Automation doesn’t make FX, equities and fixed income traders unnecessary, but it does make them more efficient – which ultimately can lead to better profits.Read more

https://treasuryxl.com/wp-content/uploads/2020/08/Refinitiv.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-05-05 07:00:512022-05-05 16:26:10Rapid changes in trading are taking place. Are you keeping pace?

In December 2021, LIBOR setting publication ceased on over two dozen settings. But the transition is far from over as phasing out continues for legacy contracts.

As of the end of last year, 24 LIBOR settings have ceased publication.

The FCA confirmed Synthetic LIBOR to be allowed for the temporary use of “synthetic” sterling and yen 1M, 3M and 6M LIBOR rates in all legacy LIBOR contracts.

The main challenge that remains is the USD LIBOR Transition

Since the end of 2021, publication of 24 LIBOR settings has stopped (CHF, EUR, GBP, USD and JPY) and the most used GBP and JPY LIBORS are now being published with a new methodology called “synthetic LIBOR”.

USD LIBORs will continue to be published until mid-2023 using panel bank submissions. Discussions surrounding Euribor are ongoing, but EU regulators appear to be waiting until the LIBOR cessation has fully taken place to define a more detailed agenda for Euribor.

To sum it up – the LIBOR transition is not yet over!

On 16 November 2021, the FCA confirmed Synthetic LIBOR to be allowed for the temporary use of “synthetic” sterling and yen 1M, 3M and 6M LIBOR rates in all legacy LIBOR contracts.

This applied to all other than cleared derivatives, that have not been changed at or before 31 December 2021.

The Synthetic LIBOR are published on existing Refinitiv Instrument Codes (RICS), as shown in Figure 1.

Figure 1: Refinitiv Eikon LIBOR= quote

Synthetic LIBOR methodology

Synthetic LIBOR = ISDA Median Spread + Term Rate.

For example, the JPY 3M Synthetic LIBOR value published on JPY3MFSR= RIC is calculated as per below:

The main challenge that remains is the USD LIBOR transition. Even with the cessation set to 30 June 2023, market participants have been asked to implement transition and identify fallbacks by regulators.

Even if the use of USD LIBORs has been discouraged and drastically limited for new contracts, data from DTCC and ISDA suggests that LIBOR contracts were traded in January 2022 but in low volumes.

The FCA defined clearly the stipulations in Further Provision and Information in relation to the Prohibition and the Exceptions:

The market-making exception applies only where market-making is undertaken in response to a request by a client seeking to reduce or hedge their USD LIBOR exposure on contracts entered before 1 January 2022.

The prohibition does not prohibit new single currency USD LIBOR basis swaps entered in the interdealer broker market.

The lack of credit component in SOFR appears to raise some issues, mostly from regional banks, that also stressed the fact that borrowers will struggle with SOFR. LIBOR is a forward-looking term rate and interests are known upfront, with SOFR and other alternative Risk-Free Rates (RFR), interest is compounded and only known at the end of the period.

*Please note that credit-sensitive rates such as Ameribor, AXI or BSBY are available in Refinitiv Eikon but are NOT endorsed by the ARCC or FCA.

On the cash market, the Alternative Reference Rates Committee (ARRC) Progress Report, published on 31 March 2021, estimated there will be approximately $5trn USD LIBOR referencing contracts in business loans, consumer loans, bonds and securitisations maturing after June 2023.

Many of these exposures may have suitable fallback language and will be able to transition away from LIBOR prior to cessation.

ARRC has selected Refinitiv to publish its recommended spread adjustments and spread adjusted rates for cash products. The USD IBOR Cash Fallbacks provide market participants, including lenders and borrowers, with an industry-standard agreed rate, which can clearly and easily be referenced in contracts.

Refinitiv launched USD IBOR Consumer Cash Fallbacks 1-week and 2-month settings on 3 January 2022.

As mentioned in the December 2021 Bank of England Risk-Free Rate Working group newsletter, the transition towards Risk-Free Rates is progressing steadily, as per the charts in Figure 5 for cleared swaps and exchange-traded futures:

Figure 5: Cleared Swaps and Exchange Traded Futures

In a Risk.net article, Philip Whitehurst, Head of Service Development, Rates at LCH (part of LEG Group) said: “Sterling LIBOR was the most substantial population LCH had converted, amounting to about 185,000 trades for around $15trn worth of cleared swaps. They were converted into Sterling Overnight Index Average (SONIA) equivalents on a compensated basis.

