How to set up a forward contract and lock in a rate for your business

12-08-2021 | treasuryXL | XE |

A forward contract gives you and your business certainty, allowing you the peace of mind to have confidence that your international exposures are taken care of.

At Xe, they work with businesses of all sizes across many industries. They recognize that each business has its own requirements for its payments, and thus do they offer a diverse suite of money transfer products and solutions in order to meet each business’s international payment needs.

Let’s say that you’ll need to make a payment in the future. Right now, the rates are in your favor, but your payment is weeks or even months away, and you’re worried that the rates could change in the coming weeks, which would make your upcoming payment much more expensive than it would be now. You can’t influence the markets, but is there anything you can do to avoid feeling the brunt of currency market volatility?

In that case, the forward contract would be the right solution for you. Let’s take a closer look at what that is and how it could help your business.

What is a forward contract?

A forward contract is an agreement to buy or sell an asset at a specified price on a specified future date. In the context of money transfer, this is how it works:

-

You specify which currencies you’d like to exchange, and get a quote at the current exchange rate.

-

You select the date on which you’d like to send this transfer, and provide all necessary recipient and payment information.

-

On that date, the transfer will automatically trigger, and will convert and send at the previously established rate.

You could think of it as the “buy now, send later” money transfer option. You’ll do the work of setting up the transfer now, and your currency exchange will happen at the current exchange rate, but the transfer itself won’t happen until the date you’ve specified.

Why is a forward contract useful?

A forward contract can be useful in two ways: allowing you to lock in your rate to avoid future volatility, and to ensure that your payment will be sent (and delivered) by a certain date.

Changes in currency values can dramatically impact the cost of your business money transfers. If the currency that you’re sending weakens, or the currency you’re transferring to strengthens, a simple payment could suddenly become much more costly for your business. A forward contract gives you and your business certainty, allowing you the peace of mind to have confidence that your international exposures are taken care of.

Additionally, if your payment needs to be delivered by a certain date, arranging your payment in advance can ensure that it will be sent on time. No matter how busy things get leading up to the transfer date, you can rest assured that your payment is taken care of.

How to set up a forward contract

If you’re interested in setting up a forward contract and securing a rate for your business’s upcoming money transfer, give them a call to set that up with our team. If you don’t already have a Xe account, take a look at their guide to registering for a business account.

Get in touch with XE.com

About XE.com

XE can help safeguard your profit margins and improve cashflow through quantifying the FX risk you face and implementing unique strategies to mitigate it. XE Business Solutions provides a comprehensive range of currency services and products to help businesses access competitive rates with greater control.

Deciding when to make an international payment and at what rate can be critical. XE Business Solutions work with businesses to protect bottom-line from exchange rate fluctuations, while the currency experts and risk management specialists act as eyes and ears in the market to protect your profits from the world’s volatile currency markets.

Your company money is safe with XE, their NASDAQ-listed parent company, Euronet Worldwide Inc., has a multi-billion-dollar market capitalization, and an investment grade credit rating. With offices in the UK, Canada, Europe, APAC and North America they have truly global coverage.

Are you curious to know more about XE?

Maurits Houthoff, senior business development manager at XE.com, is always in for a cup of coffee, mail or call to provide you the detailed information.

![]()

Visit XE.com

Visit XE partner page

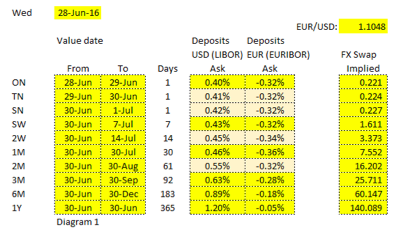

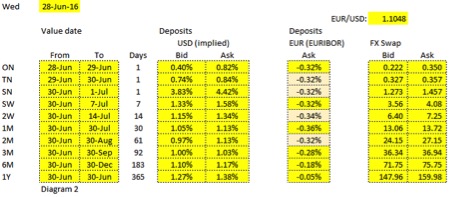

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows:

Now if we would consider exchanging a USD deposit versus a EUR deposit for 1 year the cash flows would be as follows: e are looking at a single day FX swap, the annualized rate could swing a lot.

e are looking at a single day FX swap, the annualized rate could swing a lot.