Option Tales: Cheap Options Part III

| 31-05-2016 | Rob Söentken

Today in Rob Söentken’s Option Tales: When buying options it is tempting to see if the premium expenses can be minimized. A number of solutions are possible, which will be discussed in four articles. In the previous article I talked about choosing the longer tenor and the compound option. Today I will discuss the average rate option (ARO) and the conditional premium option.

Average Rate Option (ARO)

An Average Rate Option (ARO) can be misleading because it is like a vanilla option except for the reference rate against which it is exercised. The reference rate for an ARO is an average based on spot rates for USD taken at predetermined intervals. For a vanilla option it is the single rate for spot at maturity. If the intention was to hedge the rate for USD in 1-year time, the average of USD rates during the year is really something different.

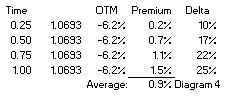

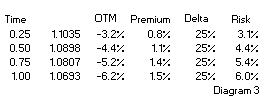

If we would be looking to hedge a 1-year tenor and the averaging would be at quarterly intervals, a rough and quick estimate of an ARO’s cost would be the average premium of separate vanilla options for respective tenors, in this case that would be 0.9% (see diagram 3). Which would be considerably less than a vanilla option costing 1.50%.

But unlike a strip of options which can be exercised individually, an ARO can only be exercised in total. At maturity the averaging of the fixings is mostly done, and it could happen that while the last fixing is In The Money (ITM), the average of the fixings is not, making the ARO expire worthless. In this example it would be advantageous to have a strip of vanilla options because each option would be exercisable independently of the other. The ARO on the other hand is worthless because the average would still be above the strike. This inherent risk in using an ARO will make the premium of an ARO even a bit cheaper than a strip of vanilla options.

The bottom line remains that the premium of an ARO is lower than a vanilla option for the same tenor, because the embedded tenor of the ARO is really shorter. The effect is comparable to paragraph 2 ‘Choose shorter tenor’. Slightly worse even when considering the averaging effect.

Conditional Premium Option

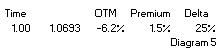

A Conditional Premium Option has the advantage over a vanilla option in that premium only has to be paid if the option is In-The-Money (ITM). But… if the option is ITM the premium will be a multiple of a vanilla option. The premium of such a Conditional Premium Option is calculated by dividing the premium of a vanilla option (1.5%, see diagram 5) by the chance it will be exercised (Delta, in this case 25%), ie 1.5% : 25% = 6%. It could be a very disappointing to find that if this Conditional Premium option is only marginally ITM at maturity, because the premium of 6% still has to be paid.

(1.5%, see diagram 5) by the chance it will be exercised (Delta, in this case 25%), ie 1.5% : 25% = 6%. It could be a very disappointing to find that if this Conditional Premium option is only marginally ITM at maturity, because the premium of 6% still has to be paid.

A Conditional Premium Option is constructed by buying a vanilla option and selling a digital option with the same strike. The digital option will be for a payout of 6% and because it also has a chance on exercise of 25% it will generate 1.5% premium, offsetting the premium of the vanilla option.

Next week in the last Option Tales article; the Reverse Knock-Out Option (RKO).

Would you like to read more on Rob Söentken’s Option Tales?:

2. ATM or OTM

3. Cheap Options part I

Ex-derivates trader

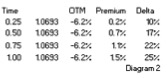

bought the option for 1.5%, we could sell it after 3 months at 1.1% and buy the USD through an outright forward transaction. This approach shows that the net cost of option protection would be only 0.4% (1.5% – 1.1%). Which would be cheaper than the premium of a 3-month option with the same Delta. Also, because the option has a higher Delta than a 3-month option with the same strike (25% vs 10%, see diagram 2), it will follow the spot market much better. The bottom line of paragraph 3 is that a longer dated option can be bought with the intention to sell it again at some point, the net cost being less than buying a shorter dated option. While it serves as a hedge against price changes.

