Busting some of the ‘holy grail’ myth of reverse factoring as example of supply chain finance solutions….[Part 2]

| 8-1-2019 | by Marc Verkuil |

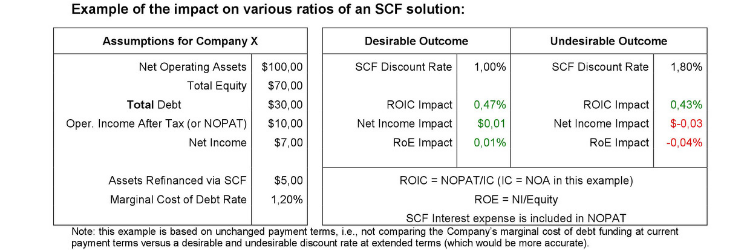

In the first part of this article, which focuses on the potential disadvantages, risks, and pitfalls of SCF and RF Programs in particular from the perspective of the Seller, the benefits of an RF Program were mentioned, while the almost unavoidable impact on a Seller’s WACC and the potential negative outcome for the Seller from an EVA, ROE and EPS perspective have also been discussed. In this final part of the article, focus will be on the possible commercial impact on account of SCF for a Seller, as well as on the regulators’, investors’ and credit rating agencies’ points of view. The article will present conclusions and some recommendations in the realization that since no company is the same, the thought-process going into the decision for entering or not entering into SCF will not be the same either; certain positive or negative arguments described herein may be more relevant for one company, while others may be more impactful to another. It is safe to conclude, however, that there is substantially more to SCF than what is typically presented and marketed, and it is hard to argue that SCF is the ‘holy grail’ to working capital finance for each and every party involved.

Both the immediate and potential future commercial impact of entering into an RF Program should carefully be considered…

What may be overlooked by Sellers when they are concluding upon a “cheap SCF solution that increases their ROIC and reduces their working capital balances”, is that such solutions are different from the usual forms of debt funding in the sense that even though the Buyers can not be a party to the transaction, these solutions implicitly involve all three parties in the combined commercial/financial transaction. This results in the Sellers having little control on the terms, conditions, and continuation of such funding solution, while there is an important commercial element that is not apparent in more common debt funding. The potential consequences of a lower credit-worthiness of the Buyer or less credit capacity or appetite of the Factor to the Buyer have already been mentioned in this respect. Moreover, and as argued before, an RF Program is usually offered subsequent to the Buyer, being the financially and commercially ‘stronger’ party, requesting an extension of its payment terms from the Seller. Even though the Seller may not be in a position to decline such a request anyhow, the Seller should carefully consider a number of commercial questions and, if deemed relevant, negotiate these as best as possible upfront with the Buyer: “does the RF Program provide real(istic) opportunities to increase sales and EBIT or ensure a more committed and longer term relationship between Seller and Buyer, i.e., do the commercial benefits outweigh the negative (financial and/or ratio) impact, if any?”, “can the Seller charge the additional funding cost, including the cost of extending its payment terms, of an RF Program structurally through to the Buyer?”, “could such a program create a precedent, and if so, what could be the impact (think of other customers requesting/requiring the same extensions and programs)? E.g., what are the long-term consequences of extending payment terms under an SCF program and what happens if or when the program is terminated; will the Terms & Conditions ‘automatically’ return to the old payment terms?” A sound argument in favor of an RF Program may be the fact that credit insurance (on the Buyer or in the market as a whole) may either no longer be available or be higher priced than what the Factor is offering. Hence, a number of questions and arguments a Treasurer usually does not need considered, let alone answered in a straightforward, bi-lateral working capital facility with a lender.

Also note the continuing trend of the desire for more transparency…

There is clearly a trend, driven both by regulators and investors, towards (public) companies being required or demanded to reporting or disclosing more financially relevant information, and as such, not only to leave less room for the non-disclosure of off-balance sheet transactions that may be relevant for the public, but even to add certain transactions that have historically been treated off-balance sheet, back into the financial statements for certain reporting parties; think of IFRS16 as a recent example in this respect. Currently, if receivables (invoices) are sold in an RF Program on a non-recourse basis there are no required reporting or disclosures in any financial statement filings under US GAAP or IFRS. For the MD&A section of a public company’s quarterly and annual filings (at least under the US SEC rules), however, disclosures are more judgmental and subject to materiality thresholds. Such potential disclosures cover a wide range of corporate events, of which the most relevant (from an SEC and FASB perspective, but probably similar for IFRS purposes) are: (a) “trends, demands, commitments, events or uncertainties that will result in, or that are reasonably likely to result in, liquidity increasing or decreasing in any material way”, and (b) “any known material trends, favourable or unfavourable, in capital resources, including any expected material changes in the mix and relative cost of capital resources, considering changes between debt, equity and any off-balance sheet financing arrangements”. An exact materiality threshold above which a company would be required to disclose its off-balance sheet (SCF) programs has not exactly been defined (yet) from an SEC or FASB perspective.

The reference above to the impact of certain (SCF) transactions on a company’s liquidity position is worth explaining further, as this is a position the major credit rating agencies also tend to take: due to the uncommitted nature of basically all SCF solutions and certain other (significant) financial transactions that are not reported in the financial statements of a company, the rating agencies, if or when made or becoming aware of these types of deals, will add these back into the financial statements for ratings purposes. The most important reason for their argument is that the moment these programs are terminated, the company’s liquidity position will be impacted and the company will most likely need to replace the off-balance sheet funding with an alternative source of funding, which the agencies unconditionally assume to be on-balance sheet unless the company can and would want to proof differently, which is a difficult task. Although there are no exact materiality thresholds with the rating agencies either (to the author’s knowledge), it is clear they effectively decide to adjust for those known SCF solutions that they deem relevant and material (in total) in both the balance sheet and income statements.

Conclusively, SCF solutions may be a valuable funding tool, but be aware…

SCF solutions, including RF Programs, may be a valuable additional and alternative source of funding, even for financially and commercially ‘weaker’ Sellers participating in such programs. However, these parties in particular should be well aware of both the broader financial impact, i.e., beyond the “cheap discount rate and positive ROIC impact” as often advertised by the Factor, as well as of the immediate and strategic longer term commercial and financial consequences of such programs, i.e., these solutions should only be entered into for “all the right reasons” and at the “right” cost (of marginal debt funding as the upper limit). Finally, from a Treasurer’s point of view, typically targeted with at least considering, if not outright optimizing the investors’ interests and having a ‘bottom line’ (WACC, ROE, EPS, EVA) perspective on things, it is recommended to ensure that even if certain of these solutions do not tick all above boxes positively, they do not impact or threaten to impact the company materially, both instantly and in the future, which could include putting a firm limit, e.g., an x% of total debt threshold, for these types of programs in place. Finally, it would probably not hurt for Treasurers, particularly those employed by Sellers again, to pro-actively advise their executive management teams and wider (financial and commercial) organizations of those arguments in this article that they deem to be relevant for their businesses.

Treasury Professional