“The same was applicable for around 75,000 yen LIBOR trades, with aggregate notional of about $4.5trn, and 25,000 to 30,000 Swiss LIBOR trades worth about $1.5trn, as well as a very small population of euro LIBOR trades.”

Whitehurst stressed that Euribor trades were not converted.

On the OTC Derivatives markets, the adoption of new Risk-Free Rates is very high.

GBP, CHF and JPY swaps are now exclusively done on new Risk-Free Rates. SOFR swaps are progressing versus LIBOR, at a quite slow pace, and now represent close to 50 percent of the traded notionals, according to ISDA swaps info figures.

Unsurprisingly, the exception remains EUR, where fewer than 30 percent of the traded notionals are on €STR.

Cross-currency swap markets are rapidly ditching legacy interest rate benchmarks in favour of RFRs.

Since the beginning of 2022, trades in euro/dollar cross-currency OTC swaps have almost exclusively referenced the secured overnight financing rate (SOFR) and the euro short-term rate (€STR).

DTCC data repositories from U.S. markets data show how 95 percent of USD / GBP, USD / JPY and USD / CHF now trade RFR versus RFR.

The transition has been pushed by RFR First initiatives, the second phase of SOFR First, launched in September 2021. It stated that interdealer trading conventions for cross-currency basis swaps between USD, JPY, GBP, and CHF LIBORs will move to each currency’s risk-free rates.

Cross-currency swaps prices can be found in Refinitiv Eikon, using the OTC advanced search tool, the OTC Pricer App and the Swap Pricer app, which now allow price cross-currency swaps based on new RFRs.

Although 24 LIBOR settings have already been discontinued, this does not spell the end of the LIBOR transition.

Market participants are still actively transitioning away from LIBOR trades in USD, while getting prepared for other IBORs transitions in the Eurozone and the rest of the world.

https://treasuryxl.com/wp-content/uploads/2022/04/ref-200-5-april.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-04-05 07:00:002022-04-04 18:23:02The LIBOR transition is far from over

https://treasuryxl.com/wp-content/uploads/2020/08/Refinitiv.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-03-07 07:00:262022-03-04 15:58:10Your new home for fixed income

Andrew Hollins, Director of Corporate Treasury Proposition at Refinitiv, brings you a round-up of the latest Corporate Treasury Data Insights, including corporate treasury activity during COVID-19 illustrated through Refinitiv’s usage data, a Refinitiv report on ESG risk and whether carbon markets matter to COP26.

Corporate treasury activity illustrated through Refinitiv data usage saw the COVID-19 pandemic split into three distinct phases.

The initial phase concentrated on credit risk data and analytics, as well as corporate financial data. Meanwhile, phase two focused on cash balances, and phase three honed in on ESG data and analytics as the world moved towards the ‘new normal’.

Other areas of corporate treasury under the microscope included risk mitigation and ESG, carbon markets and COP26, and the state of the U.S. labour market.

Refinitiv’s usage data paints a fascinating picture of corporate treasury activity throughout the pandemic. As events unfolded, we saw interesting and distinct dynamics play out.

We’ve discerned three phases of the pandemic.

Phase 1: the survival phase

The standout feature of this initial period was the focus on credit risk data and analytics, highlighted by an unprecedented increase in usage of the Credit Default Swaps app – 155 percent in EMEA, and 120 percent in Asia and the Americas.

