")

Accounts receivable and payable teams need to be staffed, while inventory brings warehousing costs and obsolescence risks. But no business can do without it – everyone hates to win a sale, and then find it cannot be fulfilled, due to a lack of inventory or credit appetite for the customer.

The cost of working capital has increased recently: higher interest rates are painful, while just in time supply chains are being called into question, as COVID and geopolitical issues have disrupted logistics.

This call is the first of several where we look at how treasurers are handling this issue. This session was about the role of treasurers, and the involvement in the business decisions: this is a real test of treasurers’ influence. It was a rich and lively discussion – the full report is 15 pages. I encourage people to read it.

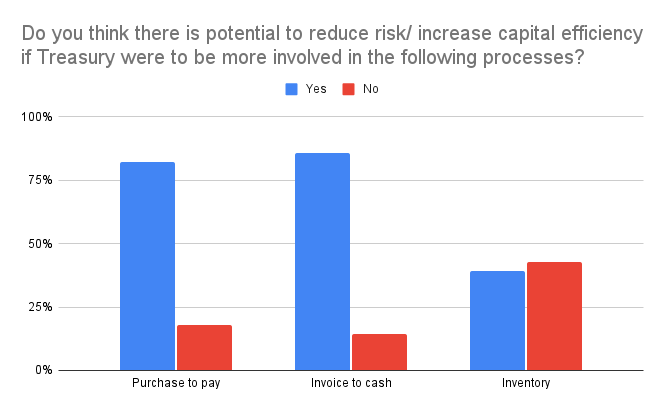

We started with the results of a survey amongst our members.

- This was not a surprise: participants all felt they had an important contribution to make, but that it was not being fully appreciated or utilised by the business. Involvement was highest in managing payables – it is mostly administrative. It was lowest in inventory management – this is typically under supply chain. Receivables management was between the two.

- This was not discussed in the call or the poll, but there was no mention of the mathematical models which can be used for the trade-offs between lost sales and financing costs. However, several participants wryly remarked that their businesses accepted longer payment terms for their customers than they received from their suppliers – even when they were the same company.

- Several participants benchmark their working capital levels to the competition. This can easily be done using the published annual accounts (but beware of differences in accounting treatment!), while some financial services providers have tools which use anonymised data from their working capital programmes.

The main takeaways:

- Approaches vary considerably. Some participants have the full support of the CEO and CFO. These companies view working capital as a key component of their balance sheet structure, and have implemented comprehensive programmes to manage it. These include KPIs and programmes implemented with Sales and Procurement. For others, management does not view it as a priority: KPIs either do not exist, or are lesser targets than sales and revenue.

- Management with a high focus on the topic was often new, and did not seem to be driven by financial necessity, but by management principles.

- One participant found that policies on supplier payment terms were not consistent between internal systems, and not always being followed.

- Some countries, such as Turkey and Brazil, have high interest rates, making working capital expensive: this often results in increased focus there.

- Modern cash management and cross border pooling can be a hindrance: local management is no longer concerned by funding or interest expense.

- It was often possible to shorten customer payment terms without a noticeable negative impact on the business.

- Internal measurement systems can be an obstacle: some actions, such as supplier financing, can improve the company’s EBIDTA, but hurt the functional KPIs of Procurement or Sales. Changing the KPIs involves internal politics.

- Factoring receivables and outsourcing collections usually improves payment discipline, but there was concern it can lead to inflexibility.

- Factoring is perceived as being expensive; a fuller analysis, including longer DSO and hedging costs often leads to a different conclusion.

- Treasury is not always involved in decisions on early payment discounts.

- One participant used extended payment requests and early payment discounts as a tool to require important CSR data from suppliers and customers.

Bottom line: no man is an island – especially if they are a treasurer. Managing working capital requires a cross functional team effort, and it varies from one company to another. The tools are there, and are well known: KPIs, supply chain financing tools, a fuller analysis of the hidden costs. How much attention they receive depends on the financial situation of the company – but, more importantly, the attitude of senior management.

A lot can be done if the business is on board – but only then!

Can’t get enough? Check out these latest items

https://treasuryxl.com/wp-content/uploads/2016/09/asml.jpg

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:21:242026-04-09 10:21:24Finance Internship: Support the Treasury Department @ ASML

https://treasuryxl.com/wp-content/uploads/2016/09/asml.jpg

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:21:242026-04-09 10:21:24Finance Internship: Support the Treasury Department @ ASML https://treasuryxl.com/wp-content/uploads/2020/06/ABB.png

225

225

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:15:492026-04-09 10:15:49(Graduation) Internship Treasury @ ABB

https://treasuryxl.com/wp-content/uploads/2020/06/ABB.png

225

225

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:15:492026-04-09 10:15:49(Graduation) Internship Treasury @ ABB https://treasuryxl.com/wp-content/uploads/2023/12/KBC.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:07:082026-04-09 10:07:08Funding & Liquidity Expert @ KBC

https://treasuryxl.com/wp-content/uploads/2023/12/KBC.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 10:07:082026-04-09 10:07:08Funding & Liquidity Expert @ KBC https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-Kyriba-7.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 07:00:412026-04-08 16:36:59Recap & Recording: Now / Next / Later — Top 5 Treasury Tech Priorities by Horizon

https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-Kyriba-7.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-09 07:00:412026-04-08 16:36:59Recap & Recording: Now / Next / Later — Top 5 Treasury Tech Priorities by Horizon https://treasuryxl.com/wp-content/uploads/2025/09/Nomentia-BLOGS-featured-5.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 12:46:262026-04-08 12:46:26SkySparc and Nomentia partner to strengthen treasury implementation and advisory support

https://treasuryxl.com/wp-content/uploads/2025/09/Nomentia-BLOGS-featured-5.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 12:46:262026-04-08 12:46:26SkySparc and Nomentia partner to strengthen treasury implementation and advisory support https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-Embat-3.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 12:42:192026-04-08 15:50:04Live Session: Goodbye Excel, Hello Smart Finance: Wie modernes Treasury echten Mehrwert schafft

https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-Embat-3.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 12:42:192026-04-08 15:50:04Live Session: Goodbye Excel, Hello Smart Finance: Wie modernes Treasury echten Mehrwert schafft https://treasuryxl.com/wp-content/uploads/2026/02/Monex-BLOGS-featured-1.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 08:57:462026-04-08 08:58:52April 2026 FX Forecasts

https://treasuryxl.com/wp-content/uploads/2026/02/Monex-BLOGS-featured-1.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-08 08:57:462026-04-08 08:58:52April 2026 FX Forecasts https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-TM.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-07 15:22:392026-04-07 15:22:39Live Session: What Your Treasury Should Measure (Even Without a TMS)

https://treasuryxl.com/wp-content/uploads/2026/04/Live-Session-TM.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-07 15:22:392026-04-07 15:22:39Live Session: What Your Treasury Should Measure (Even Without a TMS) https://treasuryxl.com/wp-content/uploads/2024/10/Carlo-_BLOGS-Expert-featured-2.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-07 07:00:292026-04-03 14:13:25The digital euro: Towards more European digital autonomy

https://treasuryxl.com/wp-content/uploads/2024/10/Carlo-_BLOGS-Expert-featured-2.png

200

200

treasuryXL

https://treasuryxl.com/wp-content/uploads/2018/07/treasuryXL-logo-300x56.png

treasuryXL2026-04-07 07:00:292026-04-03 14:13:25The digital euro: Towards more European digital autonomy