| 06-08-2019 | Carlo de Meijer | treasuryXL

Since Facebook announced its plans to come up with their own digital currency named Libra, a heated debate has risen about whether central banks should issue their own digital currency.

Central banks worldwide have expressed their worries about Facebook’s plan. According to them the prospect of a tech firm (and may be also others in the future) with billions of users launching its own money potentially poses a threat to existing fiat state currencies and especially to monetary stability.

Long-time sitting at the side-lines, this plan may accelerate the idea of a central bank digital currency (CBDC). Though there are no real plans (yet), are some strong arguments for central banks to start issuing their own digital currency.

This however raises a number of questions such as: What sort of digital currency?; What would be the main arguments? What role should banks play in this process? And, what would be the impact on financial stability?

Central banks counterbalancing Libra

Central bank are seriously watching the emergence of a new global digital currency called Libra, introduced by Facebook (see my Blog: Facebook and Libra: a global digital currency, 1 July 2019). The birth of Libra thereby serves as an “alert” for central banks and regulators.

There is growing belief that if Libra could be successfully launched, it would challenge central banks’ monetary sovereignty, posing a long-term threat to central banks control of money. Any role for Libra beyond the payment function could bring changes to the rules of the global monetary system, and regulators should pay close attention to that possibility.

“From the government’s perspective, we pay more attention to its influence on financial services, monetary policy and financial stability.”

Accelerating the launch of their own digital currencies by central banks could be a counterbalance.

Reactions

The initial cautious stance towards a central bank issued digital currency, ranging from wait-and-see to very negative, has firmly changed. Central banks and governments from all over the world as well as international financial institutions like the IMF and BIS are now sounding a much more positive tone.

IMF

It is interesting to find that already last year (November 2018) the International Monetary Fund (IMF) started to examine the potential innovative nature of digital currencies and has supported CBDC proposals more positively. Christine Lagarde, at that time Managing Director of the IMF, urged central banks to consider CBDC since they could satisfy public policy goals, including financial inclusion, security/consumer protection, and privacy in payments.

BIS

While just a few months ago, Augustín Carstens, the general manager for the Bank for International Settlements (BIS), was still questioning the value of central-bank-issued digital currencies, he recently acknowledged that central banks will likely soon need to issue their own ones.

Carstens warns that “big techs have the potential to become dominant” in this area thanks to network effects. Further, the arrival of such products “might just be around the corner if there is clear evidence of demand from the public”.

“And it might be that it is sooner than we think that there is a market and we need to be able to provide central bank digital currencies. If Facebook and big tech companies get their way, however they may have to.” Augustin Carstens

BIS is now supporting the many central banks’ efforts to research and develop digital currencies based on national fiat currencies. At the very least, the BIS concludes in its recent report, new “comprehensive” public policy is needed to “respond to big techs’ entry into financial services so as to benefit from the gains while limiting the risks.”

The potential implications of such a change towards central bank digital currencies for the stability of the global financial system however aren’t entirely clear, according to the BIS.

ECB

Though not taking an official position, a European Central Bank (ECB) official has come out generally in favour of wholesale central bank digital currencies (CBDCs).

Vitas Vasiliauskas, a member of the Governing Council of the ECB and chairman of the board of the Bank of Lithuania, said the question is not if but whether CBDCs should be retail, wholesale, or both. A retail CBDC would be available for the general public, while a wholesale version would be restricted to serve a limited circle, mostly financial institutions. In between these two types, “multiple theoretical sub-models also exist,” he said.

PBoC

The People’s Bank of China (PBoC), the country’s central bank is accelerating its efforts to introduce a government-backed digital currency, aiming at “securing a cutting-edge position in the global cryptocurrency race”. The central bank is organizing market-oriented institutions to jointly research and develop a central bank digital currency and the program has been approved by the State Council.

“A digital currency issued by the central bank can improve the efficiency of monetary policy, and help to optimize the payment system.”

China’s monetary authority identifies the nature of digital currency as “a substitute for cash”, rather than a speculative instrument. The use of cash is declining in China amid booming digital payment systems.

The central bank digital currency could be a new monetary policy tool, or an investment asset that carries an interest rate to satisfy investors’ demand for value. It might also be used as a reference for bank interest rates on deposits. The Chinese digital currency also could be used domestically. But “everything is just under discussion”.

Why CBDCs?

There are various arguments raised to issuing central bank issued digital currency based on DLT. The main are described below.

Towards a cashless society

One of the reasons mentioned is that in the Western world a growing number of people do not use cash anymore. Physical payments are thereby gradually replaced with electronic payments. CBDCs could provide a safe, liquid payment instruments to the general public. They have the potential to reduce cash handling costs since all the transactions can be made using a digital representation of money and are traceable.