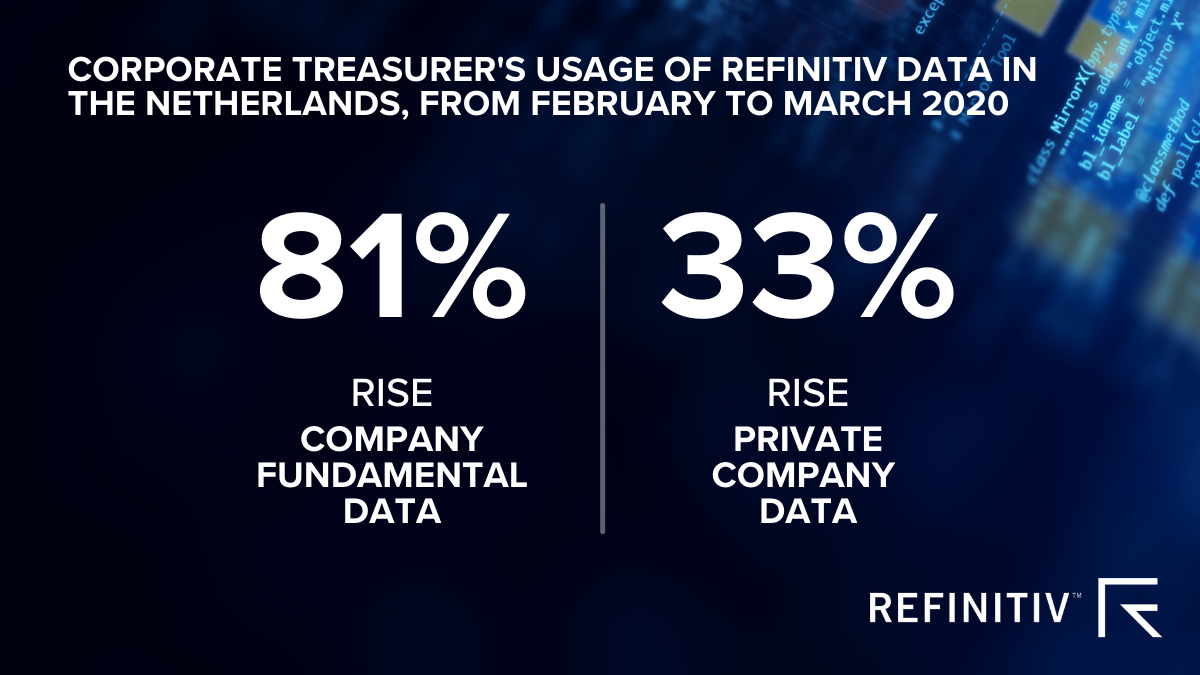

Demand for corporate financial data also grew strongly – notably company fundamental data (usage up 81 percent), private company data (usage up 33 percent), sectoral data, and peer analysis (usage up 113 percent).

Conversely, during this initial phase, we saw a distinct fall in demand for ESG and LIBOR-related data and analytics.

Phase 2: the cash and corporate health phase

From June to September 2020, activities aimed at boosting cash balances were very much apparent. Our data showed a notable acceleration in corporate debt issuance.

In addition, there was also another, even bigger, jump in demand for company fundamental data with usage of key ratios and cashflow data growing by 160 percent and 175 percent respectively.

Phase 3: return to ‘new normal’