bought the option for 1.5%, we could sell it after 3 months at 1.1% and buy the USD through an outright forward transaction. This approach shows that the net cost of option protection would be only 0.4% (1.5% – 1.1%). Which would be cheaper than the premium of a 3-month option with the same Delta. Also, because the option has a higher Delta than a 3-month option with the same strike (25% vs 10%, see diagram 2), it will follow the spot market much better. The bottom line of paragraph 3 is that a longer dated option can be bought with the intention to sell it again at some point, the net cost being less than buying a shorter dated option. While it serves as a hedge against price changes. buy the 1-year option in diagram 2 for 1.5%. Alternatively we could consider buying a right to buy this option for 0.4% in 3 months time. At that time the 1-year option will only have 9 months remaining, but the strike and 1.5% premium are fixed in the contract. On the expiry date of the compound option we can decide if we want to pay 1.5% for the underlying option. Alternatively, assuming nothing has changed, we could buy a 9 month option in the market for 1.1% (see diagram 2). In such a case we wouldn’t exercise the compound option.

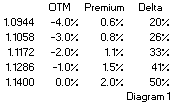

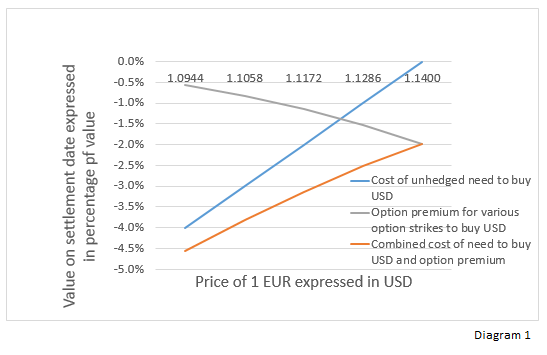

buy the 1-year option in diagram 2 for 1.5%. Alternatively we could consider buying a right to buy this option for 0.4% in 3 months time. At that time the 1-year option will only have 9 months remaining, but the strike and 1.5% premium are fixed in the contract. On the expiry date of the compound option we can decide if we want to pay 1.5% for the underlying option. Alternatively, assuming nothing has changed, we could buy a 9 month option in the market for 1.1% (see diagram 2). In such a case we wouldn’t exercise the compound option. Should we need to exercise the option to get our USD, it still means a combined hedging cost of 3.8%. Which is more than if we had bought the ATM option for 2% premium. Conclusion: Buying an OTM option reduces the up-front cost versus buying an ATM option. But ex-post hedging with an OTM option could result in total hedging cost which are higher than an ATM option.

Should we need to exercise the option to get our USD, it still means a combined hedging cost of 3.8%. Which is more than if we had bought the ATM option for 2% premium. Conclusion: Buying an OTM option reduces the up-front cost versus buying an ATM option. But ex-post hedging with an OTM option could result in total hedging cost which are higher than an ATM option. option is exercised, or the USD must be purchased from the market at the prevailing rate.

option is exercised, or the USD must be purchased from the market at the prevailing rate.

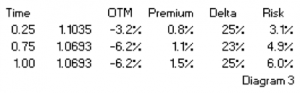

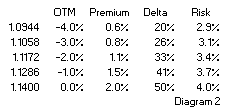

Risk appears fairly stabile across strikes, which makes sense because the premiums are calculated with one volatility on one underlying. The Risk on OTM is lower than that for ATM options. It appears that OTM premiums are relatively more expensive, they give protection against less potential loss.

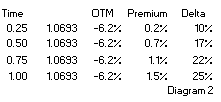

Risk appears fairly stabile across strikes, which makes sense because the premiums are calculated with one volatility on one underlying. The Risk on OTM is lower than that for ATM options. It appears that OTM premiums are relatively more expensive, they give protection against less potential loss. Diagram 3 shows Premiums, Delta and Risk for different tenors. ‘Time’ is the time to expiry of the options in fractions of years. Its shows that for longer tenors, the Risk is higher. But disproportionally. For the same chance on exercise a hedger could double the premium to buy a hedge for a 4x longer tenor.

Diagram 3 shows Premiums, Delta and Risk for different tenors. ‘Time’ is the time to expiry of the options in fractions of years. Its shows that for longer tenors, the Risk is higher. But disproportionally. For the same chance on exercise a hedger could double the premium to buy a hedge for a 4x longer tenor.