…. and a formal based economy

A shift in central bank money from cash (physical money) to digital currency is another way to shift the economy from being informal-based to formal-based so that the economy becomes more tax-based, transparent, and efficient. This is especially relevant for emerging markets.

Increased financial inclusion

Another motivation for especially emerging economies regarding CBDC proposals is financial inclusion. In many of these countries a large number of people are unbanked and/or without access to commercial banks and the internet and thus excluded from conventional banking services. CBDC might promote digitization of the economy and, thus, economic and social inclusion.

More effective monetary policy

Shifting from cash to digital currency through issuing CBDC may enhance the effectiveness of monetary policy (such as a negative interest rate policy under the effective lower bound) because of limiting the scope of cash substitution that could emerge to avoid a negative interest rate.

Implementing CBDCs can allow new monetary policy tools to be used. Alternatively, CBDCs can be used as a tool to increase aggregate demand by making ‘helicopter drops’ of newly created CBDCs to all citizens, making it easier to meet the central bank’s monetary policy target of price stability.

Safer and more effective financial system

And there are the efficiency and financial stability gains to be get from CBDC. CBDC has the potential to improve the existing wholesale financial systems—including interbank payments and settlement systems, delivery versus payment systems, and cross-border payments and settlements systems.

Allowing individuals, private sector companies, and non-bank financial institutions to settle directly in central bank money (rather than bank deposits) may significantly reduce the concentration of liquidity and credit risk in payment systems.

This in turn could reduce the systemic importance of large banks. In addition, by providing a genuinely risk-free alternative to bank deposits, a shift from bank deposits to digital cash may also reduce the need for government guarantees on deposits, “eliminating a source of moral hazard” from the financial system.

Foster fintech sector

The use of CBDCs may promote a technological environment and foster the fintech sector. This is especially relevant for emerging economies. Those economies may find it difficult to develop banking systems and capital markets that are comparable to those in advanced economies. Fintech services are new and innovative.

Encourage competition and innovation

The regulatory framework would make it significantly easier for new entrants to the payments sector to offer payment accounts and provide competition to the existing banks. It would also reduce the need for most smaller banks and non-banks to run their payments through the larger banks (who are able to set transaction fees at a level that disadvantages their smaller competitors).

What sort of central bank digital currency?

When discussing the options of central bank digital currencies we can differentiate proposals into retail CDBC i.e. targeted to the general public and wholesale CBDC issued only for financial institutions. And there are multiple in-between types that may have characteristics of both retail and wholesale.

Retail CBDC

A retail CBDC is one that will be issued for the general public. Retail CBDC based on DLT has the features of anonymity, traceability, availability 24 hours a day and 365 days a year, and the feasibility of an interest rate application.

The retail proposal is relatively popular among central banks in emerging economies, mainly because of the motivation to take the lead in the rapidly emerging fintech industry, to promote financial inclusion by accelerating the shift to a cashless society, and to reduce cash printing and handling costs.

Wholesale CDBC

A wholesale CBDC is for financial institutions that hold reserve deposits with a central bank. It could be used to improve payments and securities settlement efficiency, as well as to reduce counterparty credit and liquidity risks.

A value-based wholesale CBDC would replace or complement reserves at the central bank with a restricted-access digital token. A token would be a bearer asset, meaning that during the transaction the sender would transfer value to the receiver, without intermediaries.

This would be something fundamentally different from the current system in which the central bank debits and credits the accounts without transferring actual values.

The wholesale CBDC is seen as the most popular proposal among central banks because of the potential to make existing wholesale financial systems faster, inexpensive, and safer. The Bank of International Settlements (BIS) also shares the view that wholesale CBDC could potentially benefit the payments and settlements systems.

Some experiments have been already conducted or examined by central banks since 2016—such as those in Canada called “CADcoin” under Project Jasper, Singapore Project Ubin, Japan-Euro Area Project Stella, Brazil, South Africa Project Khokha, and Thailand (Project Inthanon). (See my earlier blogs: Blockchain and Central Banks: A Tour de Table Part I and II, 3 and 9 January, 2017).

Retail versus wholesale CBDC?

Compared to emerging economies, central banks in advanced economies are not enthusiastic about retail CBDC. And that is not surprising. Many central banks do not wish to create competition between central bank money private sector money, taken into account the limited potential benefits from using retail CBDC.

A retail CDBC would be a step too far (or too early) for them. If a central bank issued a digital currency whereby everyone (including businesses, households and financial institutions other than banks) could store value and make payments in electronic central bank money (the r-CBDC variant), this could have wide-ranging implications for monetary policy and financial stability.

Wholesale Central Bank Digital Currency would bring a number of important efficiencies. Besides their retail payments and settlements systems are already highly efficient, almost real time, and always available. Most citizens are banked, while the use of cash in most European countries – with the exception of Sweden and Norway – is still rather high (and not declining in the same speed).