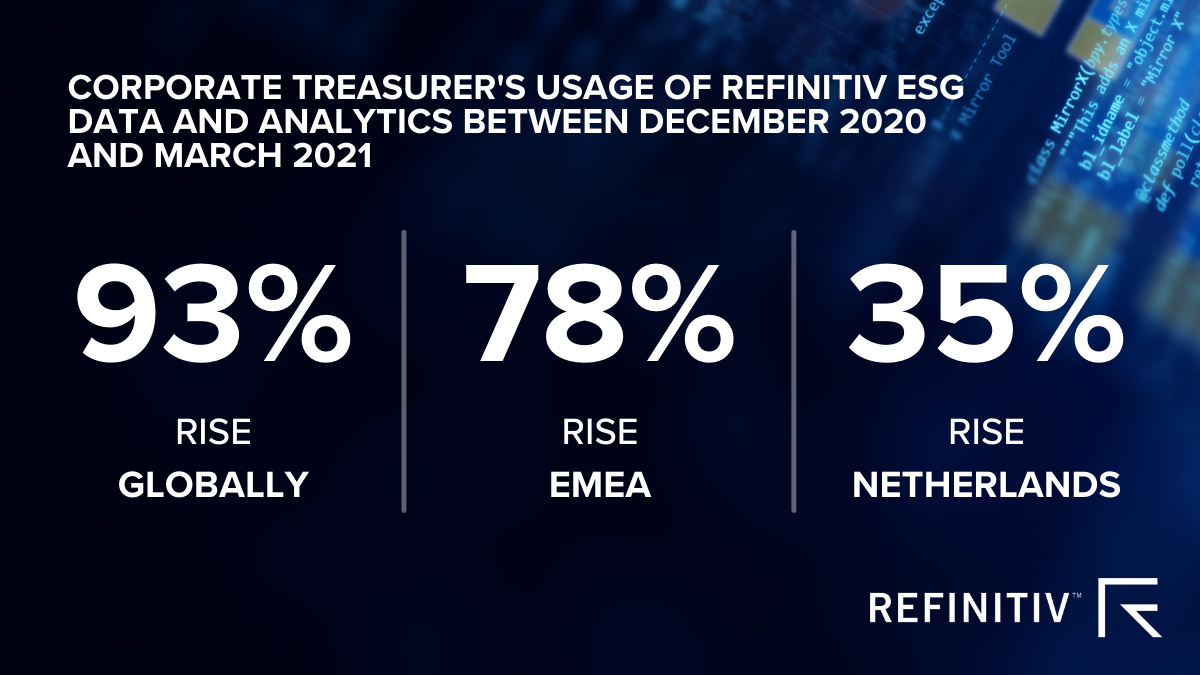

Emerging from the pandemic demand for ESG data and analytics is once again rising strongly. Between December 2020 and March 2021, it has grown by 93 percent to stand well above pre-COVID-19 levels.

This trend is likely to continue its upward trajectory given the rapidly evolving regulatory and demand-led factors that seem to be driving the focus on sustainability.

Refinitiv unpacks more of our usage data insights in a new masterclass series produced in collaboration with TreasuryToday.

Refinitiv report: Risk mitigation and the pivotal role of ESG

The far-reaching consequences of COVID-19 have forever changed the risk landscape, and rising levels of third-party risk now demand urgent attention.

Persistent gaps in formal due diligence must clearly be addressed, but a broader sea change is needed: both financial institutions and corporates need to adopt a more holistic approach to risk management – one that incorporates environmental, social and governance considerations as a fundamental tenet of the risk mitigation process, rather than as a separate silo.

Carbon markets are a key tool for countries to cut their greenhouse gases and meet their Paris Agreement commitments.

The cost of polluting is rising in Europe, parts of North America, South Korea and New Zealand. Most likely it will do so in China, the latest country to launch a national emissions trading system.

The COVID-induced rigidities in the U.S. labour market are easing, but the labour market remains extremely tight, implying potential upwards pressure on inflation from wages.

Refinitiv launches USD IBOR Institutional Cash Fallbacks in production to facilitate industry transition from USD LIBOR | Refinitiv has announced that USD IBOR Institutional Cash Fallbacks are now production benchmarks, and it will launch USD IBOR Consumer Cash Fallbacks 1-week and 2-month settings pending Refinitiv Benchmark Services (UK) Limited (“RBSL”) board approval. Read more

https://treasuryxl.com/wp-content/uploads/2021/05/TreasuryXL-Refinitiv-Newsletter-Thumbnail.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2022-02-01 07:00:482022-02-01 08:49:19Corporate Treasury Data Insights: trends in COVID-19 Refinitiv usage data

LG Electronics is a global leader and technology innovator in consumer electronics, mobile communications and home appliances. Following an analysis of the market, LG decided to implement a trading and confirmation solution in order to improve its foreign exchange processes. Read the case study to find out more.

LG Electronics is a global leader and technology innovator in consumer electronics, mobile communications and home appliances, employing 87,000 people working in 113 locations around the world. With 2013 global sales of US$53.1 billion, LG comprises five business units.

The company’s previous foreign exchange had several inefficiencies and risk of manual errors, and was difficult to audit. Too much time was spent on simple and mundane processing rather than value-added functions. The task for LG was therefore to find a solution that would allow the company to solve these inefficiencies and allow its staff to focus on other areas of the job.

As a solution, LG decided to implement a trading and confirmation solution in order to improve its foreign exchange processes. The system ensures that the best price will be available and LG can then execute on the platform electronically. With this innovative technology, LG has been able to really reduce its operational risk across their FX trading workflow.

“We now have the ability for users in our various Asia entities to create, modify and approve FX spot and forward orders electronically,” says Calvin Lee, Manager, Asia Pacific Treasury Centre at LG. “The solution will then electronically consolidate orders for our Regional Treasury Centre to control and feed approved orders to our relationship banks to obtain an electronic ‘multi-bank quote’”.

