Foreign currency hedging, a protection of cash flow

| 25-10-2017 | Rob Beemster |

Currency volatility is a well-known uncertain component of international business. In the pre-euro era one could suffer severely by currency movements of its European neighbours. Corporations, dealing within euro countries, have diminished the currency exposure.

Currency volatility is a well-known uncertain component of international business. In the pre-euro era one could suffer severely by currency movements of its European neighbours. Corporations, dealing within euro countries, have diminished the currency exposure.

A historical overview of the euro versus the us dollar

Looking back over the last 60 years, we can see that from 1958 till early 1970s there was stability due to the Bretton Woods golden standard. At the end of this, the Vietnam War made it impossible to keep the dollar relation to gold. Early 1980s, the Reagan administration introduced a new economic policy; Reaganomics. Lower taxes and high governmental expenditure. This created a huge mess in America’s monetary situation. Interest rates went to enormous heights, the dollar climbed to unknown levels against the yen and European currencies. American exporters could not sell their products due to this high dollar.

Why the attention to Reaganomics? Well, the Trump administration is a vigorous trailer of the Reagan policy. Lower taxes might be introduced soon and Mr Trump also wants to invest heavily in infrastructure. Obvious, some similarities with Reagan. The new helm of the Federal Reserve Board will soon be appointed. When the board will have more hawks than doves, interest rates might raise sooner than expected. This might have consequences for the dollar and we may see here a reflection of the early 1980s.

Trump and the us dollar

It is known that President Trump regularly protests to so-called currency manipulators like China and Germany. Their trade policies are in his view unacceptable. Due to this view of Trump on currencies, it will be questionable whether he would tolerate a higher dollar at all. The highly unpredictable Trump policy makes it impossible to judge in what direction the dollar will manoeuvre.

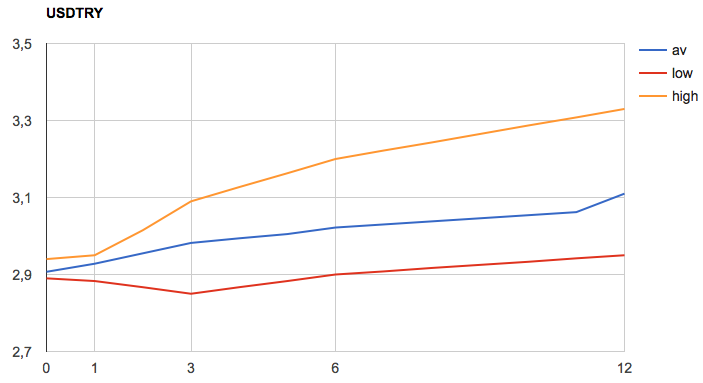

The highly volatile euro/us dollar

The dollar has fluctuated severely since the euro introduction in 1999. ECB’s first President, Mr Duisenberg was facing tough times as the euro went from its introduction level of 1.17 to the low of 0.8350 a couple of years later. His world trip to recommend the euro as world reserve currency has realized a demand from authorities to stock euro’s in their currency reserve system. The aggressive build-up of FX reserves by Asian monetary authorities has helped to revitalize the euro. Duisenberg made it happen that the currency went up from low 0.80s to almost 1.60 against us dollar in a couple of years. This occurred not so long ago!

Two examples of neglected currency risk

1, many corporations have changed its landscape to the global market. A lot of exporters are billing their products in euros. A currency risk is obvious when these companies focus on one target area. Clients may find the products too expensive when euro is rising. So one runs indirectly a currency risk. Many countries have linked their currency to the dollar, so a change in the euro/us dollar may have consequence on your sales.

2, trading with China and agreeing to do the transfer in dollars, does not really mean that the risk exposure is in dollars. The transfer risk is in dollars, but the real currency risk is in yuan. Say, the European importer buys goods from China and both have agreed to do the payments in dollars. The Chinese counterparty will adjust the price of the goods when yuan moves against the dollar. The European corporation should install an us dollar/yuan currency risk hedging policy.

Don’t underestimate the course of currencies

Being an active international corporation is not easy, many components are changing markets constantly. Internet makes markets more transparent then ever thought, automation changes the landscape, consumer behaviour is sometimes not logical and newcomers/interrupters create new markets. Within this one has to deal with currency volatility. But this is a component one can conduct. Foreign currency strategy is essential for any internationally active corporation. Currency volatility cannot be underestimated and needs control.

Barcelona valuta experts can help you to create a decent foreign currency strategy. Call us on +31.654981315 or mail us via [email protected] for more information.

Owner of Barcelona valuta experts BV