Moreover, wholesale CBDC technology would allow linking to other platforms. Directly linking securities or FX platforms to cash platforms could improve the speed of trades and eliminate settlement risk. Settlement on OTC markets, as well as for syndicated lending and trade finance could speed up considerably if linked live to an instant wholesale CBDC system.

Wholesale CBDC may also simplify (cross-border) payment infrastructure, strongly reducing the number of intermediaries involved. This may improve efficiency and security, minimise liquidity and counterparty risks and reduces cost.

Deploying DLT technology would also allow “smart” features to be added to wholesale CBDC, including earmarking funds, limiting their use in time and place, applying conditional interest rates and others. Such smart features would allow central banks to explore new and powerful operational monetary policy tools, such as tailor-made interest rates.

Finally. real-time monitoring and better track-and-trace options on a unified platform should facilitate both anti-money laundering efforts by banks and supervision over those efforts.

Coordinated CBDC approach

This wholesale approach is a likely first step towards more universal adoption of CBDCs. It is less disruptive and makes global payments cheaper, faster and more secure. But who should take the initiative to build the wholesale CBDC?

Only central banks have the mandate to issue a digital currency or token and call it legal tender. They however lack extensive experience and resources needed to build and maintain such an infrastructure and, build a compliance apparatus to supervise clients and transactions.

The private sector, on the other hand, has the necessary experience and resources to do this. Next to that, commercial banks also have an incentive, as regulation is becoming ever more stringent (KYC, AML), and makes it more costly to maintain a presence in payment systems in multiple countries.

Moreover, the current international payment system, based on correspondent banking, creates various costs such as KYC and handling costs of all banks involved. There are also delays due to opening hours in different time zones while liquidity is trapped in pre-funded nostro-accounts. A single cross-border 24/7 international direct payment and settlement system therefore is very attractive for them.

In order to build a successful wholesale CBDC, one needs the private sector’s experience and the central banks, thereby taking away the various counterparty risks. Moreover, jurisdictional differences need to be harmonised. So international public-private partnerships make sense.

Though this seems controversial, one should keep in mind that the existing monetary system is already a public-private partnership. While central banks determine monetary policy and monitor financial stability, commercial banks actually create most of the money by lending. Central banks (and other government agencies) in turn license and regulate them.

The way forward

Up till recently, not many central banks so far have found strong advantages of issuing their own digital currency at this stage because of several technical constraints.

The potential launch of Libra however has been an important wake-up call for a large number of central banks.

Given that blockchain technology has been progressing fast in the settlement and payment areas (as well as DLT), central banks may now see incentives to increase their interest in wholesale CBDC proposals and consider actual implementation seriously in the near future.

Wholesale CBDC however will still have to compete with upgraded legacy systems. Both central and commercial banks should therefore take a cautious approach when building completely new alternatives. Experimental wholesale CBDC that are cross-border from the start and involve multiple commercial and central banks, should have the biggest chance of success.

A retail CBDC however may be “a faraway goal” because of the potential adverse impact on commercial banks by promoting a shift of retail deposits from commercial banks to a central bank.

Carlo de Meijer

Economist and researcher

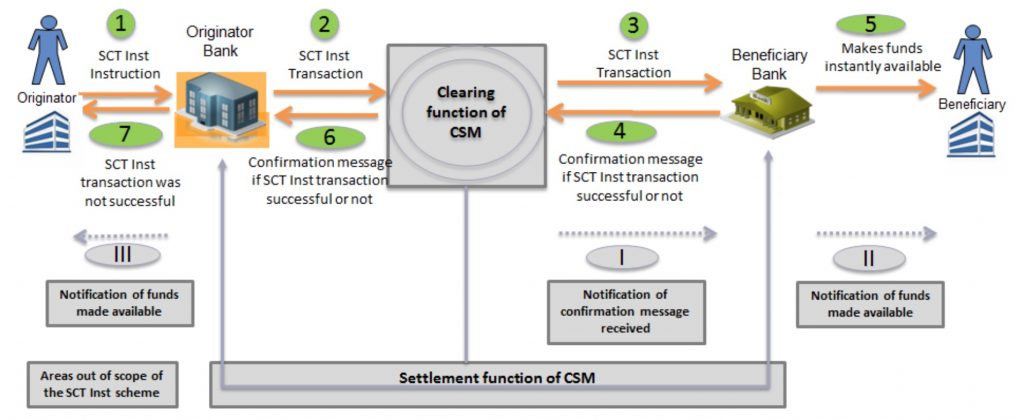

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.

At the end of last year the SEPA Instant Payments requirements from the European Payments Council have been published. Consequently the Dutch requirements 3.0 from the Dutch Payments Association were published last month.