The new platform LG has implemented has greatly increased the efficiency of the company’s FX process while at the same reducing the risk the group was exposed to. On top of these advantages, LG has benefited from much-improved control as a result of implementing the solution.

Key benefits

Productivity gains

Process efficiencies

Foreign exchange gain(s)

Risk removed/mitigated

Increased control

https://treasuryxl.com/wp-content/uploads/2021/12/LGElectronics_RefinitivCustomerStories_Thumbnail.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2021-12-06 07:00:262022-01-28 10:07:34Refinitiv case study | How LG Electronics reduces operational risk across its FX trading workflow

Haier Group Corporation is a Chinese multinational consumer electronics and home appliances company, designing, manufacturing and selling a full range of smart appliances, whilst also focusing on channel integrated services. Read more about how Haier Group treasury has succeeded in establishing an intelligent risk management model, covering their whole workflow by connecting with their internal accounting and funds settlement system and externally linking financial data resources (such as Refinitiv) and more than ten global banks.

Haier Group Corporation is a Chinese collective multinational consumer electronics and home appliances company headquartered in Qingdao, China. The FX risk management function under Haier Group’s treasury now controls 22 countries and areas and 20 currency pairs. Their centralised management is difficult due to the wide range of regions and currencies, while the traditional analysis and management from manual booking does not keep up with the current business development demand. Haier Group treasury has succeeded in establishing an intelligent risk management model, covering the whole process by connecting with the internal accounting system and funds settlement system and externally linking the financial data resources (such as Refinitiv) and more than ten global banks.

https://treasuryxl.com/wp-content/uploads/2021/10/Haier_RefinitivCustomerStories_Thumbnail-1.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2021-11-01 07:00:232021-11-01 14:04:44Refinitiv case study | How Haier Group uses a one-stop FX Management solution to mitigate currency volatility

Mercuria is a global energy and commodity group, operating in more than 50 countries with over 1,000 employees and offices worldwide. Read more about why Refinitiv Eikon was selected to fulfill the complex cross-asset requirements from pre-trade, trade, through to post-trade and credit screening.

Mercuria’s business lines cover a diverse range of commodities trading as well as large-scale infrastructure assets. For that reason, they searched for a cross-asset platform to manage credit, pre-trade, trade and post-trade to quickly, efficiently and accurately access global market insights, trusted market data and ‘best-of-breed’ industry analytics to help price-up derivative products.

Refinitiv Eikon platform was selected to fulfil the complex cross asset requirements from pre-trade, trade, through to post-trade and credit screening.

https://treasuryxl.com/wp-content/uploads/2021/09/Mercuria_RefinitivCustomerStories_Thumbnail.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2021-10-04 07:00:522021-10-01 09:12:54Refinitiv case study | How Mercuria manages risk across assets with a single platform

The LIBOR transition: We explain what fallback rates for the USD cash markets are and provide practical insights on how these rates can be used.

Refinitiv USD IBOR Cash Fallbacks are designed to ensure existing USD LIBOR referencing products such as loans, bonds and securitisations can continue to operate post-USD LIBOR cessation.

There are two versions of the Refinitiv USD IBOR Cash Fallbacks: those for consumer products and those for institutional products.

Initially, market participants can use the prototype USD IBOR Cash Fallbacks to become more familiar with the rates and test technical connectivity.

During my previous blog on fallbacks in April 2021, I outlined the importance of introducing robust fallback rates into the USD cash markets.

There is a substantial exposure of cash instruments that have no effective means to easily transition away from LIBOR upon its cessation. New LIBOR legislation signed into State of New York law reduces the adverse economic outcomes associated with the instruments by requiring them to use the Alternative Reference Rates Committee’s (ARRC) recommended fallback language.

In March, the ARRC announced Refinitiv as publisher of its fallback rates for cash products. Since then, Refinitiv has been working with the Federal Reserve and the ARRC to finalise the design of the USD IBOR Cash Fallbacks.

Fallback rate economically equivalent to USD LIBOR

The Refinitiv USD IBOR Cash Fallbacks provide the rates described in the ARRC’s recommended fallback language.

These are composed of two components: the adjusted Secured Overnight Financing Rate (SOFR) part measures the average SOFR rate for the relevant tenor. Added to this is a spread adjustment, which measures the difference between the USD LIBOR for each tenor and SOFR compounded in arrears for that tenor.

