Want zodra je klant in het online winkelmandje op “bestellen” klikt wordt een checkout-proces doorlopen. De optimalisatie van dit proces vindt plaats binnen en buiten het domein van je betaalprovider. Een snel checkout-proces met een geoptimaliseerde klantbeleving helpt je klant om deze laatste fase van je funnel met succes te doorlopen.

About EcomStream

EcomStream is an independent consultancy and is specialized in optimization of online, omnichannel and marketplace payment solutions, and optimization of checkout flows.

The goal is to achieve much lower costs for you while creating a much better customer experience for your customers.

Thanks to its lean organisational model, EcomStream will help you to reduce the cost of ownership of your payment solution and to improve your ROI, fast.