Adding these two components together gives an all-in fallback rate that is economically equivalent to USD LIBOR.

There are two version of the Refinitiv USD IBOR Cash Fallbacks: those for consumer products and those for institutional products. Both are published to five decimal places and include the adjusted SOFR rate, the spread adjustment and the all-in rate.

Watch: Refinitiv Perspectives LIVE – The LIBOR Transition: Risk-Free Term Rates

Consumer cash fallbacks

Refinitiv USD IBOR Consumer Cash Fallbacks are designed to ensure existing USD LIBOR referencing consumer cash products such as mortgages and student loans can continue to operate post-USD LIBOR cessation.

These rates are based upon compound SOFR in advance, which means the rate is known at the start of the interest period, plus the spread adjustment.

Prior to 1 July 2023, the spread adjustment will be calculated as the median difference between USD LIBOR and SOFR compound in arrears for the previous 10 working days, resulting in the spread adjustment changing on a daily basis.

This is an indicative rate, and while it should not be used as a reference rate in financial products, it is designed to aid familiarity with the USD IBOR Consumer Cash Fallbacks prior to adoption in July 2023.

Following 30 June 2024, the spread adjustment will be calculated as the median of the historical differences between USD LIBOR for each tenor and the compounded in arrears SOFR for that tenor over a five-year period prior to 5 March 2021.

For the period between 1 July 2023 and 30 June 2024, the spread adjustment will be calculated as the linear interpolation between the two rates outlined above.

A floored version of the consumer cash fallbacks is also available, meaning that if the average SOFR across all days in the tenor is below zero, then the all-in published fallback rate will be solely the corresponding spread adjustment.

Refinitiv USD IBOR Consumer Cash Fallbacks will be published in 1-month, 3-month and 6-month tenors.

Institutional cash fallbacks

Refinitiv USD IBOR Institutional Cash Fallbacks are designed to ensure existing USD LIBOR referencing commercial cash products such as bilateral business loans, floating rate notes, securitisations and syndicated loans can continue to operate post USD LIBOR cessation.

In order to account for different conventions in different markets, there are a number of different versions of the Refinitiv USD IBOR Institutional Cash Fallbacks. There are three different ways of capturing the average SOFR rate: SOFR compound in arrears, Simple SOFR in arrears and SOFR compound in advance.

Added to this is the spread adjustment, which is calculated as the median of the historical differences between USD LIBOR for each tenor and the compounded in arrears SOFR for that tenor over a five-year period prior to 5 March 2021.

Unlike Refinitiv USD IBOR Consumer Cash Fallbacks, there is no transition period. This means that the spread adjustment remains fixed for perpetuity.

Each of the SOFR compound in arrears and Daily Simple SOFR rates will be available in up to seven tenors in a variety of different forms in order to conform to convention in different markets.

The 3-, 5- and 10-day lookback without observation shift versions give counterparties more notice by applying the SOFR rate from three, five and ten business days prior to the rate publication date.

The 2-, 3- and 5-days lookback with an observation shift versions also give counterparties more notice by applying the SOFR rate from two, three and five business days prior to the publication date, but in contrast to a lookback without observation shift, it applies that rate for the number of calendar days associated with the rate two, three and five business days prior.

The 2- and 3-day lockout versions fix the SOFR rate for the last two and three days prior to publication.

The plain version has no lookback, observation shift, or lockout.

The SOFR compound in advance rates for institutional products will be available in 1-month, 3-month and 6-month tenors.

Initially, market participants can use the prototype USD IBOR Cash Fallbacks to become more familiar with the rates and test technical connectivity.

Following the ARRC’s recent endorsement of Term SOFR, Refinitiv plans to supplement the initial prototype with a forward-looking term rate version in due course.

During the prototype phase, we anticipate changes to the methodology based on user feedback to ensure full alignment with industry standards prior to publication of the production rates.

Production rates for the institutional cash fallbacks should be available from autumn 2021, and for the consumer cash fallbacks they will be available from July 2023.

How to access the rates

Prototype rates are now available from the Refinitiv website and through Refinitiv products including Refinitiv® Eikon, Refinitiv Real-Time and Refinitiv® DataScope.

https://treasuryxl.com/wp-content/uploads/2021/09/LIBORTransition_Thumbnail.png200200treasuryXLhttps://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.pngtreasuryXL2021-09-14 07:00:512023-07-05 10:19:56Transitioning from LIBOR: Explaining the cash fallback rates

As a leading financial markets data provider, Refinitiv is an essential partner for corporate treasurers. Refinitiv’s global, multi-asset and multi-jurisdiction view of risk, credit and economic data enable treasury teams to drive stability by managing the global and interconnected nature of risk today.

⬇️ ⬇️ ⬇️

In this interview, we take a look at how Refinitiv’s corporate treasury customers used Refinitiv data and apps to remain agile and proactive in one of the most volatile years ever. We also consider what data is likely to be needed as we recover from the pandemic and companies seek growth.

Proposition Sales Specialist for Enterprise Solutions, Refinitiv, an LSEG business.

INTERVIEW

1. From your data, what can be identified about the behaviors and activities of corporate treasurers during the onset of the pandemic?

Using the data we have available, we’ve been able to discern three broad phases of corporate treasury response and action throughout the pandemic. The period March through to May 2020 represents Phase 1, which for many Corporates could be termed the ‘Survival Phase’. During this first phase, we witnessed pronounced patterns of activity amongst our Corporate Treasury clients.

Firstly there was a strong focus on analysing and reviewing the Credit Risk of suppliers, clients and also corporate’s own credit risk. Treasurers wanted to know if their customers would be able to pay for the goods and/or services they are supplying, and if their suppliers were still going to deliver supplies, raw materials, component parts, goods, etc.

We also saw a spike in usage of Company Fundamental Data(app for company financial analysis, for financial statements and valuation metrics for over 90,000 companies listed on 169 exchanges in 150 countries), especially so for balance sheets, income statements, key ratios and Cashflow data. Furthermore, there was an increased appetite for Private Company data, which almost certainly reflected a desire to review the health of the extended supply chain, a trend which has continued.

Finally, there was an increase in usage of Sector-specific Economic Indicator data, up 30% globally from Feb – Mar 2020 (this app allows users to search for any Economic Indicator, chart the history, export to Excel and view associated press releases). An increase was also seen in the use of Peer Analysis data (allows for the comparison of a company against its peers across a multitude of measures and variables), reflecting a demand for wider sectoral intelligence, as well as insight into how related companies were performing in such a stressed environment. Conversely, we also saw a decline in demand for ESG related apps and data, as well as data and apps relating to Libor transition. Libor transition in particular had been a high priority area for most corporate treasurers, but the economic shock brought on by Covid-19 pushed these onto the back burner during the ‘Survival Phase’.

2. What are the Data and App usage highlights from Phase 1?

Globally, Credit Default Swap (CDS) data usage grew 115% in EMEA and Americas between February and March 2020. Asia showed a 155% rise in usage of this data during the same period. (The CDS Dashboard app provides comprehensive Streaming price coverage on major global Index and single name CDS from major market maker).

In the Netherlands (February to March 2020), there was an 83% rise in usage by Corporate Treasurer’s use of credit and credit risk data, specifically;

68% rise in use of Debt Structure data (both for oneself and for one’s peers)

67% rise in Starmine Credit Risk data (Starmine Credit Risk models utilize industry-specific accounting ratios, equity market valuations and text mining models to produce a 1-100 score of an company’s credit risk).

During the same period we also saw significant increases in usage of company fundamental and private company data. At the same time there was a clear drop in consumption of ESG data.

81% rise in Company Fundamental data

33% rise in Private Company data

45% drop in use of ESG data

Looking at year on year data for the Netherlands for March 2020 and March 2021, we saw a 50% rise in CDS data; 50% rise in Debt Structure Data; 66% rise in Industry sector data; 113% rise in use of peer analysis apps.

Furthermore;

Private Company Data and Analytics grew by 31% between February to March 2020, receding during the summer months but then grew >100% from October 2020 into Q1 2021.

3. As the pandemic progressed, how did the behaviors and activities of corporate treasurer’s change?

Moving on from ‘Phase 1’ (above) and heading into ‘Phase 2’, which we can place from mid Q2 through to Q3 and call the ‘Cash Phase’, many companies focused on cash preservation and extending their cashflow runway as far as possible. Companies focused on maximising all sources of liquidity, in some cases working with suppliers to extend payment schedules and expedite receivables as far as possible. Companies also drew down reserves and utilised credit facilities. We also saw Bond Issuance accelerate significantly especially in Q3.

4. What are the Data and App usage highlights from Phase 2?

In the Netherlands, from June to October 2020, we saw a notable pick-up in usage of Issuance and Credit-related data and analytics:

A 40% rise in usage of the New Issues Monitor – (app providinga comprehensive library of new issues covered by Thomson Reuters and supporting IFR).

A more than 250% jump in usage of Starmine Credit Risk analytics and data

A 25% rise in usage of the Fixed Income All Quotes app

At the same time, there were also further significant changes in usage of apps and data related to the financial health of the supply chain and the corporate ecosystem in general:

Income Statement: Up 116%

Balance Sheet: Up 72%%

Key Ratios: Up 160%

Cashflow: Up 175%

5. How do you see the behaviors and activities of corporate treasurers changing as we move into a recovery mode from the pandemic?

If we identify Phase 3 as the ‘Recovery Phase’, which focuses on positioning and planning for a return to normality, or at least a new normal, our usage data suggests that many companies continue to focus on bond issuance and refinancing in order to take advantage of current lower yields. It’s notable that issuance of US$ denominated debt by non-US companies has been particularly strong in the first quarter of 2021.

There are distinct trends apparent in the usage data for our issuance-related Data and Analytics apps, in particular:

DCM Pricer – usage is up 21% from November 2020 to March 2021 (a custom bond calculator designed to build new bond issues and price them for the primary market)

Debt Structure app – usage is up 20% between November 2020 and March 2021

New Issues Monitor – usage is up 52% from November 2020 to March 2021 (New Issues Monitor provides a comprehensive library of new issues covered by Thomson Reuters and supporting IFR).

As countries navigate out of the pandemic, we can also see that ESG is firmly back on the agenda, with usage of our ESG apps and data rising strongly as we move deeper into 2021. For much of the pandemic period many companies focused on survival, but a rapidly developing global sustainability landscape is contributing to a significant shift towards adopting and ESG standards and behaviours across the corporate sphere.

Globally, ESG Data and Analytics Usage has grown 93% between Dec 2020 and March 2021, higher than the pre-Covid-19 peak.

Across EMEA, this was up 78% in the same period.

In the Netherlands, although below the global and EMEA percentages, ESG Data and Analytics usage was still up 35% in the same period.

Looking beyond Covid-19, conversations with our corporate treasurer clients have revealed an appetite for greater visibility and predictability when it comes to cash and liquidity management. Aligned to this, is a desire for increasingly accurate forecasts and risk analysis regarding projected future cashflows. Hedge accounting and hedge effectiveness tools also feature strongly in these conversations.

Furthermore, automation to support more robust and frequent analysis and reporting, as well as a comprehensive enterprise-wide view of cashflow, risk and liquidity, are also areas of growing interest which are going to feature more in the post-pandemic landscape.

Finally, ESG data consumption has recovered and is now above pre-Covid-19 peaks. This trend is likely to continue on its upward trajectory, becoming systemically more prevalent than it was pre-pandemic, given the rapidly evolving regulatory and demand led factors which are driving an ever-greater focus on sustainability. We recently hosted an event with the Association of Corporate Treasurers on treasury ESG roles and responsibilities which you can watch on-demand here.

6. How can corporate treasurers gain access to Refinitiv’s market-leading data and navigate current and future volatility?

Serving more than 40,000 institutions in approximately 190 countries, Refinitiv provides advanced data and technology to help corporate treasury teams make critical decisions with confidence. Our corporate treasury solutions help deliver accurate and relevant data, tools and analytics that can be accessed easily and intuitively – advancing your end-to-end workflows and ensuring seamless integration with your entire treasury management eco-system.

To find out more, speak with our experts by completing your details here.

Trusted by 15,000+ corporate treasurers, our Partner Refinitiv’s free monthly mail contains the latest Refinitiv data insights, must-read analysis and practical advice for Corporate Treasury teams. We dig into everything from Cash management, Market monitoring, Funding, Investments, Trading, Risk and Sustainable finance: supporting your workflow from start to finish.

Subscribe to their Corporate Treasury newsletter today to:

Receive expert analysis on marking-moving events

Keep ahead of industry developments and their impact on your team and business

Get exclusive access to our data-based insights and interactive charts

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.